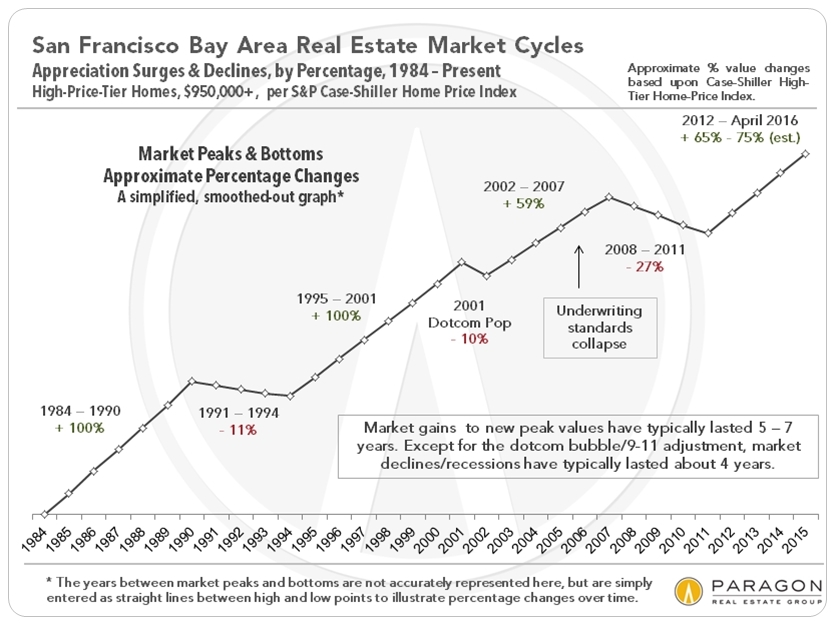

“Over the past 30+ years, the period between a recovery beginning and a bubble popping has run 5 to 7 years. We are currently about 4.5 years into the current recovery, which started in early 2012. Periods of market recession/doldrums following the popping of a bubble have typically lasted about 4 years. Generally speaking, within about 2 years of a new recovery commencing, previous peak values (i.e. those at the height of the previous bubble) are re-attained – among other reasons, there is the recapture of inflation during the doldrums years.”

From the above chart, my WAG is prices in fortress would decline by 5-10%, just outside 15-20%. Just dreaming on a public forum . And if it takes only 2 years to recapture previous high, what is the point of timing?

Besides, if time is rough and sellers are desperate, you can take advantage. No sane seller will do seller financing in this market. But what if times are rough? Sellers may be more open. Also near the top lending tends to be lax. I still wish I had the foresight to get a few million dollars’ worth of NINJA loans back in the days.

In short, there is no bad time to buy. And it’s not my agent license speaking.

If this chart has been published earlier, I would just buy one SFH in SV in 2014 instead of three SFHs in Austin suburbs. The correction is just too small, can get those prices from probate sale or old folks retiring elsewhere.

Also, when prices drop most people are too scared to buy. They wait thinking it’ll drop more, or they are worried about their job security. Prices decline when there are recessions, and there are far more layoffs in recessions.

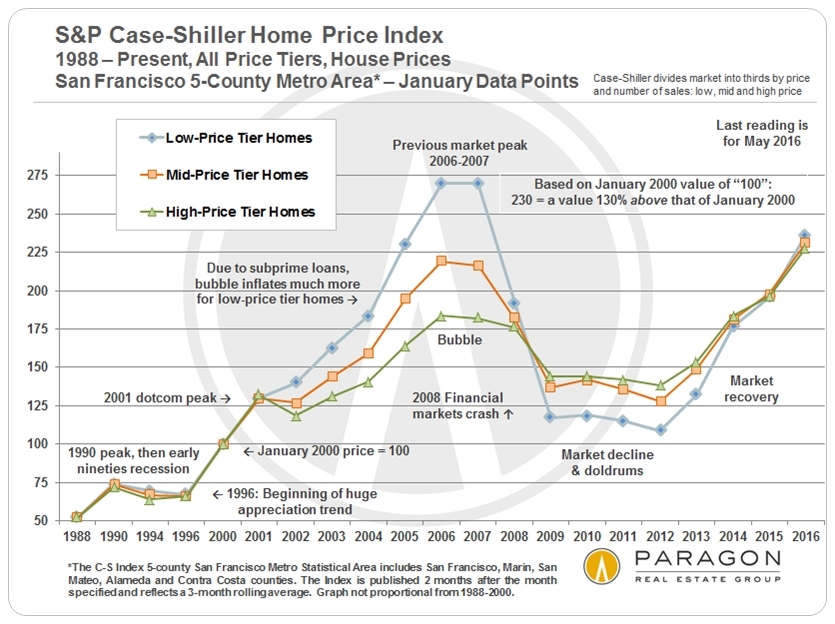

A lot of great charts. I am amazed by this data. In 2000 all three tiers started the same and went through different highs and lows, but now they are at similar appreciation %.

Also note that low end didn’t see any dip in the dot-com crash. It just kept on chugging along… kind of gelling with my suspicion that the low to mid tier will keep on going now, while the high end is correcting.

At national level, RE appreciates at inflation rate. RE in SFBA have always appreciated faster than inflation. The bounce from 2009 is a few folds faster than inflation.

Low end is still appreciating…still affordable…Plus it is where boomers put there money after exiting from the BA…To Sac suburbs, Tahoe, Palm Springs, and surrounding states…Oregon and Arizona in particular

The intent is to buy one more SFH in SV, not to diversify first. Now, I have to sell the Austin houses to buy the SV house, or hopefully the 2017 correction is deep enough so I don’t have to sell Austin houses.

Why do you need to sell the Austin house esp when you get a good yield 8%? Also what is the cap rate for this home? 8% yield is almost like SP500 growth.

With such cash flow, can not you get another mortgage with 25% down payment?