4x gain I.e. 300% over 8 years. 2.5 years of that was in cash, so essentially 5.5 years.

1 Like

Cash is also an investment, low risk and low return

Is your stock return better or worse than your RE then?

Disclaimer: no personal info will be accepted

I think it is wrong to focus on return too much. The important thing is to participate, and participate in large volume. If you put $1M into the stock market, then all you need is a 11% return which is enough to beat a 100% return on a $100k portfolio.

2 Likes

Hmm, this is a novel perspective. I would rather owning a 100k portfolio that doubles every year than a 1M portfolio that increases 11% per year.

You took my example way out of context. Why would a 100k portfolio perform 10x better than a 1M portfolio?

What I meant was that the more you put into the stock market, the less you need to chase for higher returns because even mediocre returns can result in huge gains if your portfolio is big enough.

So you should really re-evaluate your situation here to see why you haven’t been successful with stock investing? You just need to add a lot more capital into the market to make your money work for you than the other way around.

Savings is the first step. If you save and invest, then compounding goes to work for you. If you spend and borrow, then it works against you. The vast majority of Americans spend and borrow. That’s why median retirement savings, savings, and net worth numbers are so low. Meanwhile, household debt keeps increasing.

Savings and spending is a separate topic. The question is RE vs stocks, and it is hard to gauge the actual stock performance. Are most people on this forum double, triple SPY over 10 years?

The published audit of many stock portfolios show a much lesser performance than claimed. This forum could be full of extremely successful outliers

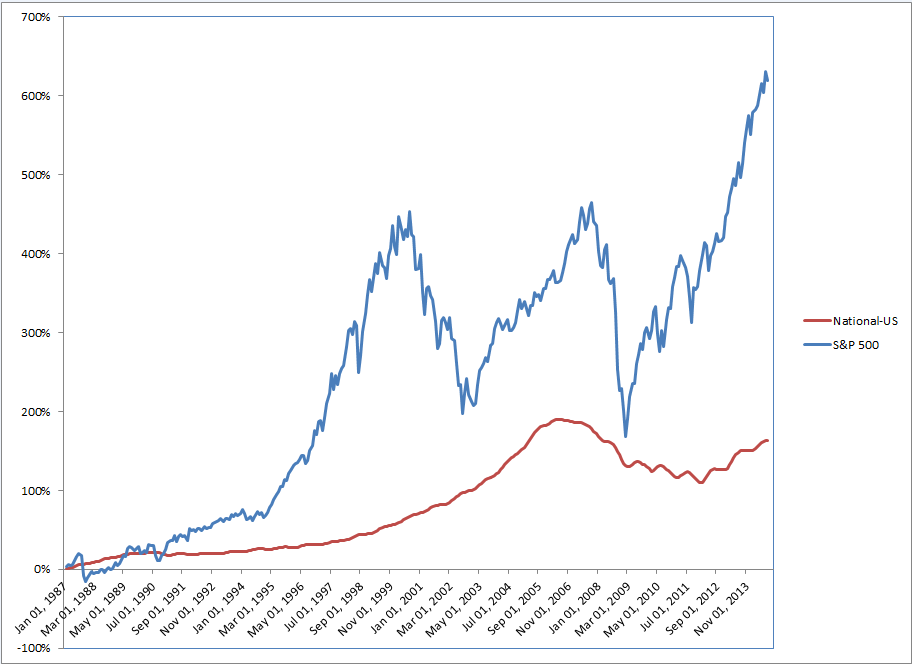

You’re also cherry picking RE by only considering the bay area. If you want apples to apples, then compare SPY index to national Case-Schiller index. That removes investment selection and looks at performance of the entire asset class. Individual returns will vary based on the skill of the investor picking the investments.

2 Likes

LOL…I don’t have to prove anything. Try do discredit the guy above, I am not the one putting him on a pedestal, the people trusting him and paying him lots of $ to do so, do.

Insurance fees go steadily, not increasing. That’s why we use a rider that makes the chargers be lower because we allow the insured to put more money into “corridors” to not go into MEC, and for that we the agents don’t get paid that much.

Does 401K gives you living benefits, if you know what that means?

Does 401K leaves your family with an extra amount of $ if you die, tax free?

Does 401K allows you to take home 75%-80% of your own money, tax free?

Does 401K avoids the risk of the stock market as in 2008-2009?

Now, I would be a stupid person trying to fight the mathematical calculations on an illustration as you did last time saying your numbers didn’t add up. Really mister Einstein? That means, you know better than the high techies doing those numbers and the department of insurance approving them?![]()

You better find out if the DOI is hiring high techies, you may be of a good service to the people, insurance companies are ripping people off and 401K is not. ![]()

But, I know, your ignorance is outstanding, and my English is not that efficient to make you understand. Read the following, you may, I repeat, “you may” understand. I will use the Roth Ira as an example.

Google ROTH IRA OR IUL.

By David Mcnight.

The Roth 401(k) vs the IUL

This of course begs the question: Is the Roth 401(k) really less expensive than IUL? Comparing an IUL’s fees to traditional tax-free investment accounts can be a tricky proposition, especially if you fixate on first-year expenses alone.

Let me illustrate with an example. According to USA Today, the average expense ratio of a Roth 401(k) account is about 1.5 percent per year. So, if you make a contribution of $10,000 to your Roth 401(k), your first year expenses will be $150. Conversely, if you contribute $10,000 to a properly structured IUL, your first year expenses might be closer to $1,500.

