“This policy, jokingly, basically works with air. Yes, out of $3,400, $2,800, yes, two thousand and eight hundred dollars go back to the owner of the insurance policy in a form of a loan month after month. The rest is to pay for cost of insurance- $600 =COI.”

This is why you’re a fraud. Read your own illustration. The planned annual income, planned annual loan, and accumulated loan are all zero until age 60. How is the person borrowing $2,800/mo if those are zero? As soon as they borrow, then they are charged interest. The returns decline and they won’t have the $400k/yr at age 60. You’re either ingnorant or purposely leaving out material information.

Notice the illustrated loan rate is 6.14%? That means if they borrow the $2,800 the cash value only earns the difference between your weighted average interest rate and the illustrated loan rate which is less than 1%. By the time they take their fees, the client would lose money each year. If the index performs less than the loan interest rate, the client loses money then too. You either know this and are purposely avoiding it, or there’s no way you know enough to be selling these products.

For the Part 1: Based on your pictures posted, I clearly understood what insurance company does. Your IRS quote “rules of the 26 U.S. Code 7702 & 7702A and so on” is legally protecting insurance company to do such business.

They get big monthly premium, grow the amount at 6.44% until 60 (sure, we need to pay 3400/month until 60) and then they provide 424k/year as loan every year until death. This is exactly like reverse mortgage with collateral of premium money. At death, they reconcile the balance and provide balance to heirs. IRS can not consider a loan as income.

As I said already, we live at the mercy of insurance company at the age of 60 until death. More than we survive, we need pray the insurance company needs to survive ! We do not legally own anything

Regarding part 2: You mis-understood the concept of 401k. Yes, you are not against 401k, but your understanding is not correct.

We own 401k and we use brokers (Vanguard or Fidelity or Schwab or any other brokers). If they maintain (it is optional) they charge you a fee. They are financial planners/analysts maintaining your wealth. If you buy mutual funds, they charge you a fee, which is common as ER (expense Ratio). But still legally you own the money. You can move from one broker to another, or withdraw (IRS penalty before 59.5 years)…etc

My company uses fidelity as broker, but I maintain myself. I do not pay any money or extra payment to them. At any time, we own the money just the savings account or checking account.

Gee! It’s what? Almost 3 AM somewhere and I have a stalker on the line?

This poor guy’s guts are burning! He can’t let it go!

After asking so many dumb questions he goes to attack and attack and attack because he can’t let go of his past stupidity asking so dumb questions. Do I care? No! He thinks that somebody here is going to buy a life insurance from me. Not anymore! I got more than one and they are happy. I do it just to make somebody madder than what he is. Guess who? My stalker!

Happy now boy? You can put as many negative topics about life insurance as you want, I will post as many about 401K and any deferred programs as I want, and I can beat you to the punch on that.

Now you can go to sleep, you were waiting and waiting for me to respond, right? Well, I knew that! Go, before you kill somebody, you are so hurt inside we need to call security in your compound, you never know a mad man going postal. You work for who you said? …

Go ahead, you have a spread shit better than something the DOI in CA and the government approves. You look childish with your "well, I brought data, graphics, why comment guys, I am the only one knowing the truth… really?

Our clients understand numbers, and they are told about all this, risks and benefits, you dummy think that I need to bring 30 pages when your stupid brain won’t understand them anyway? Why? You won’t.

Don’t you have a dodge drafting, coward kissing putin’s rear end Twhitler’s topic to defend? Oh…I forgot! You are not one of his supporter!

Прощай, товарищ товарищ

Yes, we are at the mercy of the insurance, 401K managers. But, if you know, and I know you know, you play the game, make your moves and hope for the best.

I forgot, in life insurance, as in this policy, you own the money too. You can choose the strategy every year if the IC allows you to do so. The problem is when you need to make a loan. Who is more lenient? That’s the question.

How it works: Indexed universal life insurance links the policy’s cash value component to a stock market index like the Standard & Poor’s 500. Your gains are determined by a formula, which is outlined in the policy.

•Pros: You can access cash value, which grows over time. The cash value is linked to a stock market index, so if the stock market goes up, you get some upside, too. Within limits, your payments and death benefit amount are flexible.

•Cons: Your cash value doesn’t take full advantage of stock market gains. Understand the policy’s fees and participation rates and the cap on your return before you buy.

Participation rate: The policy will dictate how much your cash value “participates” in any gains. For example, if your participation rate is 80% and the S&P 500 goes up 10%, you get an 8% return.

If the index goes down, you won’t lose cash value; you’ll just get zero rate of return. Some policies offer a small guaranteed interest rate in case the market goes down.

I have that type of policy, 4% guaranteed. But why bother with ignorant people?

Cap on gains: Your gains in cash value will also be limited by your cap, which is the maximum you’ll get no matter how high the market goes. For example, a cap might be 10%. If the index goes up 20% and your cap is 10%, you’ll get only 10%. And remember, only a portion of your payments are going into the cash value component to begin with.

