3 Likes

Most of the time,

Forecast = garbage as in GIGO, enough said ![]()

Do you think the same for AAPL? Will AAPL order book be reduced by 25% next year or increase 10% next year?

Two points,

Is why don’t over dependent on FA especially quarterly result or single year result. More critical is corporate governance ![]() , business practices

, business practices ![]() and moats

and moats ![]() . Btw, speaking from a buy n hold (hopefully forever) investor’s perspective.

. Btw, speaking from a buy n hold (hopefully forever) investor’s perspective.

Consumer staples are more stable, is why WB buys mostly consumer staples stocks. AAPL has become a consumer staple ![]() around the time BRK started invested in it.

around the time BRK started invested in it.

Irony: we can’t tell what Fed would do next meeting yet we think we can forecast what discount rate to use for 10 years? Discount rate would magically stay constant for 10 years when we want it to be?

Instead of answering my question, you went blah…blah…

I pity you…even the young people in Reddit trying to learn proper way !

I have answered you in the first sentence. Doesn’t matter (thought was obvious so is silent, guess I should be explicit and start with those two words). The rest of the para is to elaborate why I said so.

Exactly, when I was young, I learn the “proper” way as taught by literature and experts. Now I threw them away because I realize doesn’t matter. I have past that stage ![]() Soon those young people would graduate from the “proper” way

Soon those young people would graduate from the “proper” way ![]()

In case you still didn’t get the message, what you are learning about FA and macros, I have learned long long long ago. I recalled you said you have started learning these about 5 years ago. But I have learned them much longer. To you, you have discovered a new toy, but I have played and discarded it ![]() Please don’t stop posting those because of my view, I sense many bloggers are still relatively new to investing, they would appreciate your posts. I am just presenting an alternative old man’s view

Please don’t stop posting those because of my view, I sense many bloggers are still relatively new to investing, they would appreciate your posts. I am just presenting an alternative old man’s view ![]()

In short, I have used FA for decades and conclude that most of the time is GIGO.

1 Like

Yesterday, CRWD crashed; today AH, SNOW crashes. Data Cloud (e.g. cybersecurity, database, data analytics, …) segment is too clouded.

What a beast. 67% rev growth and 165% retention.

1 Like

AH is a crapshoot. It’s already back to today’s opening.

1 Like

Another monster.

1 Like

Market values ZS (20B) with 53% eps growth for next 5 years. Potentially, when next stock crash happens (S&P to 3000 range), This may be around 2B-5B range.