Based on this comparison alone, the Roth 401(k) seems the obvious winner. But comparing first year account balances hardly tells the whole story. Here’s why: The fees inside the Roth 401(k) are low when taken as a percentage of the first year’s balance (in our example, 1.5 percent per year), but when measured in actual dollars, the story changes dramatically over time. For example, if that $10,000 Roth 401(k) grew to $100,000, the annual fees would jump from $150 to $1,500. If it then grew to $1,000,000, the annual fees would balloon to $15,000. In other words, the more money you accumulate in a Roth 401(k), the more fees you pay.

Contrast that with the ongoing fees of a properly structured IUL. Generally speaking, when an IUL is structured to maximize the cash accumulation within the growth account, the fees stay relatively level. This is accomplished by buying as little life insurance as the IRS requires while stuffing as much money into it as the IRS allows. Under death benefit option 1 or A, the amount of insurance you have to buy under IRS guidelines actually decreases as your cash value accumulates. Even though the internal cost of insurance is rising, you’re actually buying less of it as time wears on. This keeps the IUL’s fees relatively stable over the life of the program.

Even though the fees in the IUL are stable, they grow smaller over time when seen as a percentage of the overall cash value. For example, when an IUL account value grows from $10,000 to $100,000, that same $1,500 fee now represents only 1.5 percent of the total account value — the same as the Roth 401(k). When the cash value of the IUL reaches $1,000,000, however, that $1,500 now represents only 0.15 percent of the cash value. The following chart demonstrates the IUL’s cost-effectiveness over time when compared to the Roth 401(k):

And the winner is

So, given a full accounting of fees over the life of both programs, which alternative is the least expensive? By looking at the trajectory of fees in either scenario, it appears that, given enough time, the IUL eventually wins out.

But how can we be certain? A surefire way to determine the least expensive alternative is to perform a side-by-side comparison where you contribute equal amounts of money to both programs over a fixed time period (say 10 years). Next, distribute tax-free dollars from both programs for another fixed time period (say 25 years) starting in year 11. Be sure to apply the 1.5 percent expense ratio to the Roth 401(k) while letting the life insurance illustration system account for the internal expenses of the IUL.

In most cases, you’ll find the IUL can distribute tax-free dollars just as productively as the Roth 401(k). Equal distributions, by definition, mean equal fees. In fact, when you run the internal rate of return (IRR) on a properly structured IUL, you’ll find that its annual expenses, averaged out over the life of the program, are around 1.5 percent.

http://www.thinkadvisor.com/2014/08/27/the-roth-401k-vs-the-iul

I showed exactly why the math was wrong. If you could understand the math, then you’d have been able to follow.

So you post one source saying UIL fees are flat, and a second source saying they average 1.5% of account value. You can’t even agree with yourself.

Is there any comparison using SPY and Cas Shiller index? But there’s no rent info. Actually most comparisons ignore the rental income or the equivalent rent a stock investor pays.

Most of the financial literature favors stock investment by ignore the equivalent rent a renter or homeowner would need to pay

number?

Wrong to focus on return in %, should focus on absolute return ![]()

This says stocks. I think most people agree a primary home should be top priority. The question is what to with additional investment money.

2 Likes

Where is the rent for the house?

What’s the absolute return? Dollar amount?

Is the $1m return on $1B portfolio the same as a $1m return on a 100k portfolio?

You’d have to add it. You’d also have to add your expenses to get a a “dividend” equivalent. I think that chart excludes S&P 500 dividend reinvestment. It’s must the change in value of the index.

LOL…You can’t beat the illustrations math, they are sanctioned by the DOI. Stop playing dumb, you are out of your field of expertise. Period!

Flat and average, who cares. You implied costs were 2-5%, so, who is the loser here?

Also, learn about COI and commissions. You are out of your league here.

Oh…I bet you have a life insurance, tell me, which one is it? You wouldn’t be having one if you don’t trust them, right? ![]()

![]()

![]()

![]()

It’s easier to invest $1M in real estate than stocks. To invest $1M in real estate you just have to come up with 25% down or $250k for a rental. You can borrow the rest.

To invest $1M in stocks you have to come up with $500k up front, and borrow 100% margin to $1M.

I think most people would feel very confident with 25% down to buy a house, but if they have to dump $500k into the stock market and borrow another $500k margin they would probably be losing a lot of sleep every night over it…

1 Like

Exactly. That’s a real reason that RE is better for most folks. Theoretical stock return is not so real

The math you posted was wrong. I actually posted the correct math. Who knows what you did to create that table.

You were pretending there’s no fees or commissions for UIL and trying to scare people with how high 401K fees are. The truth is both fees are about equal, so who’s the liar?

Anyone with a real job has life insurance, disability insurance, dental, vision, and healthcare (that’s much cheaper and better than exchange plans). If I want to increase my life insurance to $1M, it would cost $41.30/mo. They guarantee the rate and coverage if I leave the company. The policy pays out on a terminal diagnosis. Plus, I have disability coverage, so if I’m disabled I’d get 60% of my base pay for life. So I could take the other $958.70 a month I save by not buying your UIL and invest it. At 8% a year, I’d have $1.26M in 20 years.