For borrowers, the calculation is clear: If an asset appreciates faster than the interest rate on the loan, they come out ahead. And under current law, investors and their heirs don’t pay income taxes unless their shares are sold. The assets may be subject to estate taxes, but heirs pay capital-gains taxes only when they sell and only on gains since the prior owner’s death. The more they can borrow, the longer they can hold appreciating assets. And the longer they hold, the bigger the tax savings.

“Ordinary people don’t think about debt the way billionaires think about debt,” said Edward McCaffery, a University of Southern California law professor who says he coined the buy-borrow-die phrase. “Once you’re already rich, it’s simple, it’s easy. It’s just buy, borrow, die. These are planks of the law that have been in place for 100 years.”

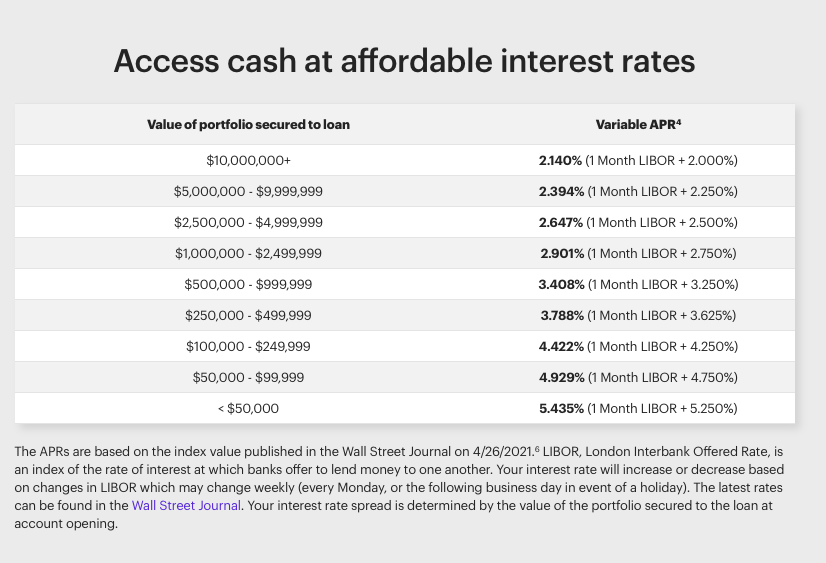

In addition to the bespoke loans Goldman Sachs Group Inc. GS -0.42% offers clients of its exclusive private bank, the Wall Street firm advertises securities-based loans of $75,000 to $25 million to clients of outside financial advisers with “no personal financial statements, tax returns, or paper applications.” Merrill Lynch recently quoted an interest rate of 3.2% to clients with at least $1 million in assets. Those with $100 million or more can get a rate as low as 0.87%.

I was reading that the other day. Most of the things are we talked about on this forum, but nice to see some recap, and worth the read. Rich get richer scheme!

These kind of loans are by no means just for the super rich only. On IB I can take cash out as a margin loan and spend on whatever, no question asked. They can even give you a debit card if you ask. Interests rate is much better than the 3.2% Merrill Lynch is giving.

Yah i forget if it was called an equity loan program or pledged asset program. it’s one of those 2. My wife got it. but as @Zeapelido said just be careful. You don’t want to borrow too much against a volatile portfolio.

Thank you this is great. I’m definitely going to apply for this line.

I had single minded focus on Real Estate for too long and thus I’m totally un-educated when it comes to maintaining my Schwab portfolio and utilizing it to the max . I’m going to discuss with my FA of any downsides to it but I don’t see any big risks.

you guys are all great friends , we should all have a real get together sometime.

