Twilio is interesting. It owns the communication infrastructure on the cloud. I want to find out if Amazon will or can kill them off anytime soon. Probably not because it’s a lot of grunt work, and Twilio is hosted by AWS anyway.

MSFT has been in software and server services for a longer time since the days of Apple competition.

Amazon is new to cloud service, but it became leader (market share).

Now, MSFT catching up with Amazon means, they lost it already. Most of the MSFT software are enhancement or conversion of old versions to new.

Where as for AMZN, everything new, but they made it incredible speed.

“The findings suggest Microsoft is posing more competition to the public cloud market leader, Amazon. They come as Amazon and Alphabet’s Google release products that address a key area that Microsoft embraced before they did: “hybrid cloud,” which means customers can use a mixture of cloud services and software they run in their own data centers, and manage both with a common set of tools.”

MSFT got distracted by mobile and forgot where their strength is. At least it manages to recover not like motorola (semi, handset)… motorola employed too many engineers not enough business people.

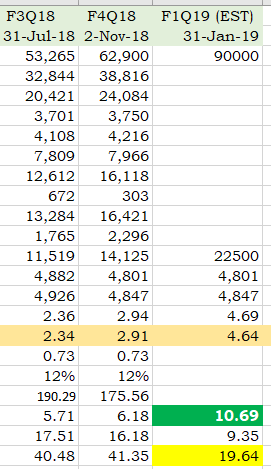

Added UBNT, If you forecast next 5 years, which will sustain and which will give better growth for you? It is pretty difficult to find out, but that is the best way.

My pre-scan ( not analyzed properly) pick will be UBNT and then VEEV (by seeing 19.6% and 21.2% Profit Margin) . Wait for some fall, grab the opportunity.

I recently watched BA went down to $309, but picked up at $315, good to hold long as this is established company, dividend payer, lot of US government and world wide orders.

If there is rate hike pressure is applied, many companies will vanish or struggle in future.

Read the pages 8,9,10,11 - possible four vulnerabilities that can result crash or bubble. That helps you to decide which companies are better (of course, you may know these by experience, he has spoken clearly).

If you listen to his 40 mins speech, he nicely put it. The above pdf is transcript.

Shares of Splunk (NASDAQ: SPLK) jumped 9.9% on Friday after the operational-intelligence platform company announced stronger-than-expected fiscal third-quarter 2019 results. In fact, this marked Splunk’s 16th straight quarter of exceeding top-line guidance.

If that wasn’t enough, Splunk called for revenue in the current (fiscal fourth) quarter to arrive at roughly $560 million, up 33.4% year over year and comfortably above consensus predictions for $557 million. Splunk also raised its full-fiscal-year 2019 guidance for revenue to be approximately $1.74 billion (up from its old target of $1.685 billion), and increased its fiscal 2020 revenue outlook by $150 million, to $2.15 billion.

Self-made billionaire Jerry Jones, who made his fortune in the oil business, bought the Dallas Cowboys in 1989 for $150 million. Today, his team is worth an estimated $5 billion.

not enough business people.

not enough business people.