Can you get 50k 401k loan to buy an investment property? Does Fidelity or other brokerages verify whether you are using the 401k loan to purchase a primary home?

You can get the loan for any reason, not only for home buying!

The interests you pay will go to your own 401k account as ROI.

The only issue is that 401k loans are low interest around 4% range while stock or mutual funds may return you around 10% to 15% level.

Normally, people suggest not to take 401k loan, but primary home buying is a reasonable one to take loan.

Broker won’t verify any documentation except when you request for 10 year amortization ( docs required ) when buying primary home

1 Like

That’s great. Somehow corporate brainwashing gave me an impression that 401k loan is for first time primary home purchase only. It’s a great program with such flexibility.

1 Like

If you read your 401k plan summary documentation, you will be informed everything clearly. It may be 12-16 pages documents from your company 401k plan.

1 Like

what company is this?

You can borrow each 50k separately!

1 Like

Thank you so much for your advice! I also had no idea you could borrow for other things from 401K.

If you can move your 401K, cash it now that the tax brackets lowered. Do it as many times so your tax bracket is not effected by the income it generates. Then, open an IUL with big lump sum.

Count on your husband income x 23 for a death benefit. Death benefit will increase by default every year to accommodate/pay for the loans.

Open it on your husband. It costs a little bit to get insured, but you can loan up to 80% of your premiums without paying them back. Ever!

As I was explaining before, $100K a year, you loan $80K +.

Then, after using $80K for whatever purpose you want, you still have $80K earning 7% + up to 16% depending on the 4 strategies to choose from so the insured retires with a good amount of cash.

$80K + $80K = $160K.

It takes some time to understand it. This is new, something the archaic stone age people won’t get in their brains. You know, the OPM thing, other people’s money.

I don’t understand how cashing in the 401K at the time when my husband is working (and I will probably be working soon too) would help with the tax issues ![]() We’re at the highest tax bracket we ever will be, and then you add 10% I thought.

We’re at the highest tax bracket we ever will be, and then you add 10% I thought.

3 Likes

Lol, you said you can’t just contribute a lump sum to IUL. You have to do a needs analysis and contribute the money monthly. At least that was your answer when I asked why you didn’t sell your home and invest all the profits into your IUL policy. Now you say you can contribute it lump sum. Which one is the lie?

You don’t even understand what OPM is. You’re talking about loaning yourself your own money.

Oh boy! Do you know this is not an illustration but a suggestion? I am putting an example! Jesus!

Gee, thanks for remembering we need to make a needs analysis. Except that is done when people are interested.

You are learning, cool!

Lump sums, are allowed one time in the beginning of the policy. We’ve had clients, opening a $3K a month, $22K lump sum. They loan the cash value immediately as soon as the IC transfer the premiums into the policy. It could be a matter of days.

What I said is that you can’t just throw an amount you like to contribute, income, health and age are counted in the equation.

Now, go back and read a book. I said that the death benefit or face amount, whichever you want to talk about, is 23 times the insured’s income.

And, I believe terri’s husband makes good $. I don’t know about her income. I am pretty sure they both may make $8,333 a month. Gee! A Mexican I know working as an electrician is making $81 an hour.

Now, as I said before, if you don’t believe on this, just skip the comment. Why wasting your time on something you know pretty darn well?

$80K + $80K = $160K…Don’t you love it? $100K in, $160K results.

So, again Marcus, what’s your income, or what’s your % returns if you got $80K in your hands, and another $80K making 7%-16%? Don’t forget, simple interest against compounding interests.

I am pretty sure, terri would agree, that $80K can pay a handsome mortgage in the vicinity of $1M every year. Not counting what you get in appreciation. 5%-10% appreciation every year?

Add all those winnings to your pathetic complaint about paying 4% simple interests against 7% compounding interests. You are never, ever, gonna win the debate.

I forgot, you mention 40% of the times when the market went down. Well, if the market goes down, so it’s your 401K, right? Did you forget that little detail, last crash, 38.5%? And the small detail that with IULs the loss is stopped at 0. No loss of principal?

And, that if you don’t want to loan money because you are going to pay interests, well, don’t loan. Or don’t contribute the excess, just pay the cost of insurance, if something happens to you, your family will have plenty of cash to survive. Pretty simple, it’s all about mathematics, something you lack on this thingy.

Pretty tough, right?

Yup, now we have more fake math that’s been previously debunked.

Here you go again with simple vs. compound interest. You can’t even tell the loan interest is compounding every month. Go ahead and deny the loan interest is compounding, because you’ll just look like a fool to anyone that understands basic math.

You and your mentor are so smart that you thought 7% compounded monthly means you get 7% every month. That calculation you 2 put together was hysterical.

