another losing sj home:

https://www.redfin.com/CA/San-Jose/2261-Gunar-Dr-95124/home/1646398#property-history

Any guess on this… Its been on market so long now.

https://www.redfin.com/CA/San-Jose/1708-Grizilo-Dr-95124/home/851947

https://www.redfin.com/CA/San-Jose/1734-Balsa-Ave-95124/home/715497

https://www.redfin.com/CA/San-Jose/1708-Grizilo-Dr-95124/home/851947

1734-Balsa went pending in 2 week.

1708-Grizilo is in Willow Glen High boundary, less desirable than Branham high.

Also, smaller lot than 1734-Balsa but in better condition.

Probably, seller would accept offer at listing price?

It has been on the market for 24 days, not too long in my opinion.

However, previous sold history seems suspicious to me.

It was sold $100K under asking price in 2014.

In 2014, market was very hot.

Is it near high voltage power line or something?

I dont think there is high power line. I think it was in original condition when sold in 2014. It was remodeled after

The seller made 10x profit in 24 years.

Not bad at all.

I am not sure about buyer’s buying point though.

If the buyer wants to use it as primary, it would be better to look for nicer location (this is close to 6 lane busy street, facing parking lot of cambrian park plaza(one of the urban village location, meaning high rise building would be built soon), surrounded by 2 other shopping malls…).

If the buyer wants to rent it out since it has one main house(3385sf) and guest house(800sf), it would be better to buy 2 of 3br/2bath SFHs in this area with the same budget.

Maybe, buyer has other plan like demolishing the existing house and build something else in accordance with urban village plan?

In any cases, it is not really ordinary setting.

Not surprising that there were not many buyers interested in.

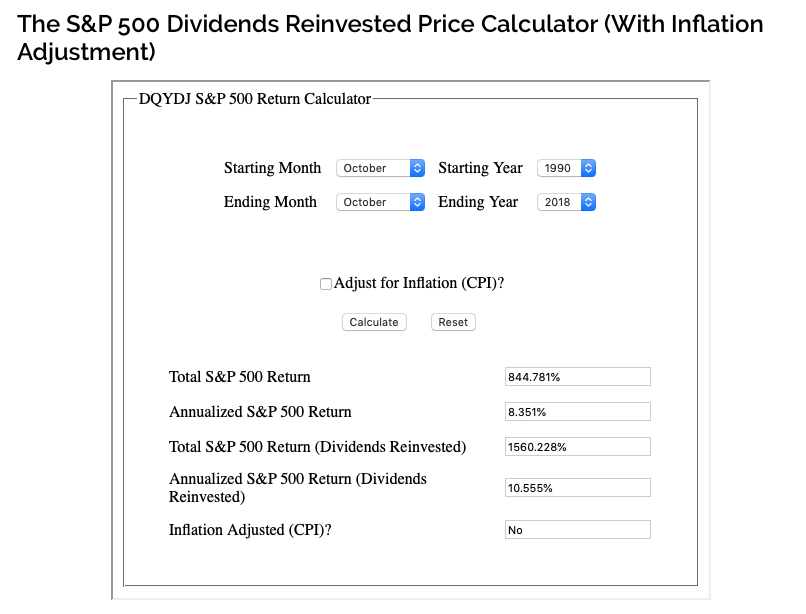

Historically S&P appreciates at 7-11% per year, at the end of 24 years, every $1 invested in S&P index becomes $12.24 ![]()

1 Like

I invested from 1990 till now didn’t get anywhere near that return in index funds. Pretty much nothing good happened from 2000-2012, except up and down aggravation

did you DCA? ![]()

Do you DCA yourself?

I put no money in between 2000-2012

@hanera, we are back to the rent vs buy argument from that Dropbox engineer. In that calculation, I saw that if housing goes up by 5% a year, it beat renting a Fremont home worth $950K. That time all of you said that it’s not realistic to expect 5% growth in housing. This particular home that @Jane is referring to grew at a rate of almost 9-10% a year in the last 24 years. With that kind of growth, renting is a loser proposition. It also beat index funds.

Computation of gain for RE is wrong. I have shown the computation twice.

1 Like

Yeah, involves cost on the loan, etc.

SP 500 with Drip.

The stock market went nowhere from 2000-2012

Idea of investing in index fund is decades or multi-generation. If invest for yourself, may not be that great as the timeframe might be too short.

That spreadsheet takes the cost of the loan into account. The key point is that, even if the house appreciates 3x or 10x, the loan is still 80% of the original x. So the whole 5% PITI is just on a fraction of the property value after a few years, but the rent is 3% of 3x or 10x (in Fremont today). I understand this is a simple view compared to the spreadsheet. The key here is appreciation. That’s why buying in the bay area matters.

1 Like

wow…

https://www.redfin.com/CA/San-Jose/1904-Creek-Dr-95125/home/1440655#property-history

Not a lot of appreciation, huh. from the images looks like terrible use of that lot size - backyard looks tiny. Redfin shows it kind of like river is part of the lot. maybe that’s why.