Overall I feel there are too many FinTech firms around, and most of them offer broadly the same things. Like what is the difference between Shopify Pay vs PayPal vs Amazon Pay vs Zelle? SoFi has some loan products but where is the tech? All are based on existing bank and credit card infrastructure.

UPST claims to have some unique sauce to evaluate creditworthiness but whether it is better than the good old credit score remains to be seen. Anyway banks’ appetite for loans have significantly shrunk since JPow raised rates to the sky.

New industry also start this way. Then emerge the stronger ones that would acquire the weaker ones and many fade away. Look around…

Home Depot, Lowe

iPhone, Android

MCD, Burger King

JPM, BAC, C, WFC

…

After night is day

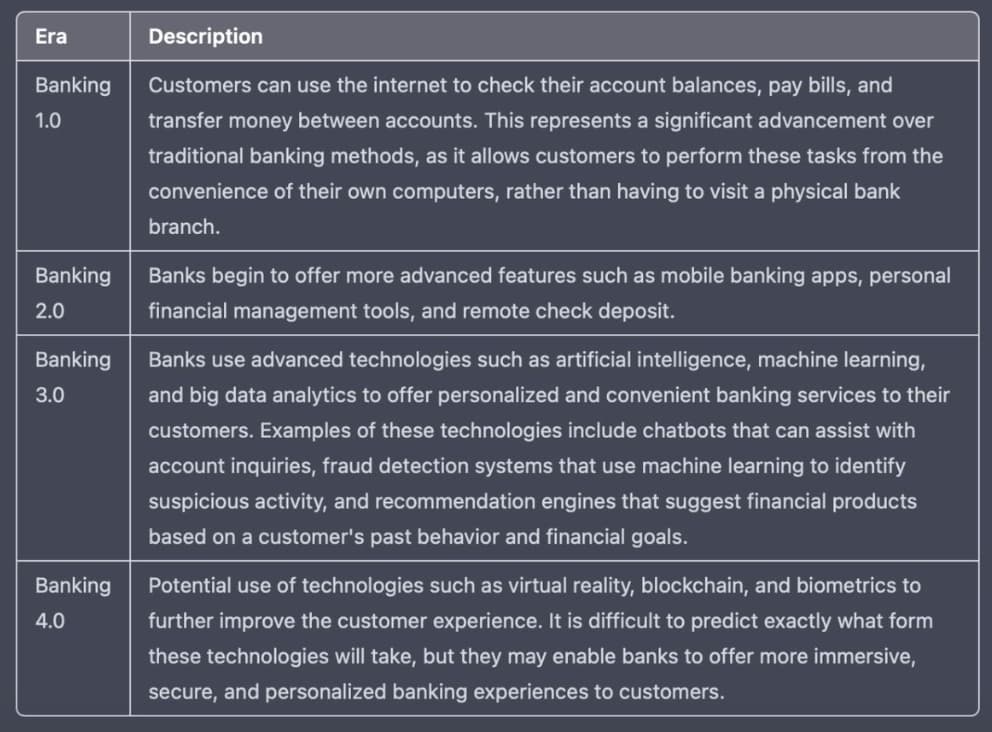

SOFI has many tech, read up… eg Galileo

Toll booths MA and V

Btw, I also think there are many NET alike around yet you are comfortable with NET Is because you have made up your mind to invest in NET and not to invest in FinTech. What you are doing is rationalizing your decision.

