Lots of stocks out there. Tesla seems to volatile to bother with. Makes more sense to trade. Buy at $270 sell at $330.

My reasons to hold:

Elon had the dream of EV cars 10-12 years before and he drafted it, you can find it internet. His dream took 10-15 years.

What we see, presently, is his dream comes true, selling 80000+ EV cars in a quarter. This is the time, the stock must go up and stabilize as EVs will revolutionize the car industry.

With current price and production rate, chances of TSLA reaching 100B mark is brighter than chances of TSLA becoming 25B company.

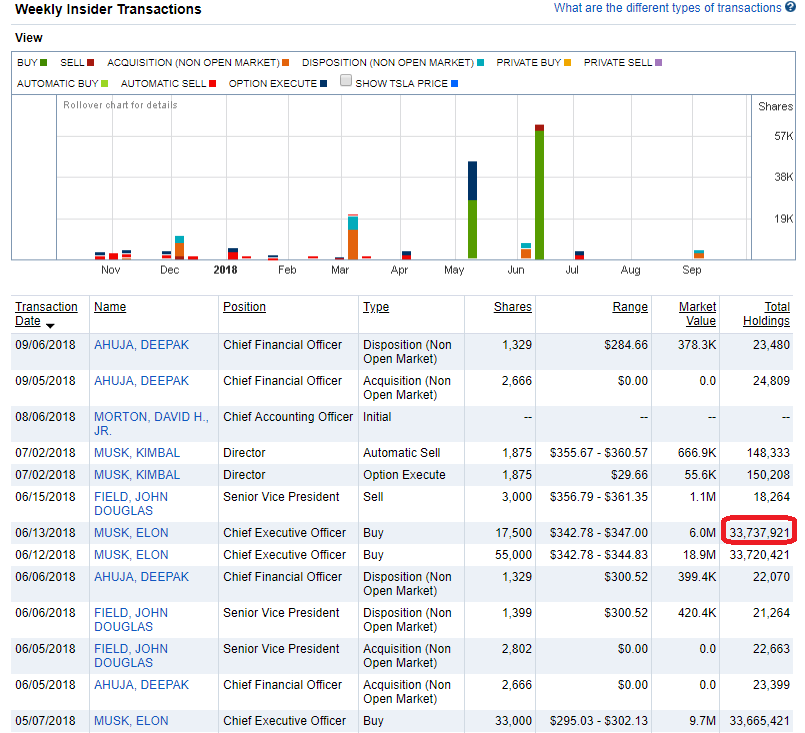

Holding is meaningful as real float of TSLA shares very low. See the data, the 37% other owners include Elon Musk’s 20% (I guess), balance is 17% is real shares float.

Chart is from fidelity.

This is probably the reason why TSLA didn’t go too low. Some1 is supporting it… is easy with small float. Elon wants to be the richest man ever so he would put in all he got.

1 Like

Volkswagen made 11M cars last year and has a market cap of 75B. Why selling 80K a quarter would take Tesla to 100B?

2 Likes

Who’s the CEO of Volkswagen? Nobody knows. Must be a really “shitty” one. Employees not only shitting on the toilet floor but maybe on those assembly lines too…

1 Like

It is the difference between main frame and tablet pc or Age 18 and age 81.

It is the EV transformation which is currently going on. EV cars are going to be the future unless an efficient technology comes.

EVs cars are almost 5 times efficient than internal combustion (IC) cars.

EV Fuel cost (3 cents/mile) is economical than IC fuel costs (20 cents/mile). I have driven so far 110000 miles using EV cars last 5 years.

Once we used to EV cars, we do not like driving Gas cars. Zeapelido already stated this , the same way I felt after using EV cars.

I have already posted this video (1 Hour) how future will be in 10 -20 years. He is one of the best visionary and also an investor.

(Tony Seba is the author of “Clean Disruption of Energy and Transportation”, “Solar Trillions – 7 Market and Investment Opportunities in the Emerging Clean-Energy Economy” and “Winner Takes All – 9 Fundamental Rules of High Tech Strategy“. Mr. Seba is a serial Silicon Valley serial entrepreneur, an instructor at Stanford’s Continuing Studies Program, and a keynote speaker. Tony Seba holds an M.B.A. from Stanford University Graduate School of Business and a B.S. in Computer Science and Engineering from the Massachusetts Institute of Technology)

I am waiting for the solar EV  No need to carry so many batteries.

No need to carry so many batteries.

That’s exactly my point all along. TSLA is all about Elon’s personal cult appeal. ![]()

1 Like

Lol: Yes, you buy Solar cars, I buy that company stock ![]()

I have no doubt about EV’s future. But we are evaluating Tesla the business here. At the end of the day it’s about how much cash you can make from each car, and how many cars you can make. Simple as that.

I can’t see how making 80k x 4 cars in a year can be worth 100B market cap. Another car firm making 11M cars is only worth 75B. Is a Tesla car 45 times more profitable than a VW car?

1 Like

Personal cult is the best. Better than all the rest…

It is as if you are sitting at Elon’s Desk and calculate the P/L for his company. I get what you are asking, but unfortunately I do not have any data point to provide the details.

The nearest and closest approximation can be made by analysts who has access to Bloomberg terminal. If someone has Bloomberg terminal access (this is $24000/month subscription), they will provide all such data. Usually, such access are available with institutional investors/hedge funds or big research institutes like Stanford etc.

But, analysts are not so reliable as they work for people who pays to support or oppose !

$30k solar EV ![]()

1 Like

1 Like

Tesla’s Model 3 Is Becoming One of America’s Best-Selling Sedans

They are only supplying the Model 3 to the U.S right now. International market will 2x - 3x the demand.

They are only supplying the upper end model right now. Unleashing the 35k + options version will 5x the demand (just based on price reduction / demand relationship).

I.e there will be plenty of demand.

1 Like

Can you buy a new iPhone for $200?

Volkwagens profit margins are low. Growth is low (err, shrinking?)

Meanwhile Tesla is growing 75% YoY in revenue. Valuation for growth companies are based on discounted estimates of future cash flow.

Here’s a basic estimate. Assume in 5 years Tesla is selling 2 million vehicles / year (in line with current growth rate and plan). Assume ASP of $60,000. Assume 15% gross profit margin. That’s $18 billion a year.

This is somewhat priced into current stock value. Once Tesla turns profitable (at least temporarily), and then concrete plans for China plant (starting construction soon), Model Y production, Semi production, Pickup Production, stock valuation based on these principles will go up higher than the current 50 billion value. Expect 100 billion valuation easily.

1 Like

And it’s only going to get worse for some companies.

Valuations are forward looking (that’s what makes some stocks more volatile, forward estimates are more noisy).

Say you are Mazda, you are making decent profit on decent volume, and valuation is in line with steady state or slow growth.

Suddenly the market sees that in 5 years, everyone is going to want EVs, and you have zero plans for EVs. Even though your current profits are okay, they are going to estimate that your profits in 5 years might be 0. Or negative, because you have all this capital spent in ICE which value has plummeted.

What should Mazda be valued at then? Future earnings are expected to tank, so the stock crashes (even if company is earning profit currently)!

2 Likes