After some cursory scanning, it might be easier to get 10x through mid cap than small cap because the calibre of the leadership of small cap is not that good or not proven, not sure how to assess before is too late. When AAPL is danger of insolvency, calibre of SJ is well known, so is a good bet.

Absolutely. Mid cap is much more proven than small cap. You can invest with 100% more confidence.

You also know you are getting much better growth potential than large caps.

So it’s really the best of both worlds.

If I want to invest long term, I would prefer UBNT and VEEV as I feel both are less risk. Not now, wait for opportunity.

TDOC and SHOP are volatile, not made profit yet, Risky ones.Both are subscription or customer account based, highly hyped and making good progress companies. Risky assets during current environment. Not now, wait for opportunity.

Redfin had sales of $59.9 million in the first quarter of this year, up 44% from a year earlier. It lost $52.84 million on that revenue.

1 Like

That’s why I want a founder CEO. Anyone brought in as a manager-type CEO of a small cap isn’t likely to set the world in fire.

1 Like

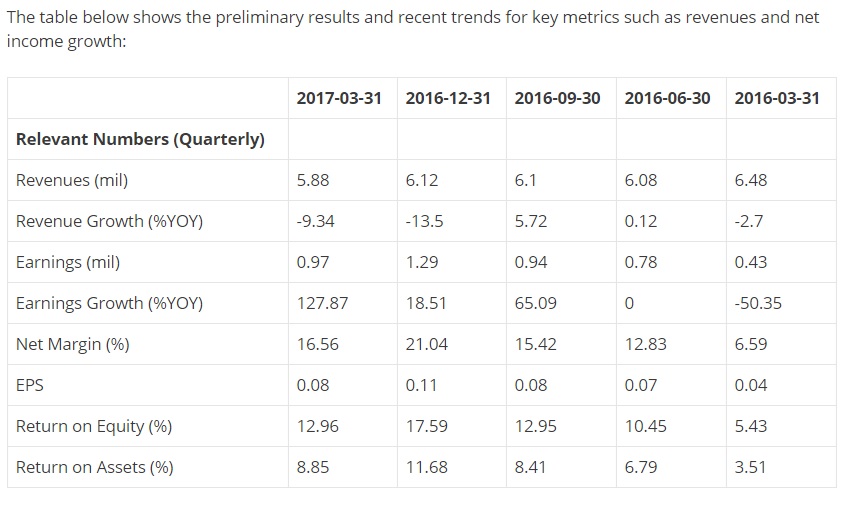

Why Ellie Mae Stock Is Sinking Today

Shares of the fintech company cratered as lower refinance volume weighed on its second-quarter earnings.

Jordan Wathen (TMFValueMagnet) Jul 28, 2017 at 12:58PM

What happened

Shares of Ellie Mae (NYSE:ELLI) are sinking today, down by about 20%, after the company reported second-quarter earnings and reduced guidance.

So what

Ellie Mae has enjoyed unrelenting growth in the years following the financial crisis as banks and other mortgage originators turn to its software packages to help them navigate new mortgage regulations and compliance requirements.

This quarter, Ellie Mae reported that its net income increased 78% compared to the year-ago period. However, much of that increase was driven by tax impacts, rather than operating factors. On a pre-tax basis, income grew just 6.7% in the second quarter compared to the year-ago period.

Weak growth was the result of lower mortgage refinancing volume and a tight supply of homes for would-be buyers. On the conference call, management noted that the average user closed only 1.35 loans per month during the second quarter, down from 1.51 closed loans per user in the year-ago period.

Now what

Lower refinance mortgage volumes aren’t just a first-half story. Ellie Mae CFO Matthew LaVay said that “[i]n the second half of the year, mortgage volume is expected to be down 28% year over year, driven by refinances down 57% year over year” in prepared remarks on the company’s conference call.

For the current quarter ending in October, Ellie Mae expects its per-share earnings to range from 38 cents to 41 cents.

The company said it expects revenue in the range of $104 million to $106 million for the fiscal third quarter.

The company went on to lay out guidance that it would earn adjusted net income of $1.47 to $1.50 per share for the full year, well below the average Wall Street analyst estimate of $1.90 per share. Ellie Mae expects full-year earnings in the range of $400 million to $405 million.

Stay away from ELLI

Disturbing news is this is software for Real estate financing/refinancing and the volume or demand is coming down.