Flexible premiums and death benefit: There are additional moving parts to keep track of, such as your payments and death benefit. Within limits, you can decrease your premiums or skip a payment, as long as your cash value covers the insurance costs. You need to keep track of this. If you’re skipping payments and you don’t have enough cash value to cover the costs, your policy could lapse. Some policies let you adjust your death benefit, too, as your family’s needs change.

You have no facts to counter my points on how loans work, so you resort to personal attacks. You’re either ignorant on how the loan works or purposely misrepresenting it which is fraud.

My mother is in exactly the same situation as your grandpa was. She has a seven figure investment base split between a trust and an IRA plus social security.

She is living in a decent retirement home - not assisted living…yet - and has to pay full boat because she has resources. Whereas, others are charged less on a sliding scale based on their available income.

Her monthly rent for a studio started at $5,000/mo went up to $5,500 after one year and is now slated to increase to $6,000/mo at the end of year two. This includes the room, some group facilities and programs, cleaning, food in a restaurant style dining room. But no extras like dispensing her medications, assisting with showering, etc.

My mother gets really worked up over the rent differentials based on income. She points out that she and my father scrimped, saved and invested and have to pay. While spendthrifts who didn’t bother to save and likely indulged in luxuries like European vacations and fancy cars now receive substantially discounted (subsidized) rents in a retirement home.

She’s right of course. We live in strange times where anyone is allowed to hate anyone who appears to have more wealth than they do and expect that their wealth will be drained away to subsidize those who don’t even try to save. We see such attitudes in news stories every day. It’s a sad, sad situation.

The only positive I can see from this is, investing in providers of such retirement communities might be lucrative. Considering those rents and the minimum wages they pay to the various employees, they’ve got to be making bank.

By not using imy HSA to cover medical expenses, it has grown into a substantial benefit that I can draw on to pay health insurance premiums between my retirement and Medicare eligibility.

However, there was a current cost in doing this. I had to pay some pretty steep medical expenses during the build up out of pocket due to the high deductibles, copays and coinsurance rates. I did save unreimbursed receipts planning to make massive, tax free withdrawals in the future if I needed money.

But, I’m looking at retiring in January and I’m only 60. I plan to use the HSA balance to pay my health care premiums until Medicare kicks in.

Kaiser health care for me (60) and my wife (66) are more than $2,000/month. I authorized payment yesterday. Luckily, my employer, although they should not be, is paying the entire tab. Well, it’s actually you guys because this is public employment.

When I retire, I’ll continue the coverage for me and switch my wife to a Medicare supplement and get her fully enrolled in Medicare. It still won’t be cheap due to her medical needs and the lower levels of insurance that will be provided by that coverage. The premiums are about $400/mo for her.

I’m at a strange point in life. Enough money to retire. But not enough to afford health care coverage that runs more than any mortgage payment or rent I’ve ever paid. I’ve tried to find some PT or other employment that offers health care but, I’ve learned the hard way that one will not be hired at 60 in most occupations no matter their qualifications. Let alone any PT work that offers health care benefits at group rates and is at least partially paid by the employer.

I keep threatening to stand on the corner at the shopping center with a sandwich board sign that reads “WILL WORK FOR HEALTH CARE”.

I’m not alone in this but have also come to realize that, most young people just don’t get it. They’ve got a big surprise coming.

I am not saying that it is right or wrong, but many people in your mother’s situation will “give” away their assets to a trusted relative (you) and get subsidized care also. I know from experience many people do it. Then they will basically accept her social security funds as payment.

Too many of the same thought… oversupply… my OHI got hammered because a provider of such lucrative retirement communities is behind on its rent. Can only make money when it is not obvious to many. When it is obvious, usually is time to sell.

No. You make post after post about how Trump will only benefit the rich. You act like that’s the worst thing ever. I asked you for one positive thing Obama did. The only thing you could name was the stock market which only benefits the rich. Apparently, you had no issue when a democrat only benefits the rich, but a republican benefiting the rich is the end of the world. If you really are against polices that only benefit the rich, then you should be against it no matter which party does it. The fact you think democrats benefiting the rich is good while republicans doing it is evil is very revealing.

There are many ways to avoid that end. Except people don’t believe what they are told with anticipation. They are just stuck to the idea of real estate, 401K, retirement packages, (non-existent nowadays in the private industry) and the dream that their SS benefits and whatnot aren’t going to be affected by their own income at retirement. Basically is the lack of planning.

But, this is the moment when you don’t hate that government. You need it and you embrace whatever it throws your way.

I believe, my own interpretation, that screw the 30s-40s and even 50 year olds living out of welfare or section 8. Those who worked hard deserve a peaceful and well provided retirement life. And we can start a dialogue with the corporations receiving tax cuts when they don’t need it. This old lady does.

It looks attractive in paper, esp no tax after 60, but all our money is owned by IUL company and we need live at the mercy of IUL company after 60 ! There are plenty of chances we get impacted when IUL company is not in existence or mis-managed.

