Great article and I think( you may or maynot) ARM is the way to go in near future. I have really come to appreciate his blog and the indepth insights he provides. If you haven’t been to this blog, check this out, run by local BA guy who owns quite a few properties himself.

The next time someone is hawking you a 30-year fixed ask them: 1) What their major was in college or grad school, 2) How many times have they refinanced before, 3) Quiz them on what the current 10-year treasury yield is, 4) Where was the 10-year treasury yield 10, 20, and 30 years ago, 5) If they are a homeowner, 6) How much more are they going to make off you. Finally, refinancing now to a 30-year fixed from an existing 30-year fixed is a good option. Refinancing to a 30-year fixed is just a sub-optimal good option vs. borrowing on the shorter part of the yield curve. Both are good options vs. not refinancing. - See more at: http://www.financialsamurai.com/30-year-fixed-mortgage-loan-vs-adjustable-rate-mortgage-arm-the-choice-is-obvious/#sthash.QDTW7iB3.dpuf

I am mainly an observer in this forum and financial samurai blog is my other source of knowledge. Yet to buy my first home.

"Match fixed rate with length of stay. If you plan to live in your house for 10 years, take out a 10 year fixed rate (amortizing over 30 years) as the most conservative loan duration. A 10 year fixed rate is cheaper than a 20 year or 30 year fixed rate. It is only logical that you match your mortgage fixed rate with your expected duration of stay. Sure, you might stay longer, but you might also stay shorter as well. If you know you plan to stay in your house forever, it’s more justifiable to take out a 30-year fixed "

If you know how many years you will stay, then you can choose right option. Otherwise, you are making loss either way. Risk is yours…

I got a fixed 2.5% rate (granted 15 years) at no cost. It is a great rate that allows me to sleep pretty darn well at night. That is all I need to know.

I have personally seen my colleagues move,upgrade, downgrade houses roughly 7 years in the bay area. So it really does depend, but if MBS is tracking with the 10 year treasury yield, its not going back to 6,7% or double digits any time sooner.

Again, it depends on what your risk profile is and like you said if that is the home you are going to retire in as well.

Agree. I bet low rates is the new normal. People keep saying rates can’t be this low for this long, and yet rates keep getting lower for longer.

The equity build up is much faster with a lower rate ARM product. Many people just look at the headline rates. But look at the payment table sometime. Compare the effect different rates have on your equity build up. Massive difference.

I ran a amortization calculator on 10 year ARM vs 30 year fixed on a 900K house. Difference in interest rates 1%.

At the end of 10 years the Principal remaining to be paid off between 10 year vs 30 year is $20K, i.e extra equity is $20K. Assuming a 2% annual growth rate(@inflation) in the initial price of a house, $20K was 1.8% of the forecasted price of the house at the end of 10 years.

If I have 20+ years remaining to retire, I would probably not put all my money in my house.

My plan is to start paying off more towards principal when Standard Deduction becomes higher than (mortgage interest+property tax) deduction.

Thats correct. If you compare equity with 5 or 7 year ARM vs 30 Yr fixed, it is significant, which should cover some of the risk incase the interest rates increase dramatically, again my bet is it wont anytime soon.

In my situation I will definitely need a bigger home in next 5 or 7 years anyway.

Is there some kind of thumb-rule when it’s best to refinance? E.g. is it when (Market rate-Current rate paid)>0.5%. I ask because, there are closing costs to refinancing.

How best to find low cost/no cost closing cost refinancing? Would love to hear from the real estate gurus here.

You can do it for no cost. I used cash call. I’d never use them for a purchase, but they had the best rate on refinancing. Everything was online. I was actually surprised at how good their technology platform was. It was far better than Quicken Loans who I used for purchase. They brag about their technology platform, but it wasn’t impressive.

Roy321, I have learnt that refinance cost is not we are shopping for, aim for the best rate possible. make the banks fight each other to get your business. send emails with rate confirmations from one bank to other.

Cost of refinance has a break even period, typically 1 year or 2 years with the savings in the interest it brings. So be prepared to pay for the cost of the refi.

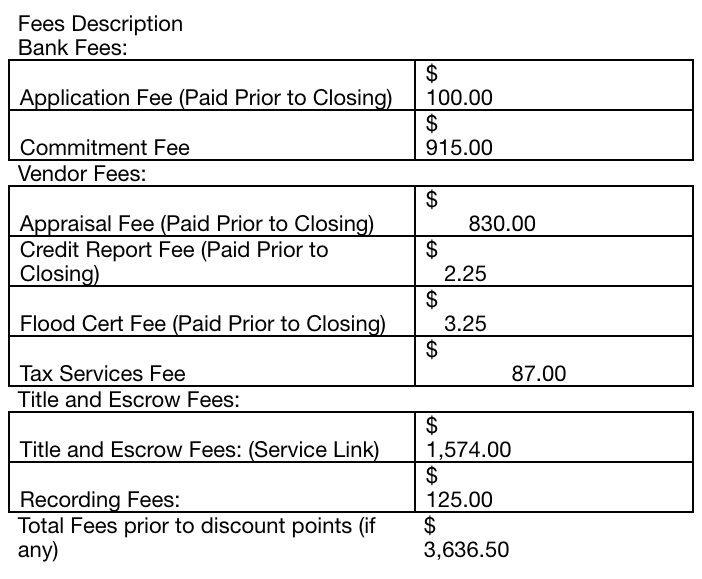

Having said that, understand each line from the refi cost breakdown and ask the bank on what is negotiable. Here is a sample breakdown of the refi cost.

My rule of thumb for refinancing was breaking even within two years.

I’m the odd duck and loved the I/O ARMs because we paid as if it was a 15 or 20 year loan. It offered flexibility when tires and brakes were needed at the same time on multiple cars. It’s that spending problem I have.

I always do no-point no-fee refis. The only cost from the refi is the interest for one day when you carry both loans at the same time (there is a one-day delay from new loan funding to paying off old loan). Technically if you think rates are at their lowest point one ought to buy points and pay closing costs to get the lowest possible rate (takes 1-2 years to breakeven), but so far I have never been able to convince myself that’s the right strategy.

I recently did a 2.4% 5-year ARM refi. When I put the numbers into my spreadsheet, I was shocked to see that the portions for interest and principle in my monthly payment are almost 50-50.

I agree with your approach. I once paid closing costs with a CU couple of years ago and then ended up with another refi a year later because rates went down further. So in this rate environment, it’s better to go no-cost no-fee refi.

Btw,2.4% APR on 5/1 ARM is a great rate. How long ago was that? Care to share the ref of the broker who got you that rate?

I did refi about 3 months ago and I think the rate today should be similar if not better. It was with HSBC. To get the best rate you need to maintain a relationship with them which means you need to keep $100k worth of assets in an account with them. When I did the refi the best rate I could get was 2.625% (5-yr ARM) with ~$1k closing costs with other lenders. My loan is jumbo.

I think $100k pre-tax funds with HSBC is not bad, but putting up $100k cash investment for a 0.225% rate reduction may not be worth it unless you have specific reasons.

If you do end up going with them you can PM me so we can both make some money.