There is no sure way to determine the eventual winners

Mission: Help individuals to achieve financial independence

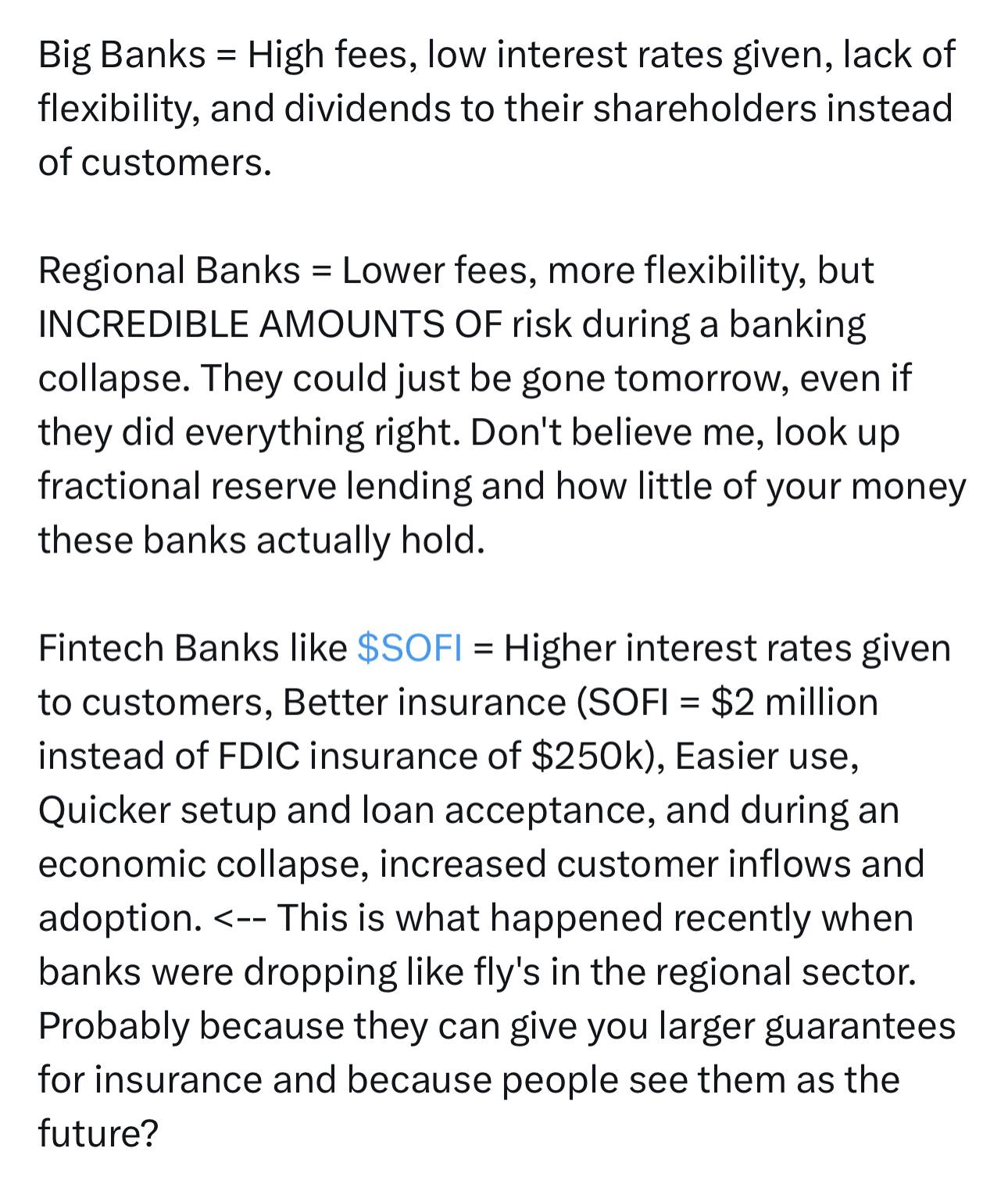

SOFI = Online bank + online insurance company so no physical presence (overheads).

ST, in order to compete with TBTF banks, behave like regional banks… offer high deposit rates. Haven’t figure out how it is planning to achieve its mission.

I honestly don’t get the SOFI model. They use AI models to evaluate risk and offer customers loans at lower interest rates. Then they also pay higher rates on deposits. Their net interest margin has to be worse. Then there’s the whole issue of their AI model evaluation of risk vs. existing models. We have TONS of data on FICO score and risk. These new risk models work great until there’s a downturn and increase in unemployment. We already know that from 2008-2009 when MBS were repackaged and sold as AAA bonds.

I also don’t get it. But gen-z and millennial swear by SOFI to be the next TSLA. Super hot with them.

Bot just a starting position. Continue to do more DD to decide what to do next.

May be can afford a lower margin because using AI and no physical overheads. I am trying to figure out how they can grow to compete with the TBTF banks. So far, feel more like an online regional bank.

AI is expensive to train and run though. I’m skeptical the AI model is cheaper than paying to run FICO scores. I suspect it’s a lot of hype with no substance.

I’m out surprised young people like SOFI. They get easy access to credit with better rates. What’s not to like about that? I think most of these fintech firms will fail the first time unemployment goes over 5% for a sustained period. They got lucky in 2020 because the government helicoptered money everywhere.

These “AI models” were products of the zero interests rate era when banks competed to lure customers to make loans, because free money were flooding into the banks. Think SVB. They tried to justify making loans to people with no or bad credit history. That never ends well.

I won’t touch these “AI loan model” companies with a ten feet pole. Chances are their models are 1) bad and 2) have nothing to do with AI.

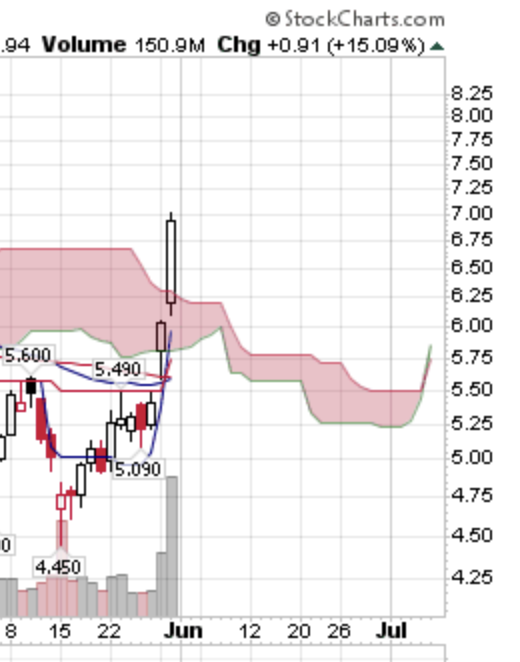

IMHO, SOFI is in Intermediary degree (multi-week) wave iv as depicted below…

Max decline for wave iv.(a) is $8, if go lower, my count is invalidated. Walking the talk, I bot into SOFI that I have sold below $8 (yes, I am an idiot) that I have bought for less than $5… then I was thinking is completion of Minor degree (multi-day) wave (1). $10.23 could be completion of wave (1)… tentatively label as wave iv… will adjust if necessary according to next 1-2 week price action.

Partner with banks… I believe is regional banks Personally, I don’t know why individuals want to hold so much though. Btw, in term of growth and profitability, is not as fast as NU (BRK/B owns a sizeable position). I didn’t invest in NU because it is HQed in Latin America… ditto for MELI. However, customers of SOFI is of high quality (have much higher salary than NU… mostly graduates).