Top 10 EV / NTM Revenue Multiples SaaS names

Snowflake and Cloudfare are always in the No.1 and 2 spots.

Top 10 EV / NTM Revenue Multiples SaaS names

Snowflake and Cloudfare are always in the No.1 and 2 spots.

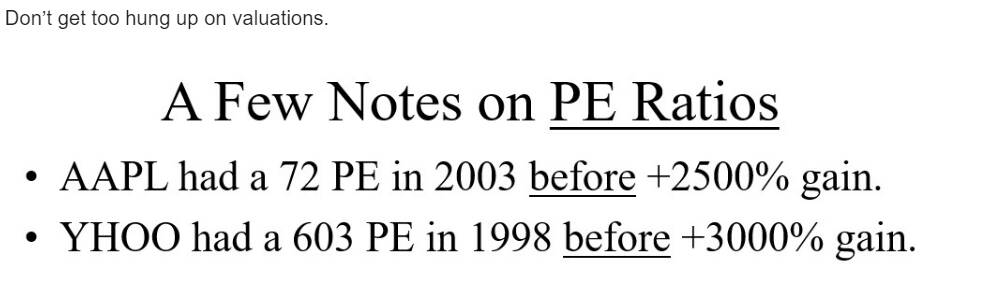

When market (vested parties esp during IPOs or Dilutions) hypes the stocks P/E shoots up like 300+.

Example: TLRY

When company growth (CAGR) increases by real revenue/income growth, market understands the real value, then P/E shoots up like 300+.

Example: TSLA.

It is up to the investor to drill down the financials (Qtrly and Annual reports, conferences) to understand the Real Value vs Hyped Values.

People also use PE as a universal term. They rarely clarify if they’re talking TTM or forecast for the next 12 months of earnings. It’s not much delta for the 5-10% earrings growth companies. It’s a huge delta for companies that are rapidly growing earnings.

Some people use PEG ratio, since you divide by the growth rate. Thats supposed to measure companies with different earnings growth rates on equal footing.

Rule of 40 has become the standard for SaaS companies. Revenue growth + non-GAAP profit margin needs to be over 40. Then people rank companies based on the score. This is why a lot of SaaS companies had to cut spending recently. Revenue growth slowed, so they had to increase profit margin to stay above 40. It wasn’t an issue with lack of profitability or risk of bankruptcy. It was pressure to hit the metric.

https://twitter.com/RealMattMoney/status/1657277819947302912

Matt comparing growth of PLTR software with AWS.

“software for the modern enterprise”

Another thought… have any of you worked in a company these days and realized how inefficient data and processes are being taken care of… these are multi-billion dollar organizations using tabular data entry like SAP and excel to run their business… Revolutionary… in 1990

It’s 2023 - the modern operating systems used to manipulate and split data using operating systems and ease of decision making overcome the Windows OS releases of 1990.

The step change in capability from Foundry OS’ to Windows is comparable to what AWS was for the internet…

What is the message?