Dude, you are not only so ignorant to some point is risible to explain you anything. First of all, you couldn’t make me a spread shit about numbers I gave you, you, the 2 phds in whatever couldn’t do that after mumbling and jumbling you could? You are fighting against a dude who can’t even write proper English but giving you a lesson of how to be quiet when you don’t know crap about anything? Oh boy!

Well, I had the patience to wait 26 years to become a citizen of this once great country, why not to relive my passion for teaching?

I am going to explain a little bit more. Please learn to be positive, you may be scaring people from believing in illustrations approved by the state of CA and the department of insurance. What’s next? Taking over the DOI by your treasonous Russian puppet commie government?

There are costs you pay for riders. And there are payments for the loans.

Under the contractual law, the insured is paying for a death benefit. Once he pays a premium after being approved, there’s a death benefit to be paid. That’s the deal. He dies, or gets injured, very badly sick, or terminally ill, he or his beneficiaries get paid whatever money is left from the death benefit if he has made loans.

Since ICs are here to make money, they give a death benefit, that creates $ to be paid. So, they allow you to choose between option A or B. We use option B that increases the death benefit as a way to wash out the loans. Client also pays for a rider to allow such loans, a few bucks every month.

So, since there’s money to be paid both to the IC or client, the IC creates a collateral account. That account deducts from the death benefit all the loans made. That’s why on any illustration, the death benefit is increased every year. It is like they are giving you free money. Of course is not, but if you see the huge amounts of income you will earn at the end of 30 years of compounding interests, something you laughed when I made that 5th grader explanation of how simple and compound interests work, you will see that it makes sense, the numbers are working towards the $334K the client will get when stops paying premiums and getting his income.

Disclaimer: The other 80% returns are not real money you can loan 100%. You loaned $80K every year, but some policies show $100 in, $100 loaned out after 10 years. We suggest to loan what is considered OK, 80%, but we have seen 90% loaned since the market is doing so good. We advice to leave a buffer zone of 20% counted as premiums. The 80K is earning 7% or more, as seen in the last 20 years.

Now, I may be stupid, but I swear I’ve seen people suggesting never to quit contributing to a 401K when a downturn even though they keep paying every time they move your money, lots of costs, everybody knows it but nobody wants to talk about it. You lose 50% of your money, you need to recover 100% to make it even.

So, why not with the IUL? You are paying for a protection when the inevitable happens. We always aim at paying the mortgage on a house. Or, as the news are telling us, pretty soon another tragedy will strike the economy, the insurance companies offering LTC long term care are going to not be able to pay for the benefits their clients paid 30 years ago. They thought the care was going to be $2K a month. LOL…

You know Marcus, one day I was bitching about the % for a loan to be paid for a home I am not going to disclose more details for. "I saw a “glitch” on the numbers, you know, I am so smart.

Well, the loan officer told me to go and suck wet sand at the beach, to quench my thirst, and he called me names, from an idiot, stupid and mother f…er and more.

Later on, another insurance agent at my office and loan officer at the same time explained me with details and laughed at me for doubting an illustration approved by the state of CA.

He said “you know what man, stop being judgmental, you sound line an idiot when you are complaining and criticizing shit about something you don’t know anything about”

Then, he reaffirmed his statement with this: “you know my friend, these are different times, you may not know it, but I am going to tell you, I can go to jail if I am hacking into an illustration to show numbers deemed not possible”.

Oh boy! I learned my lesson that time.

And so should you.

Don’t be a_____ fill the blank.

Given the same situation is permanent, and premiums are paid, my illustrations are a not only legal, but a contractual obligation if they are accepted by a client.

Now, go and say hello to your comrade Putin.

This is the playbook for when you can’t argue the facts:

- Ignore the question

- Pivot to a different topic to deflect

- State a bunch of irrelevant info to deflect

- Talk in circles a bunch

- Launch a personal attack

You just proved my point for me.

1 Like

So, again Marcus, what’s your income, or what’s your % returns if you got $80K in your hands, and another $80K making 7%-16%? Don’t forget, simple interest against compounding interests.

$80K on policy earning 7% - 12% -16% ???

Then, you have another $80K paying a mortgage of $6,666 a month. You are getting what? $5-7K a month or more from that rental, right?

Add all those winnings to your pathetic complaint about paying 4%-6% simple interests against 7% compounding interests. You are never, ever, gonna win the debate.

Answer that with numbers, not with stupid remarks.

You are the 2 phd guy, not me. Answer with numbers or be quiet about it.

You keep repeating the simple vs. compound interest. Please go learn what the terms mean. The loan interest is compounded. It’s clear as day in the illustration.

