I am glad you did.

Just don’t show any “emotional reaction”, a pathological and narcissist guy may notice you. ![]()

![]()

![]()

![]()

I am glad you did.

Just don’t show any “emotional reaction”, a pathological and narcissist guy may notice you. ![]()

![]()

![]()

![]()

Geez, money is not lost, it has to go somewhere. If USG is not getting it, someone else did. Then what do that someone do with it? Buy gold and keep in the bank? Buy houses? Buy stocks? Start a business? Spend on sexy toys? The most important for economy is churn rate… money moves around around around around. What we don’t want is stuck in one place, worse out of USA.

Btw, I have changed to shares not RSUs.

Somebody is going to get the money, sure, not you.

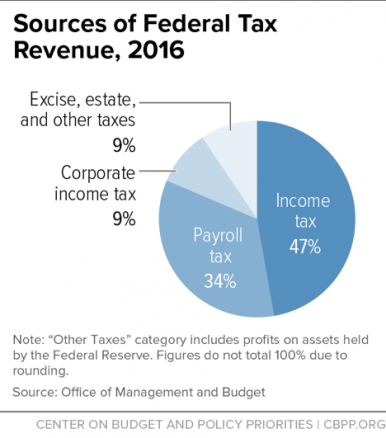

Corporate taxes are a small part of the tax revenue puzzle.

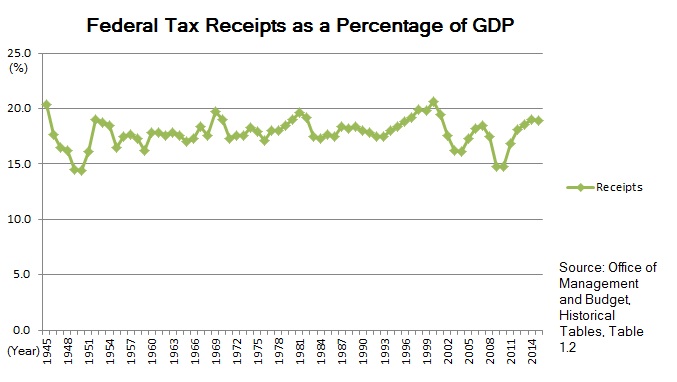

Taxes collected as a percent of GDP is pretty constant. It’s a little higher during booms and declines a little during recessions. Stock market gains matter in the scheme of taxes collected.

So when are you selling your house and using all the gains to buy a life insurance policy? You’re wasting time by not doing it right away.

Foreigners don’t pay taxes from American companies’ dividends. They don’t pay any taxes to USA on profits from stock sales either.

Retirement accounts also don’t pay taxes on dividends and stock sales.

And then there is the matter of tax rate, and how much is corporate tax cut translating into higher stock price.

I have never seen any “reservation of tax revenue” theorem. It’s not physics. There is no equivalent to reservation of energy.

I use my favorite phrase, “only an idiot” would say that because I already have one, my wife too, one for each of my kids for college, not the other worthless type. But if I didn’t have one, I would take only $300 a month and put perhaps another $2K to be loaned immediately with a 6% interest on the loans instead of wasting it in property management. ![]()

![]()

![]()

![]()

But you wouldn’t know that even though I explained it for 20 times. Did the midwife drop you when you were born? ![]()

![]()

![]()

![]()

Thanks for playing! ![]()

Now you getting it… too complicated for us to assess… we’re talking soldiering on paper.

I said it before, you ain’t going to get the money. The sharks in the swamp will.

So now you admit that they charge you 6% interest on loans from the life insurance policy.

I rest my case. This guy was dropped by the midwife when born.

Stop being an idiot then. As I recall, being called a walking fraud is what? I am telling you dummy, you really are a mental case!

Jil asked me where the interests charged to the loans were and I pointed at them 2 times.

Please, if you have a life insurance on you, throw it away, it is a waste of your $ or your boss’s money. You are already brain dead.

So would it have been that hard to say if someone takes a loan from their policy they are charged 6% interest for the loan? I think 6.14% was the exact number.

Deflecting again?

You were complaining of being personally attacked and I gave you the reason why.

It was so easy to say: Sorry dude. But that’s not your style. Your personality is of a bot.

Key word: Fraud.

Put something in that feverish brain of yours. I don’t manipulate the numbers given in any illustration, it is what it is. You like it, good! You don’t like it, good! But don’t come up with stupid accusations of fraud being committed. There are 27+ pages in any illustration with the caveats and whatnot.

**THIS VIDEO IS FOR YOU AND JIL: JIL WAS SAYING INSURANCE COMPANIES USING “OPTIONS” WAS A BAD SCENARIO. WELL, WATCH THIS VIDEO, HE SAYS OPTIONS ARE USED BY ICs.