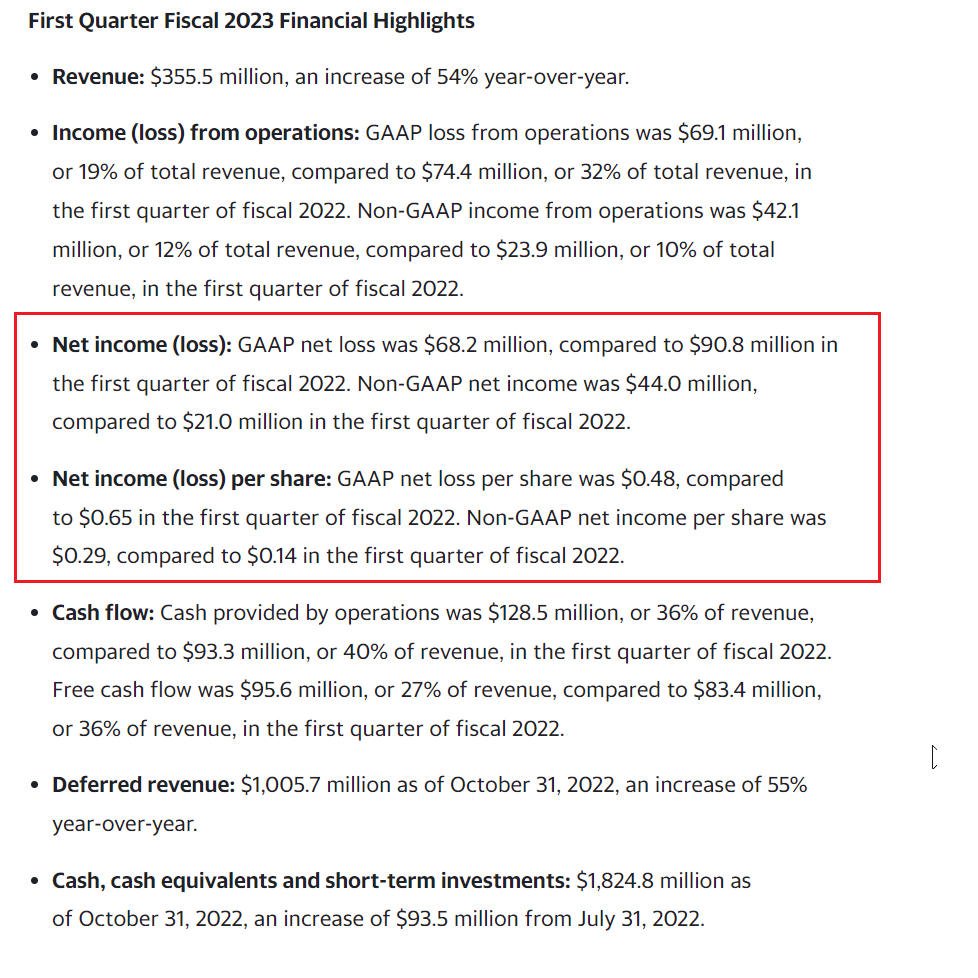

Look at this absolute level financial information, it is a loss making. Assume this way, this is a rental home bought 2-3 years before, so far made negative cash flow, will it survive next 5 years. If survives, what will be its worth?

With increase in rate, many companies, using hired cloud environment, will file bankruptcies (all contracts cancelled). The ZS security revenue rollback to deep negative. Unless some company takes over ZS, they won’t survive next 5 years.

source: Zscaler Reports First Quarter Fiscal 2023 Financial Results

2 Likes

Few years later, left with 1-3 cybersecurity stocks. PANW, …

Okay, here are the information we need to account.

Last 5 years, cloud companies are in limelight. They keep the product & services at cloud, and open up to market to subscribe cloud resources.

Every new small to big businesses contract with cloud companies, subscribe to them monthly payment basis.

For example, if I want a server or computer previously, I need to pay $3000 or $6000 purchase price, but now I just need to take cloud server between $30 to $100 for a month and keep using as long as I am operating the business.

If such new small to big companies are suffering losses due to Rate hike and leading to bankruptcies, they try to cut cost by lauy off, next cancel cloud contracts…etc and finally file bankrupcies.

This means, when businesses are filing bankruptcies, it impacts all their subscriptions, that affect many cloud companies.

The revenue and income is cut off and potentially debt ridden cloud companies may even file bankruptcies.

You may not see them after few years. Buy only strong profit making and low debt companies at this recession bottom (do not compare the peak price there were pre-recession time).

Few places to check.

- Are they making profit last 2 qtrs?

- Do they have debt and how much compared to market cap.

- What is their next 5 years EPS growth? If it is above 10% growth, be careful market priced in.

3 Likes

.

Can be deduced from earnings from AMZN GOOG MSFT.

Very few Dotcom companies from dotcom era still around. Expect slightly better for SAAS cloud companies.

1 Like

I love how you mix earnings of a company with cash flow from a rental. You highlight the earnings while ignoring the cash flow below which is positive.

It is an example only just to co-relate the situation with real estate. It is not my intention teach all financials !

Investors need to find whether such company can survive in future or not.

The core idea is that people should not account how high it went in the past.

Take for example TLRY went $315 peak, now selling at $4. Will it have potential to go back to $314? It depends on future returns/fundamentals

If you’re evaluating survival, then cash flow is what matters. Earnings don’t.

In financial evaluation, it depends on various factors.

I can show some hypothetical examples, Ponzi scheme company, where a company owns big term loan, cash flow positive by depreciation write off, but profit negative 99%. This company eventually file bankruptcy at some point of time.

Like this we can go one endless debate!

If someone wants to know financial side all permutation and combination, they need to go through Aswath Damodaran YouTube pages as he is posting all his classroom lectures free.

Unfortunately, I do not want to go endless updates, but I stop here now.

A good post asking the 100 billion dollar question, will SaaS companies lower their 2023 guidance? Crowdstrike lowered, but Snowflake did not. Most companies won’t say anything on their 2023 guide until the next earnings report in Feb-Mar next year.

Interesting plot on multiples vs growth:

![]()

U and S are cheap by this metric, and SNOW expensive.

4 Likes