You again misrepresent basic math. The real math is:

-$100,000 into policy

+$6,300 (7% gain on the $90K cash value of policy)

-$4,000 (5% interest on the $80K borrowed)

+$80,000 (borrowed from policy)

+$5,600 (7% gain on the borrow $80,000)

Total is -$12,100 for the year. As you can see, the $90,000 in the policy is only earning you $2,300 after the interest expense of borrowing $80,000. Your net return is a whopping 2.6%.

Alternatively, one could simply invest the whole $100,000, earn 7%, and be +$7,000 for the year. That means just investing the $100K is $19,100 better than buying the IUL and borrowing from it. What can I buy with that extra $19,100/yr or $1,592/mo? I can buy a $3M term life policy for 25 years for under $600/mo. Do you realize $1,000/mo compounded for 25 years at 7% gain is $810,000. Plus, I’d have my $100K/yr compounded for 25 years at 7% worth $6,325,000. That brings my total to $7,135,000.

How’s that for compound interest math?

1 Like

I believe you were editing your response when I was working on mine. You need to know what you are talking about because it makes you look like you don’t know what you are debating. ![]()

![]()

![]()

Every time I show this to my mentors, they can’t stop laughing. They ask me if this guy is a real investor and knows the difference between compounding and simple interests. I tell them no. They can’t believe it.

OK. Enough said. You sir, are pathetically infatuated with negativity towards a product that is working fine, a product that is utilized by the rich people. Specially those smart enough to not be with their nose embedded in a computer watching the stock market every day.

What’s more pathetic is the fact that you are trying to portray this product, or my illustration as lies and fraud? Really? Do you bitch and moan when they show you a loan document? No, don’t tell me, you bitch about how fraudulent they are! Jesus! No wonder! You are a pinching penny guy, aren’t you? ![]()

![]()

![]()

you got to laugh mister, life is too short! ![]()

Since I know you are so smart, and have a 401K, I am going to challenge you on your knowledge. Then I will show you my thing. I MEAN, my illustration, don’t get bad ideas. ![]()

A challenge. Try to loan 80% of your 401K. Better yet, don’t pay it back if they loan that money to you. Please, do so, then come back to me ![]()

![]()

![]()

![]()

![]()

Now, the second challenge: Invest in any index fund. Borrow-loan 80% of it but keep the 80% there. Come back to me with the results. ![]()

Then, the third challenge: count your $ in the 401K. Then, visualize this: You invested your money for 30 years, you got $500K-$1M. Deduct 20% for taxes, don’t go to add up the 34 different fees you have been subject to during those years. Then, think…think…“can I retire with the same amount year after year until I die?” ![]()

![]()

Oh, I forgot, there’s 2 of you. The challenge goes for the two twits of you ![]()

Oh boy! Some people are really so negative or ignorant, I have to show them how they can get free money when they are big shots in this arena…they say. ![]()

![]()

![]()

