I believe in SQ long term. IT passes a large smell test - i see and indirectly use their pos system every day. They are moving to become a business lender too, so overall, i think their prospects are good.

The recent 10+% move is unwarranted, and i feel like it’ll drop, but i will hold. I am leveraged on SQ.

One way to lock in gain in SQ, if you are worried about it going down, is to sell the stock and buy the calls. Make sure the calls are at the money though. I am sure option guru @hanera can fill you in on the details.

I am new to options strategy. Still reading my first book. So maybe you can roll it up? To buy some calls nearer the money instead. You can either sell one and buy one, 1:1 ratio, or even do a 1:N if you are a crazy bull like @wuqijun.

Wow this is a significant moment for me because I have always been the one influenced by YOU all on this forum. Reading, learning, and (mostly) silent until recently.

Now for the first time I actually feel like an influencer that our forum creator himself has followed me into an investment. Wow! This is a poignant moment for me!

If there are other lurkers like myself out there…know that you too could be influencing people like @manch if you speak up. And, maybe one day, even @wuqijun!

Haha well I meant that you are very stubborn and hard to convince! That judgment is based almost solely on the whole bitcoin thread.

But I don’t think it’s insurmountable. I mean, you’re still active in the bitcoin thread even if it’s to say it’s going to zero. So I think you’re open to being convinced of something new…

IMO putting money in all oil stocks has the same risk, rather I focus on the top 2 companies and buy one of them., the diversify with different companies.

In this way, I own XOM (not Chevron, nor BP), moderate profit margin, payout appx 66% with 4.15% Dividend.leader in USA.

Next best one I see now is WFC, selling one of the low end, good dividend, profit margin, but kind of legal issue with government scrutiny. They will ultimately pay some penalty and come out of this mess, but stock is too good.

My own preference is MASI, medical equipment company, it was down, but up 5% since I bought. No dividend, but selling less than fair value, good profit margin. The other leader is Sunnyvale based ISRG, best to buy at DIP.

Next one is RS, steel and aluminium, company moderate profit margin, good dividend for last 5 years and good growth last five years. This one of the best in steel companies, benefit is Trump steel tariff, better to hold long with nice dividend.

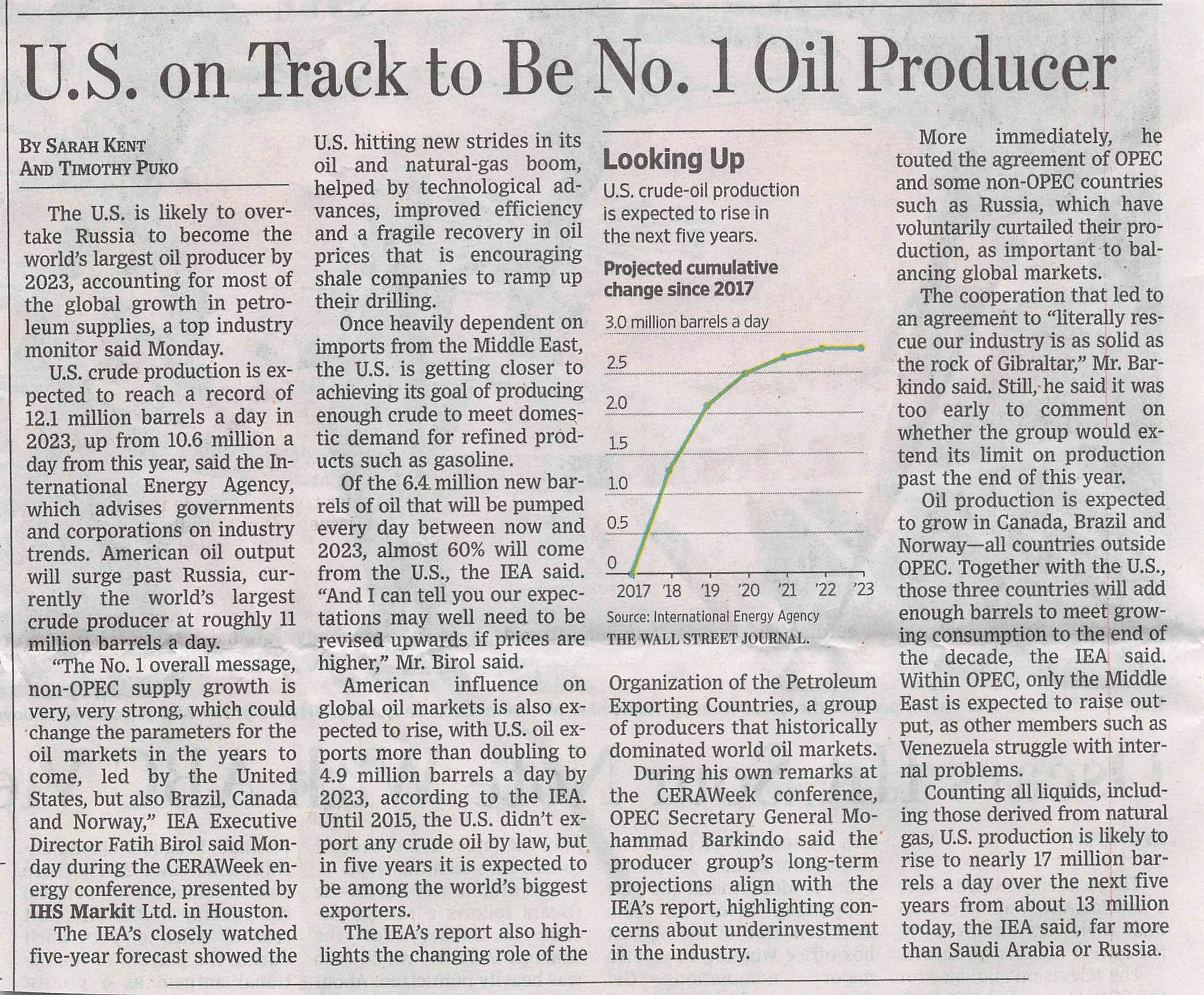

Global demand for crude is likely to “plateau” during the late 2030s, mostly because of the rise of electric cars and trucks, BP predicted Tuesday in its annual outlook.