I was lucky to have purchased FB during this mid cap phase (at $100B) and TSLA during its small cap phase (at $5B).

Now I’m at the same place with BIDU and NFLX (in terms of midcap). With small cap, I’m betting on YELP and TWTR.

All are companies run by founders!!!

AAPL and MSFT are two stocks that have you bought in when they are small cap led by outstanding founders would be keepers. They both paid dividends now. Should look for such potential in small caps, and mid cap.

INTC and CSCO are not as spectacular but still good if bought when they are small cap. Both pays dividends also.

1 Like

I think the only reason to own stuff like AAPL, MSFT is if you bought them over a decade ago and have already gained like 1000% over them. Now they are solid passive income dividend generators so it’s a keeper because selling them would incur huge tax consequences. Otherwise it’s better off to try your luck with mid cap and small caps.

Can you review EVOL, this is tiny start up, but pays dividend, good Profit Margin…etc? Let me know whether it is attractive?

Declining revenue,

CFO resigns two months ago,

Being investigated for potential breaches of fiduciary duty by its board of directors

market cap $61mil, even lower than LQMT ![]()

What is the growth path?

1 Like

Lawsuit may not be major concern unless the actions are from SEC/Government agencies.

7.5 Million cash reserve, 16.5% profit Margin, 8.92% dividend (32.8% payout ratio).

Negative: Very tiny company, no volatility, no volume too. Sales are not steady, but cyclical.

Typical for small company. LQMT is not much better. So is not really a concern. We need to know the possible growth path. EVOL is on a managed services model, how far can such a model grow? It seems the trend now is big boys serves small boys e.g. Apple, Google, Facebook, Amazon, BABA, … Managed services model is small boys serve big boy which is bad because big boys can squeeze all the profit from you. What is the pricing leverage of a managed services model business vs clients?

UBNT sounds good, still figuring how good is it vs CUDA.

1 Like

I am negative on CUDA as the Net profit is very small while UBNT is too good for technology company range 20% or above.

CUDA = High PEG, High P/E while UBNT decent PEG and P/E. Naturally, UBNT is better than CUDA.

FYI:I do not own both.

1 Like

1st time poster, been a lurker since Redfin shutdown their message board.

Thought I’d share JBGS as a possible winner and to get some feedback from you guys. JBG is a big REIT based up the road from me in Chevy Chase, MD. All over the place in the DC area and have grown substantially over the years, especially since I moved here from the BA. Just went public on the NYSE a couple of weeks ago, too, so not a lot of information out there. Quarterly common dividend of $.60 a share. Stock is currently $35.27/share.

2 Likes

I wouldn’t try to study profits or earnings of companies so diligently at all. Waste of time! All these things have already been priced in. Current prices reflect that. Question is whether you are comfortable buying them. You are not going to know more unless you are an insider. And insiders with info are restricted from trading anyways!!!

The best bet you can make is that if you happen to know a hotshot personally before he became a phenomenon, invest in him. Elon Musk was not that famous at all a decade ago. But I knew him personally since 2000 when he hired me into x.com. Same goes with FB. I knew Peter Thiel personally when I was working at PayPal so I had confidence with his investment. Today, TSLA and FB are two of my most valuable assets.

1 Like

I hope you do not mistake me telling this!

With this statement, You are lucky to be winner so far. You just blindly believe some well known people.

IMO, you need to read two books

Margin of Safety ( read page by page )

Intelligent investor

These two books will provide visibility what market is doing. You follow market is efficient theory which both books tell you NOT ! Both books are well regarded

I’m not following the market efficient theory at all. If I did I would’ve just invested into the S&P 500 (Or the world index). How was I blindly following some well known people if they weren’t well known at all when I first followed them?

All your research might enhance your knowledge, but ultimately it’s a waste of time if you are trying to gain an edge in beating the market. There are thousands of hedge fund and money managers who spent tons of money in generating the winning stock pick. You think just by reading a couple books you can gain an edge over them? You are not going to gain any edge even after you had studied 1000 books.

Yes, I might be lucky in that I happened to pick the right winners back in the time. That was my way to achieve success. I’m also pretty sure that you’re probably not going to achieve much success with this kind of research. I think it’s better for you to spend your energy with something else if the goal of doing this is to increase your net worth.