“The usual way is sell losses 30 before end Dec i.e. by late Nov, and don’t trade that counter till next year” => To know exact what to sell and how much to sell we need to know YTD profit so that profitable holdings are moved to next year and we take some loss to match YTD gain.

I use Robinhood and they do not give YTD P/L deliberately !

They want the users to mindlessly buy, sell and finally last 5 days before Dec 31 match the loss (as they give 1 year P/L).

Another simple way is to drag the hand over the year P/L and hold it on Dec30th (Friday, last day of the year trading day), you will see P/L and this is the start day, you can calculate current appreciation and subtract it. Many redditians also suggested this route.

Exceptions are there, whichever company hoards profit abroad (say AAPL or AMZN…) etc or Startups (like SHOP or TDOC), providing weight-age to GM is fine (please note weight-age), but ultimate growth is behind Net Gain.

I prefer BABA over AMZN as the NM is too good for BABA. Such NM high companies are safe during downturn as they do not fall drastically.

By focusing NM, both Seth Klarmann and Warren Buffet made big strides. For example, both of them invest in SYF, Low P/E.

Safety of our invested money is more important than making profits. That is the main reason, I sold SHOP with small 3% profit having 50% of cash in it and reduced to 5% holding.

If there is downturn, IMO, fall of AMZN (low PM) will be higher than AAPL, BABA and GOOGL (all three higher PM). People may contest this, but that is my own guess work.

I agree higher net margin will do better in a recession. Why not just get short the market then though? We are in a bull market. Growth stocks will out perform. Net margin improves as expenses are leveraged across more revenue. High gross margin is the foundation to enable that leverage.

Tesla recently said their GM will be 15%. That’s way below tech companies and barely above Ford and GM. You don’t pay a premium for that low of GM. There’s not a road to being highly profitable.

TSLA, AMZN, NFLX are exceptions and are driven by Gross (based on customers/accounts) than Net. I consider SHOP,TREE and TDOC are like that too (but some people completely differ). SNAP is trying to come like this, but it is not given that status yet. There may be other companies fall such exceptions like TSLA, but it depends on case to case. In spite of such exceptions, they have the risk.

Shorting is considered speculating, very short term objective. True, Shorting (and PUTs) can be done when we really know the downturn. For example, since beginning SNAP is going to go down, still chances of going down is higher than going up. How confident we are to short that stock?

To my knowledge, the concept of investing (vs speculating) is hold for long, across the downturns. Such people buy strong companies, hold for long, rarely sell. For those, the NM and P/E are very important factors than others.

A blog friend was asking me to think long term holding AAPL when it was $415 (pre-split). I never understood that concept at that time. He was telling me think long term 5+ years or 10+ years. Till date I am not doing that.

In this blogger, I see hanera and wuqijun are holding longer.

IMO, it is too hard to identify such companies.

BTW: After a long research, and back and forth buying and selling, I am now convinced to move my money to Mutual Funds/ETFs than holding stocks. My stocks growth is appx 15% while MF like FSPTX growth is more than 25%.

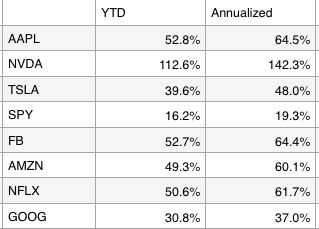

YTD? May not be Apple to Apple comparison. Could be because you didn’t commit fully all the time… usually traders are too scared to go 100% in. If you’re adding fund to FSPTX says once a month, the return is lower than 25%, may even be lower than your 15%. Below is a table for return of ANT & FANG & SPY assuming 100% in on 1st day of 2017, no additional fund in between.

IMO, NVDA is genuine gain, rocking every quarter. NVDA is not only chip maker, but bigger company with multiple products. I posted those when NVDA was $70.

The way I counted is this. Except SPY, I have purchased all of the above you said. ANT & FANG, with 5%-7% stake. There are some misses and altogether my portfolio resulted over all appx 15.5% ( fidelity provides 19.5% based on various amounts I added YTD).