It is better to pay IRS+state tax, but own something on our name at the retirement years. This is the main reason 401k survives.

Most people aren’t using 401k anyway. The average person over 50 has less than $50k in retirement accounts (401k, IRA, Roth, etc). People just don’t save for the future. Also, that analysis ignores company match which most of us can receive. Most companies match 50-100% of up to the first 4-6%. That’s a free 50-100% return on 4-6% of your annual income.

What money?

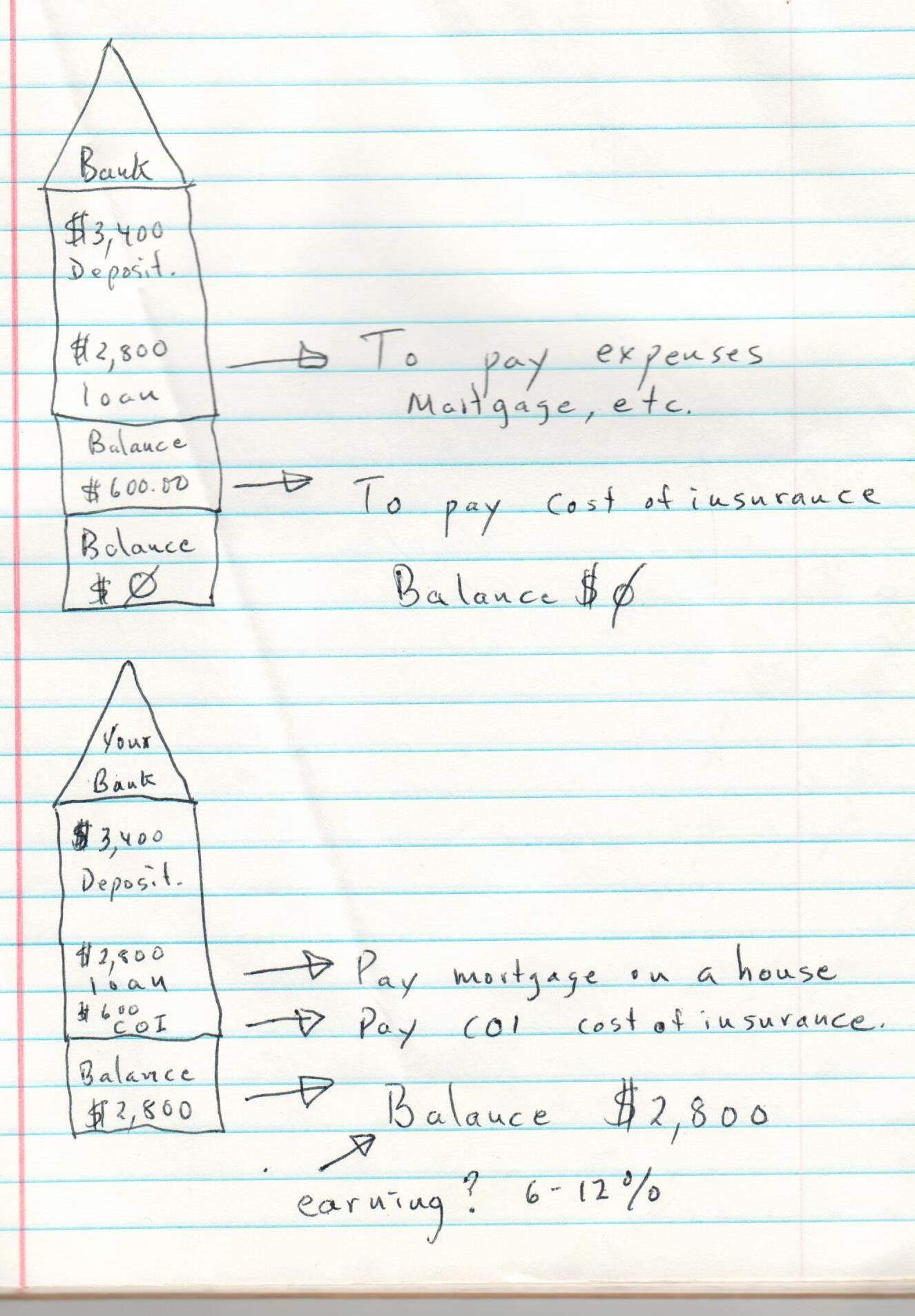

You open a premium of $3400 as in the case above.

Loan $2800 never pay it back. Are you with me?

$2,800 dollars, green bucks are still in your account. Are you with me?

Now, you have $2,800 earning up to 12% in your policy.

Then, you grab $2,800 (loan) and pay for a mortgage on a house. Understood?

Now, add the $ you get from the rental of that house. How much? Let’s say $2K a month. You have $24K from the $2,800 you loaned.

And you still have another $2,800 earning who knows, 5-6-8-12%?

I gave you an opportunity to find an insurance company going bankrupted. Did you find one?

Read the link, David explains why you won’t find one IC going BK.