I LISTEN TO THIS GUY ALMOST EVERY SATURDAY.**

If after this video you come with stupid accusations, really, you are brain dead.

You showed a illustration with $0 loans until age 60. Are you denying the illustration shows $0 loans until age 60? I’ll let you answer that one before I continue.

THIS IS GETTING TO BE NOT ONLY STUPID BUT PATHETIC. AM I HAVING A CONVERSATION WITH A KID OR A BRAIN DEAD? ![]()

![]()

![]()

![]()

![]()

OK, listen kid, I am going to repeat this for the last time. Please, I repeat, please leave your IPhone aside, your hands out of your pockets so you don’t touch yourself anymore and open your eyes and your brain. Here it goes:

The cash surrender value 75%-80% of the premium (age and health will determinate it) is the amount you can "LOAN" every month or every year. In the case I showed, $3,400 premium, $2,800 loan, month after month. I explained that again and again! You just make a phone call to the IC and the money is back into your bank account where you proceed to pay your expenses, double whammy! ![]()

Jesus! I know you were dropped on the floor when your mom was going to embrace you for the first time, God bless her heart for having a not so smart kid, but this questioning without understanding what I repeated a few times has to end. ![]()

![]()

![]()

![]()

Don’t waste my time and your time, keep going because I need this time to go and commit fraud on somebody else ![]()

![]()

![]()

![]()

![]()

5 paragraphs to avoid answering a yes or no question. You accuse others of deflecting.

You’re avoiding the math that as soon as the person borrows the $2,800 they are charged 6% interest . That 6% interest is going to offset the 6.75% gains. That means if they borrow their gains are only 0.75%. They’ll never accumulate the value you show to borrow $400K+/yr at age 60. Telling people they can borrow the $2,800/mo and still accumulate the total in that illustration is wrong. That’s why your illustration shows $0 in loans until age 60. It’s why you spent 5 paragraphs deflecting and attacking me instead of answering a yes or no question.

I think I explained 5 times everything about the loan and whatnot and here you are, asking me to explain that process with yes or no? If you understood it, why did you come back with the "oh baby, the 6% interest blah, blah, blah. That wasn’t the question, wasn’t it? Who is in serious denial about comprehension?

You can live in your world of negativism and lack of empathy for the human kind, well known on this forum by everybody when you respond, as if being on the opposite of what they say is the norm, when you bring your stupid “data”, that’s why I called you narcissist or psychopath. Nobody has seen you “smiling, or cracking a joke”. Something is wrong with you, you haven’t noticed it, but others have. You must be one of those perfectionist arseoles at work everybody hates, or the usual backstabber. Go ahead, say anything about me, I will be laughing my arse off. Will you?

On the topic.

Let me be clear here: The American language is funny. The first thing you learn as a foreigner is to insult and I am pretty accustomed to that, being called an idiot, stupid, dummy, even “spic” by black people, and not in a jokingly manner, are words not affecting me at all. Is the language of common, normal people. But, when somebody attacks my integrity, and calls me a fraud because he can’t admit his ignorance on the subject in discussion, in my world, I easily call them back mother fuckers, and if they are nearby, they will meet my fists, I don’t care if I am going to be beaten to death, but I will defend my honor. So, don’t cry wolf, don’t play innocent here, you came out unscathed by me after calling me a felon or a criminal.

I am not here to show you the mathematical equations or calculations behind the illustration. I can’t do that, I am not a techie to change anything, the numbers shown are assumptions of what the returns or income will be if the market is going at 7%, which I believe is in the 14% as of today. We follow a procedure, name, age, alleged health condition, we input some things as strategies, riders, and the rider we are using, the one that allows the loan of your money in a matter of days shown in this illustration is one of the best in the industry, no other company has it. We can change premiums, lower or increase them, even increase the extra premium for what we are not paid, but that gives us more referrals. We can schedule when, or how you want your income, the option A or B, etc. The IC company’s system gives us the illustration, and for you, again, to call me a fraud is just signs of desperation or signs of being incredulous, which is fine, we all suspect of something, but come on! This is not a piece of paper where I wrote an equation and that is the law of the land! Gee!

You expect everything to be explained in the illustration. It is approved by the state. All expenses and whatnot are already into the equation. Charges or income and whatnot can and will change based on the stock market crashing or doing better than today. Past results don’t mean the future will be the same. That is something, not even the 401K people can assure you. All we know is that our people won’t lose a penny the day the market crashes. Good luck if you are on the other side. Which you are, and big time!

As in anything, life insurance is based on uncertainty, nothing is predictable, otherwise it wouldn’t be insured.

So, now, go ahead, tell me, would you like to be known as an idiot or as a walking fraud?

I rest my case.

Now, check that video and go ahead, trash it. Everything is there. Show your ignorance, I don’t care.