@buyinghouse is showcasing his knowledge again. You can’t sell real estate and put the money into a 401k. There are annual contribution limits on a 401k (same with Roth IRA and IRA too). Roth IRA even has income limits. If you’re above the limit, then you can’t contribute new money. The tax deduction for IRA contributions phases out too. Most of us invest in stocks and RE. It’s called diversification.

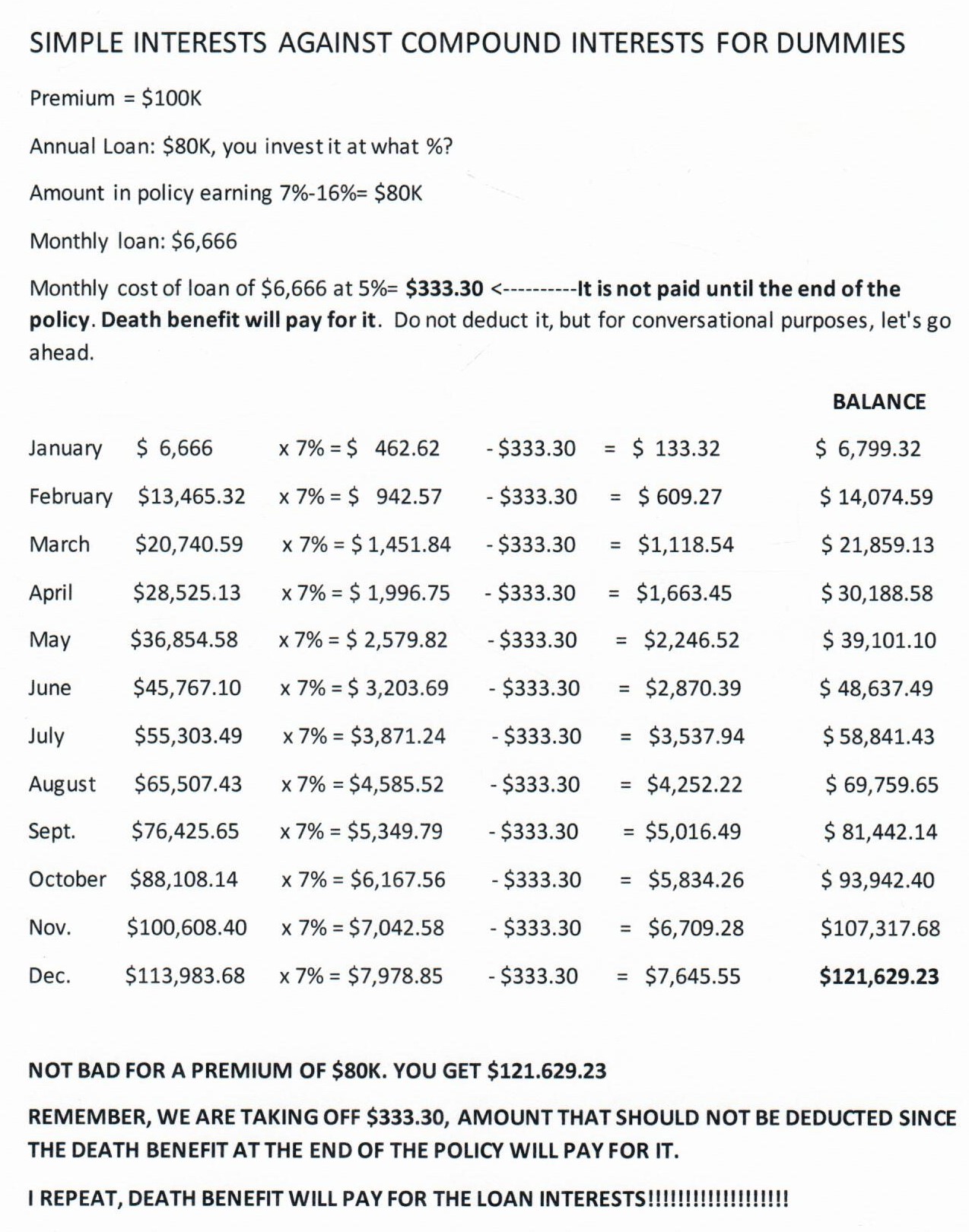

You still don’t get my point about your IUL policy either. You aren’t guaranteed the 6.75% return each year. It’s what’s called a statistical average. Some years are better and some years are worse. That’s what indexing does. Per your own data, 6 of the last 20 years had a 0% return. That’s 30% of the time you IUL generates a 0% return for the year. Do you know how much compound interest you earn in a year with a 0% return? Compare that 0% compound interest you earned to the 4% or 6% you pay for the loan.

$46K at 0% return = $0 of compound interest earned

$46K loan at 4% = $1,840 of interest owed

If you borrow, then 30% of the time you’ll have that scenario. Your policy earns zero but you still owe the interest for borrowing. You keep pointing to your illustration that you’re earning 6.75% compounded per year. That’s only a statistical average. 30% of the time you earn zero. Those years are very bad for you, since you still have to pay interest on your loan.

He won’t have anywhere near $600k/yr if he keeps borrowing the cash value every month. You think borrowing the cash value is some sort of trick where you’re out smarting the insurance company. All it is is leverage, and you don’t even realize you’re using leverage. You’re betting the investment gains in the policy will be higher than your loan amount.

I know you can’t argue the math, so I expect more insults.