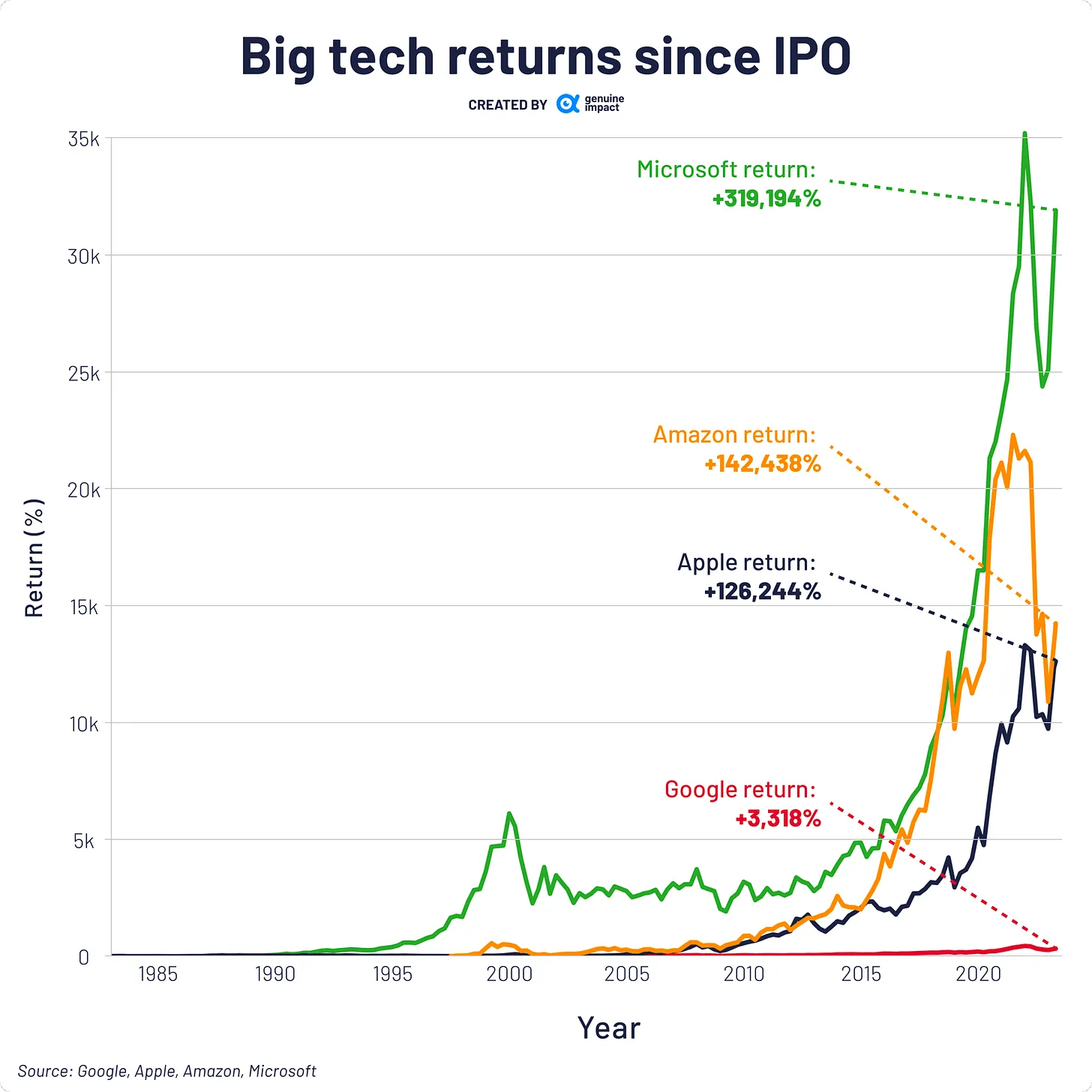

Message is shooting for 100 baggers is not realistic.

Even Google only manages 33x, assuming you held on tight since IPO. Very hard to do 100 baggers. And the pursuit of 100 baggers may hurt more than help.

Why MSFT, AMZN and AAPL make it to 100 baggers whereas GOOG couldn’t?

Btw, if you’re not going for 100 baggers, just do broad indices investing… don’t bother with individual stocks. Indices are (almost) guaranteed 100 baggers in a lifetime.

How about finding a small number of 10 baggers every decade?

.

Somehow is the same as gunning for 100 baggers. Those 10 baggers could be 100-1000 baggers.

What I mean is, if after 10 bagger, no more potential, dump; if got potential, continue to hold for another 10 bagger, total 100 bagger ![]() If still got potential, continue to hold for one more 10 bagger, total 1000 bagger

If still got potential, continue to hold for one more 10 bagger, total 1000 bagger ![]() Current examples, NVDA and TSLA.

Current examples, NVDA and TSLA.

.

Not astute enough to answer above question? ![]()

Why don’t you just enlighten us?

Don’t give up. There is one pretty obvious.

Hint: Obscurity

I thought Mongo DB does this too. I honestly didn’t get the hype around it at first. Then I saw how it can be applied to an application, and how it horizontally scales. You can throw more servers at it to scale instead of only going bigger the way SQL scales.

Snowflake is another technology that is a game changer. It seems pretty easy to automate data from all systems into Snowflake then throw Power BI or Tableau on top for dashboards and visualizations. I’m helping product manage new dashboards for our leadership team, and it’ll be Snowflake with Tableau on top.

There was a really good blog post by an Opendoor exec. It was about how most companies measure outcomes (NPS for example). They realized NPS is a lagging indicator, so they were always late reacting to changes in it. They decided to understand what inputs drive NPS and track those. That way they are focusing on actions that improve NPS. Not many companies have hit that realization yet. The entire data science space and exec understanding of it is in its infancy.

I’m slowly driving that behavior. My first step in this direction was to stop focusing on how many people are hired and start focusing on how my recruiter phone screens are happening. Those are the leading indicator of how many people will start 3 months from now. My long-term goal is to not forecast hiring and use ML to forecast it based on interview activity in Workday. It’s just lower priority compared to customer facing projects.

There’s a lot of hype around AI and automation technologies. There are a lot of other technologies that have the potential to automate work and make people far more productive. The companies figuring it out will get rich selling the solutions.

SNOW + NEEVA = Simplified version of PLTR

Many companies don’t need the sophistication of PLTR.

Analogy: Most individuals do not need a financial advisor.

Most businesses don’t need a CRM/ ERP.

Both types are needed.

Obvious corollary: Simplified ones are always easier to understand, implement and use.

Another obvious corollary: As industry matures, sophisticated ones would move down, and the simplified ones would move up. Which one is a better approach? Execution ![]()

Disclosure: I hold shares in a sophisticated one: PLTR and a simplified one: SNOW, my usual way of hedging my bet. Currently, I have slightly more $ invested in PLTR and is taking advantage of the recent swoop to add more SNOW.

Exactly. Nascent always have plenty of players. Is up to us, investors to figure out which one can make it to MSFT throne ![]()

Snowflake can get expensive easily. (Don’t disagree that it’s powerful and has very good connector ecosystem)

It’s good for smallish companies but once you have several PB and you do all your compute in it, you are locked into big costs. This lock-in has worked in Snowflake’s favor all these years.

It doesn’t help that they don’t offer transparency into tuning levers to own your costs. Negotiating with them to reduce annual contract was a huge pain for us.

I am moving more workloads at my employer to Databricks where we can manage costs better and actually know what is happening.

Is Databricks harder to use? I am guessing because of its open source roots. OS tends to be cheaper but needs more sophisticated tech staff to make it work.

Have you leveraged a Snowflake solutions architect? We had good success this that and were able to lower spend.

Snowflake did offer consulting services to save money but the economics of it made little sense. (Spend 100k save 120k).

At this point snowflake is being managed by a different team at my employer and theyve resorted to bringing in a cheaper 3rd party to analyze and optimize workloads.