My wife and I both work at FANG, early 30s with 1 baby, current house already have decent school. Let’s say we have 0.5m cash in hand, and we can still take another 1m mortgage roughly. What will you invest? I mean, I really don’t see any other better option. I did a really bad job on stock trading, and not to mention the couple of hundred K I loss in Bitcoin. Seems like buying an investment house is my best option.

So, should I buy a SFH in bayarea with 1m mortgage? Or I should buy 1 or even 2 SFH in Austin or any other good locations? One of my friend brought a SFH in Huston,TX, 2100 monthly rent for a sub 300K house seems like a good deal. I don’t think you can find any better cash flow in bay area. Of course, property tax is one issue.

Why Austin, you wanna ask? Because, I think Austin is the only location I can live in TX other than becoming a bacon in the summer.

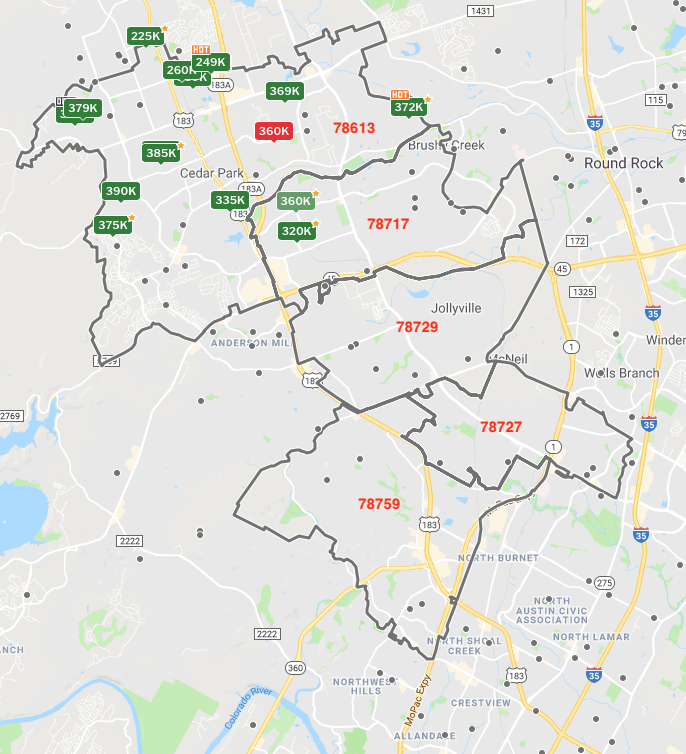

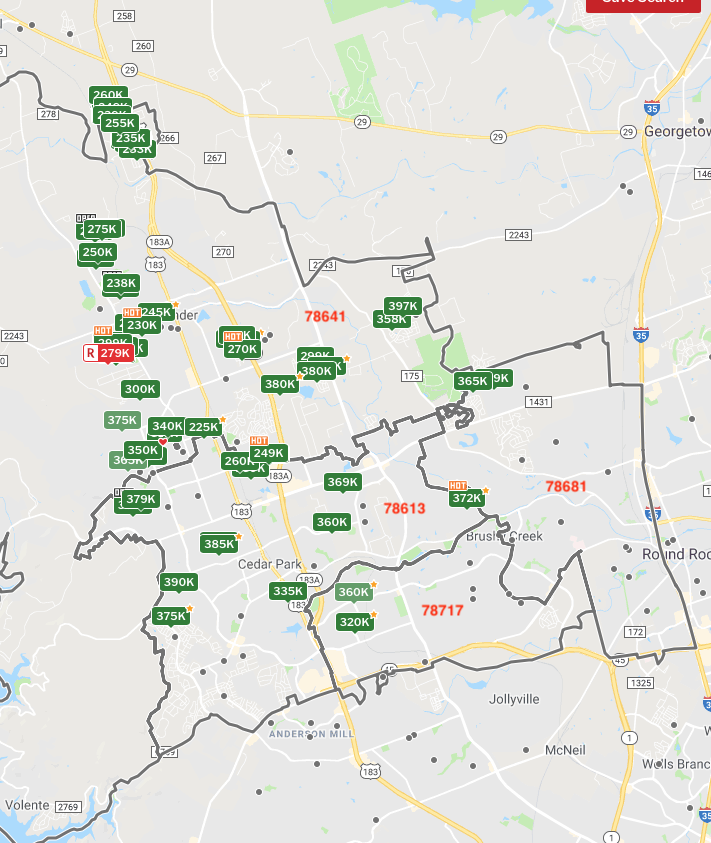

Unfortunately, so many Californians went there to buy that hardly any good rental potential for sale. Below is a map of hot zip codes with prices less than $400k.

I would stay in cash or park in an index fund till the fog is clear. Stock picking and RE rentals are risky in current environment for newbies.

Lurkers are not bloggers. Most don’t give you complete picture*. Take it with a pinch of salt. Tell them you only want to know annual rate of growth of their net worth. Not interested in success in individual stocks and rentals… selected for entertainment and bragging rights only. Did their net worth grow faster than 11% (S&P index) on average over a long period of time or faster than current annual growth rate of S&P?

*For example, 10% appreciation per @wuqijun is not the same as 10% appreciation per @manch.

For me, I am very conservative in computing return. Say, I have $100,000 in an account/portfolio, invested $10k in a stock, gain $20k. My annual return is 20%, and not 200%. Just because I invested $10k, it shouldn’t be used as the denominator, it is the allocated amount that should be used to compute return of the account/ portfolio.

Before even buying index funds, he needs to take 3 months time to study good investment blogs like this https://www.bogleheads.org/

Some elementary books

Beginner

-Little book of common sense investing by John bogle

-A Random walk down wall street by burton malkiel

-The boglehead guide to investing by Larimore, Lindauer, LeBoeuf

Too much reading, we are not getting an investment diploma!