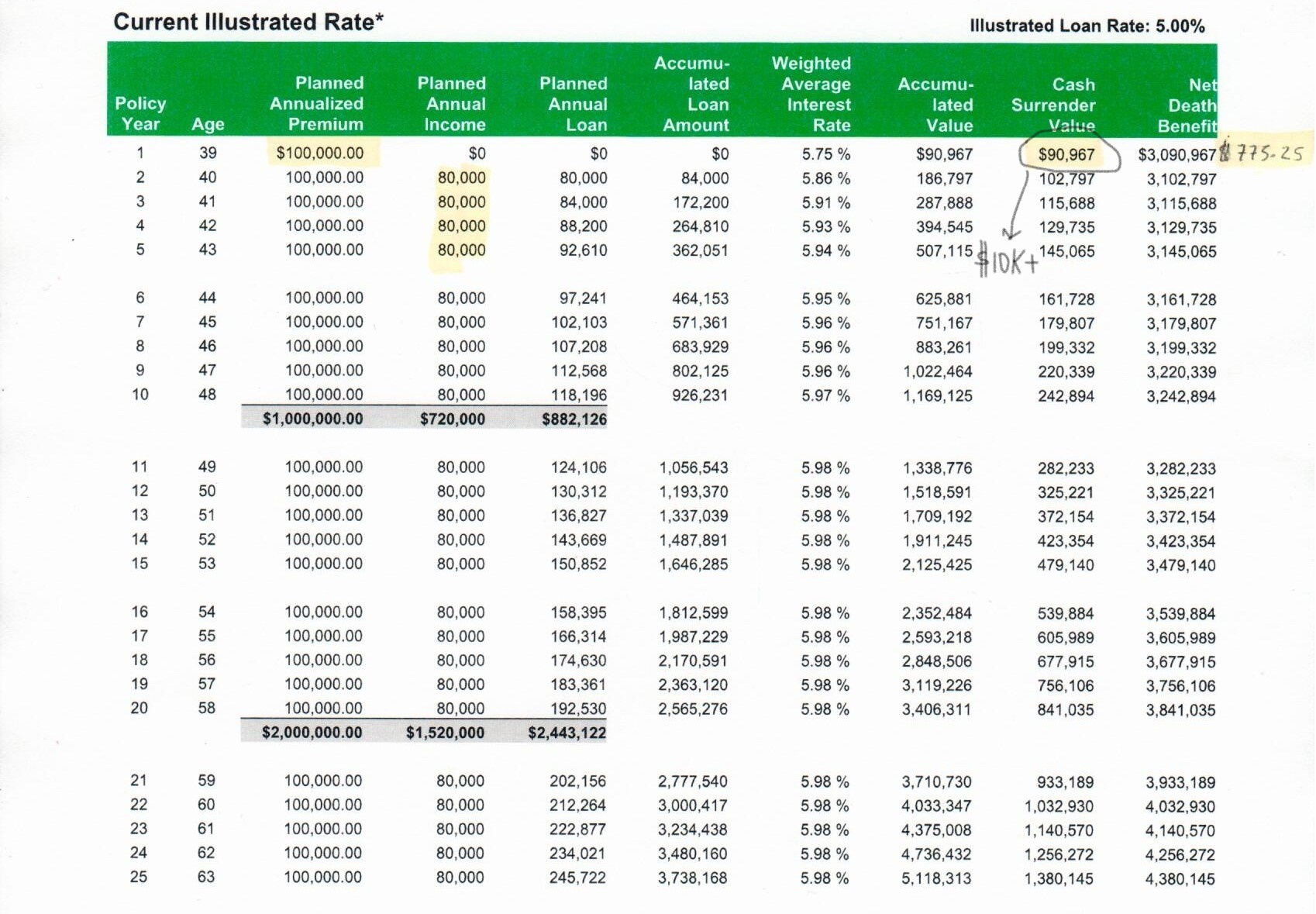

Here it goes:

Look at line or row #1. Supposedly, our client is loaning $80K, as established on the illustration. But, gee! He can loan $90,967 We suggest to leave that money there for “emergencies”…Guess what? As per the contractual agreement, the insurance company is obligated to increase the net death benefit. This client got almost $11K free, first year. With that money, he can pay the simple 5% interest of $80K. Wait! 2 years! ![]()

Next year? He gets more than what he can loan. I am not going into details, my head hurts explaining all the fine print and blah, blah, blah. The illustration is running at 7%, why not at 6%. Who cares! The battle between compounding and simple interests is a lost war for the simple interest. Proven!

I forgot to mention it: The loans are paid for by the net death benefit! ![]()

![]()

![]()

I will repeat: Loans are paid for by the net death benefit at the end of the life of the individual.

But simple interests, blah, blah, blah! Jesus! A debit card on your name, free money!

Do you get it? You put $100K a year into a policy, after I don’t know, 10 days, first month is tricky, you loan 80% of it. You are basically “investing” $20K instead of $100K. You get $80K in your hands, and another 80% in the stock market. Such money is invested by the insurance policies, we as agents don’t have anything to do with it, but asking the client to choose the strategies he likes.

The real thing is that you are so desperately trying to make this product look bad, when it is used by business owners to leverage their expenses. They don’t have time to play Warren Buffet with the stock market. They want a conservative approach to retirement. The stock market crashes, their money in that account-policy is safe. It has earned enough money to pay for loans made from the policy. Why loan if you don’t need that 80%? Don’t want to pay simple interest on a loan, don’t loan money! Gee! Keep it there then!

Even the most jumbling mumbling looney in the asylum would understand that.

If you didn’t get it this time, sorry, I don’t have cure for brain diseases.

By the way, did you know that even if you paid 7% simple interest on a 7% compound interest, compounding beats simple interest?

Simple Interest Formula

Lets say that P is your starting principal (spelled -pal and not -ple, because Your Money is Your Pal), r is the interest rate (expressed as a decimal), and Y is the number of years you invest. Then your future value will be:

P (1 + rY)

(Simple Interest)

P (1 + r)Y

(Annually Compounded Interest)

Note the two formulas give the same answer for one year. After that, compound interest takes off.

Quoting so you can’t delete it. The loan interest is compounded. I really don’t need to say anything else, since that disproves most of your post. Then you resort to personal attacks, since you can’t argue the math.

1 Like