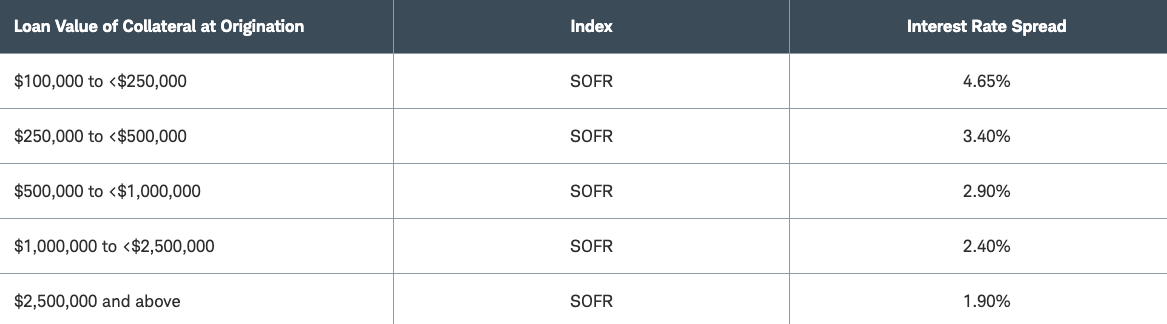

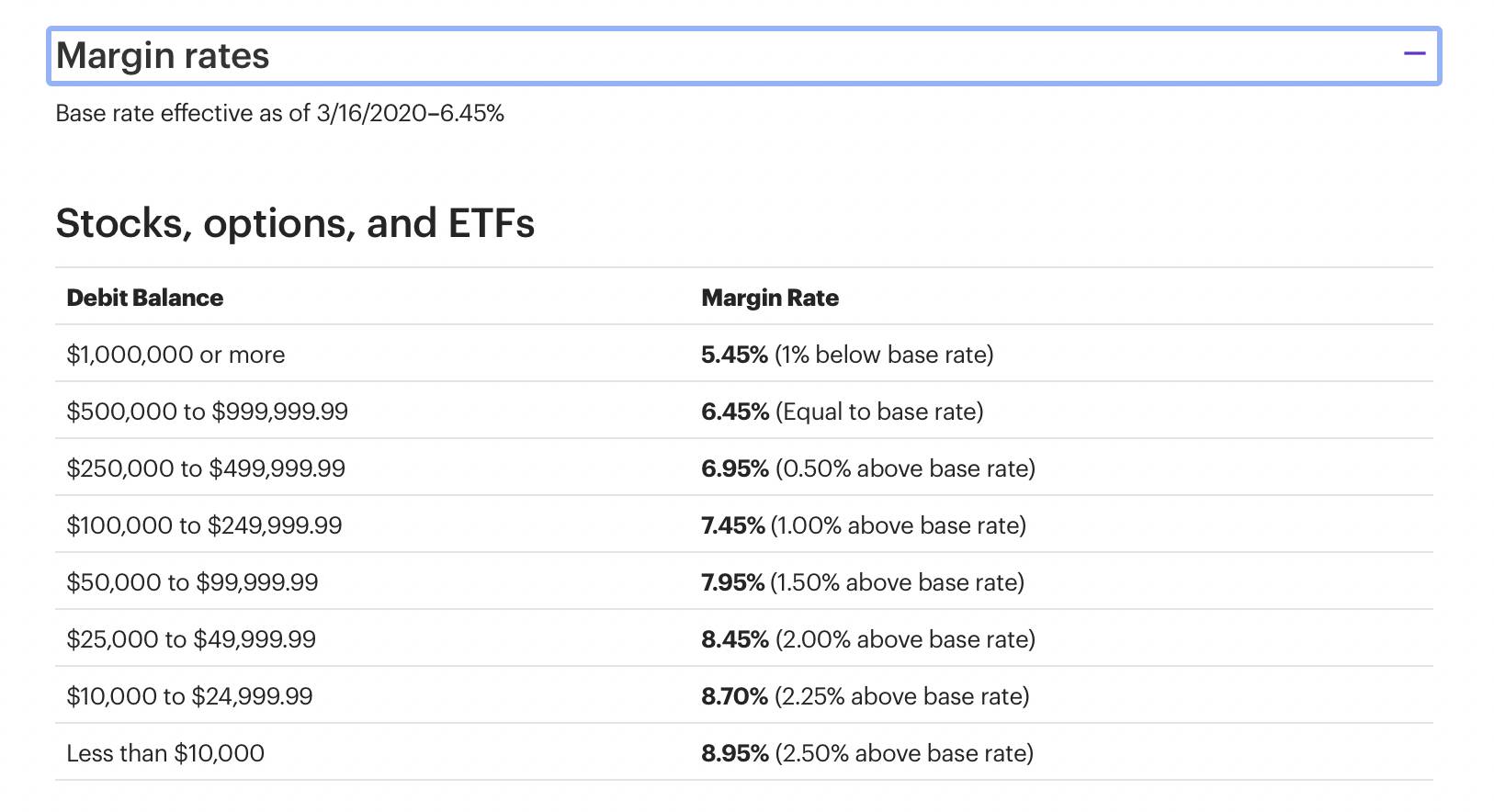

In case there is a misunderstanding, margin loans are different from collateral loans…

. Collateral loans are secured vs stocks and can be used for anything, you are charged interest on 100% of the loan (not reducing balance) all the time.

. Margin rates for trading can only be used for trading and are on whatever balance.

I didn’t borrow any collateral loans. Did go on margin sometimes, during the recovery from Mar 2020. Currently, not on margin.