Nvda broke 50-day. That’s not good in the shorter term. There will probably be a better entry in the future. I still have my June 90/140 call spread. It’s about break even right now.

UBNT, I have my eye on it. Waiting for it to form a longer bottom. Founder owns 70%, so I don’t think it’ll go down much more.

I hate TSLA. Model 3 production by September? Now it includes solar city which is losing money. They are lowering solar city sales to slow down cash burn. I don’t see a path to profitability for solar city.

Bolt so far dispatched 1167 cars as of Jan 2016. TSLA has the pressure to release now. TSLA can not add price to his 35k model. If they do, people will go to bolt easily.

Tesla will raise another $2-2.5B. When they announced model 3, I estimated they’d need to raise $4-5B total to get it into production. I was using BMW’s South Carolina plant to estimate. They’re going to land a little above the bottom of my range. If they want to make 1M cars a year, they’ll need a second factory. No way they’ll get another at the same fire sale price. It wouldn’t surprise me if it cost them $7-8B to buy a plant and tool it up, so they can make 1M cars a year.

How much is a Bolt? If enough people cancel their order for Model 3 and get their deposits back, TSLA may implode. TSLA needs every penny it can get to feed that money furnace.

An electric car is pretty useless in cold climates, restricts range up to 50%…Probably will never buy one in Tahoe…Plus the have to have low ground clearance to be aerodynamically efficient. …But I have seen a few Teslas…probably BA tourists…A Leafs range can drop to below 40 miles in subzero weather…Of course gas mileage drops a lot in Tahoe too…Cold, 4wd and slow going due to bad conditions drop mpg a lot…

*2017 BOLT EV LEASE SPECIAL

LEASE FOR $259 per month for 36 months

$3995 due at signing

$37495 MSRP

Tax, title, lic. fees extra

10,000 miles per year

25 cents per mile extra

5 at this lease

Lease terms end or change at 30000 miles

NVDA to 200-day SMA?

UBNT broke 200-day SMA? Back to $25-$30?

TSLA, 50-day SMA at $240 and 200-day at $220. Guess wait for it at 200-day just like NVDA.

TSLA may reach around $200, but not NVDA and UBNT.

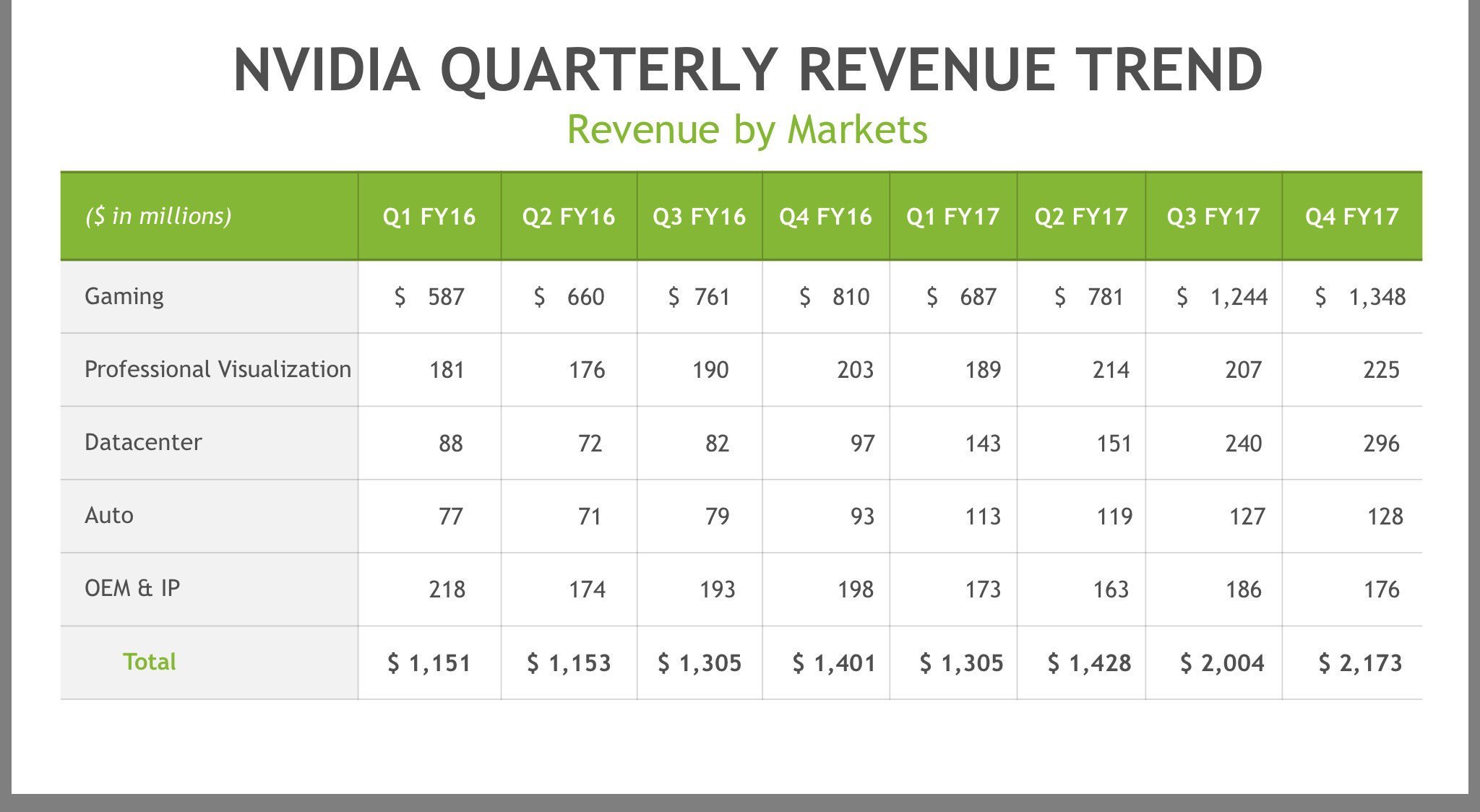

IMO, Another 35% down for NVDA & UBNT is unlikely unless a major crash happens. If you see the quarterly report, both companies are doing great, in all margins. When economy is good, they are bound to go up.

The fall is mainly by two downgrades, but not by their fundamentals and the same analysts downgraded QCOM, which is almost 8% up since the bottom.

Sold NVDA call spread. Lost $3.94/share where if I had kept common stock it would have been $14/share. I bought the spread with profits from the stock, so NVDA was still profitable overall.

I have not idea. The initial run is always based on increasing good fundamentals. However, invariably the run becomes over-expectations… we need a good way e.g. FCF analysis, to assess whether it is still supported by fundamentals or over-expectations. What did FCF analysis say? Or what is your valuation model say? Or you’re basing on TA only?

For example, according Professor Damodaran, intrinsic value of TSLA is $152, AAPL is $130.