Just find out the 5Ws of index fund and DCA purchasing is sufficient. Decide on whether want to do self-help or talk to a big boy (Vanguard, Fidelity, …) to set up the DCA into an index fund. Done.

Not required for investing in index fund Brain dead easy, hardly any effort, no need to read much, and fantastic average annual return of 7-11%.

Using @manch optometrist example, he started investing at the age of 17, and he is 79 years old, so 62 years of investment. For each $1,000 invested in S&P index fund, return is 1.11 to the power of 62 = $650,000. For each million dollar invested, $650,000,000! He earned quite a lot from his businesses, so not sure what is his annual rate of growth on net worth, for all we know is lower than index fund

Tell me his average annual rate of growth of net worth! Of course there are some real stories, I have a friend who make $30M from a few thousand trading options.

Assuming you are already maxing out your 401k, which should be all stocks or index funds, I think it’s a good idea to put the 0.5m into real estate. It’s not liquid, so it forces good discipline on you.

One SFH in Bay Area vs multiple in Austin, I think buying multiple is safer. I am not familiar with Austin in particular. I am just thinking along the line of say 3 separate rentals vs 1. If you put all your eggs into one single rental and something happened to it, you are screwed. It’s better to spread it around a little bit. Whether it’s Austin, Seattle, Denver or even Florida cities like Tampa or Orlando, I have no strong opinion one way or another.

As the original lurker, let me post in this thread. After swearing off buying anything this year (stocks or RE), I am about to submit an offer on a place (fingers crossed).

Why you may ask?

the numbers pencilled out

It was a relatively small purchase (risk is manageable) and I am holding for long term and was bullish on the long term of the purchase

I had cash sitting around and was debating between 2.5% tax free bonds vs this

I am currently in the phase of my career with a decent W2 income which lets me add leverage. Leveraging my income lets me buy cashflow positive RE with only a 30-35% downpayment

I don’t have the time or skills to be an expert at stocks like @Jil or @hanera , but RE is something that I have some domain expertise in.

Brain dead easy, hardly any effort, no need to read much, and fantastic average annual return of 7-11%.

Brain dead easy, hardly any effort, no need to read much, and fantastic average annual return of 7-11%.