I still hold some stocks like BA,NVDA, AMZN, UBNT, AAPL, ANET…etc 25% or more. For this, I need to do lot of research (good education though) some hits and some misses. These misses are real eye-opener.

In parallel, I bought FSPTX 3 months before, appx 14% up, then reviewed YTD 45%. It is a great miss from my part not noticing such a good MF. The thing is it is going to be my true buy and hold.

Now, I have divided my cash into three mutual funds FSPTX, FBSOX, FSCSX. On any case, I can no way match the speed of these three Mutual funds. Above all, I do not need to worry about paying taxes as I can hold as long as bull market is running. This is going to be my 2018 plan, but already started now.

Please note that I just want to inform you NVDA is doing great, this is for your information. As an investor, you can do your own research and see the difference. I am not here to justify the NVDA valuation.

However, you asked a thought provoking question for which I researched further and got a convincing answer (for myself).

Here, I have shared an answer for you. If you still feel NVDA growth is not genuine, I am perfectly fine. You can take it or leave it.

Valuation is complex and investors buy premium (just like the way we see bay area real estate) for profit acceleration (PEG).

With your same statement “Did it’s revenue or profit also increase by 10x from 2015?” you can not qualify NFLX, AMZN, TSLA, why not even AAPL and GOOG !

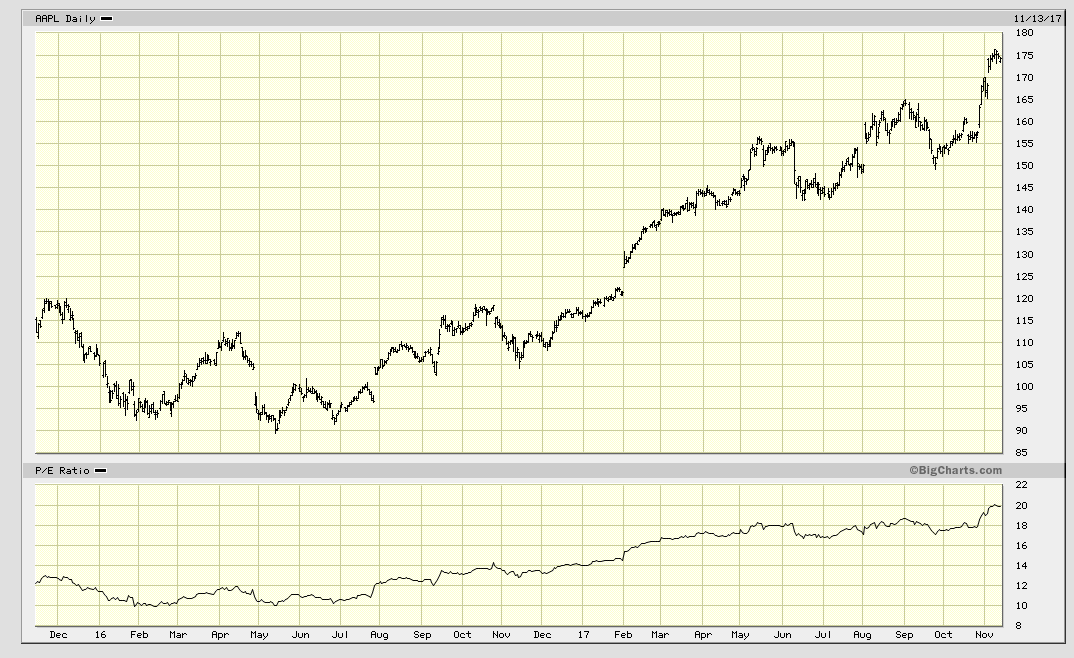

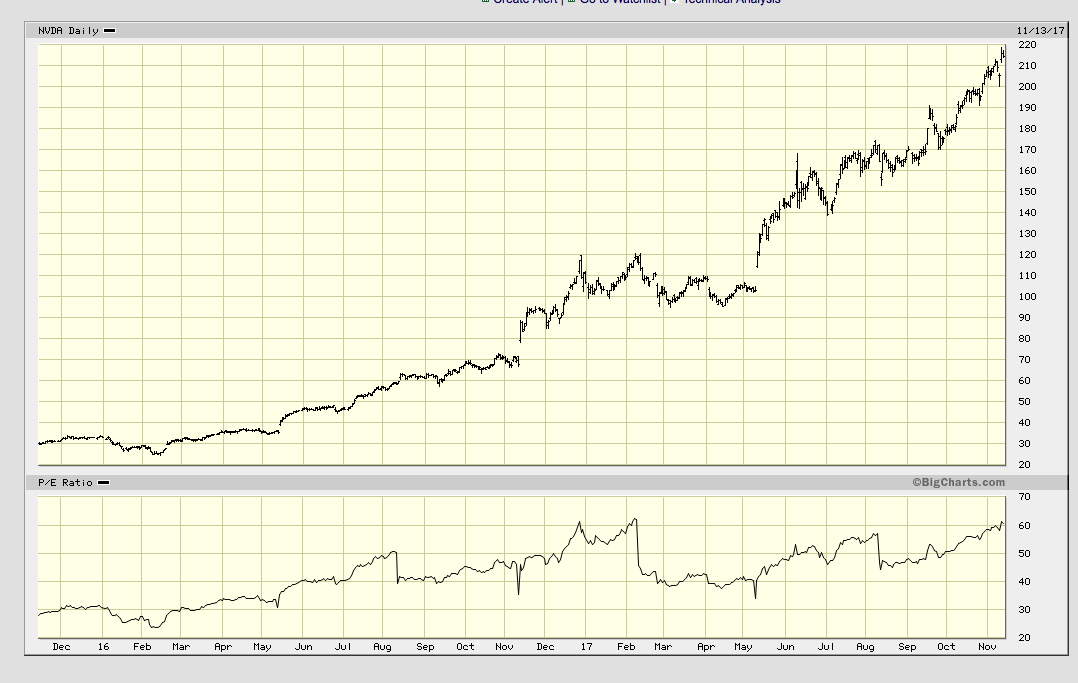

Here you go the difference between AAPL and NVDA. Obviously the growth of NVDA is faster than Growth of AAPL.

If AAPL growth and Price are justified, NVDA Growth and price are also justified…

Your charts are not good enough to dispute wuqijun’s comments. There are no share price or market cap in your charts. You need at least a revenue vs market cap comparison or a P/E trend. Apple returns quite a lot of capital to shareholders, share buyback reduces the number of shares hence push up share price but reduce market cap. Your charts are not Apple to Apple comparison.

At least NVDA has profits. TSLA is up a ton while burning cash like crazy, showing no signs they can build their product, and no hope of being profitable. They’ve guided gross margin down to 15%. That’s them admitting they another car company.

Not so. Tsla stock did not increase 10x in the last 2 years like Nvda did. Its gains happened way in the past. Flatlining is a good sign that it’s not a bubble. Nvda is most definitely helped by the unreasonable climb of bitcoin values. Of all the fang ant and bats, only Nvda has any significant linkage to bitcoins. I would be 10x worried owning nvda today than owning Tsla or any other fang stock.

See below… nvda rise is definitely driven by bitcoins. Investors already have this vision in mind…

How much of NVDA’s gains is related to bitcoins and how much isn’t? Hard to quantify this but given that the company has been around for a long time before bitcoin, and the sudden explosion of its market cap coinciding with the rise of bitcoin, it’s not hard to piece the puzzle together… I would say without bitcoin NVDA’s valuation should drop back down to the way it has always been.

This is exactly the issue I am facing. I am looking for an easy way to find out unrealized and realized gains/losses by individual tickers for 2017 so I can make a decision if it makes sense to realize some losses in 2017 to offset gains. Robinhood is severely lacking in giving these metrics so was wondering if people have already figured out a workaround. I am assuming mature companies like eTrade and Fidelity must be sharing these metrics.

The 1yr review window with manually tracking 30th Dec start shows total gain/loss and doesn’t differentiate realized vs unrealized!