Realestatebull asking RE questions instead of providing answers?

1 Like

You now know that I’m not worth 30M

2 Likes

Bummer I was going to ask for a donation

2 Likes

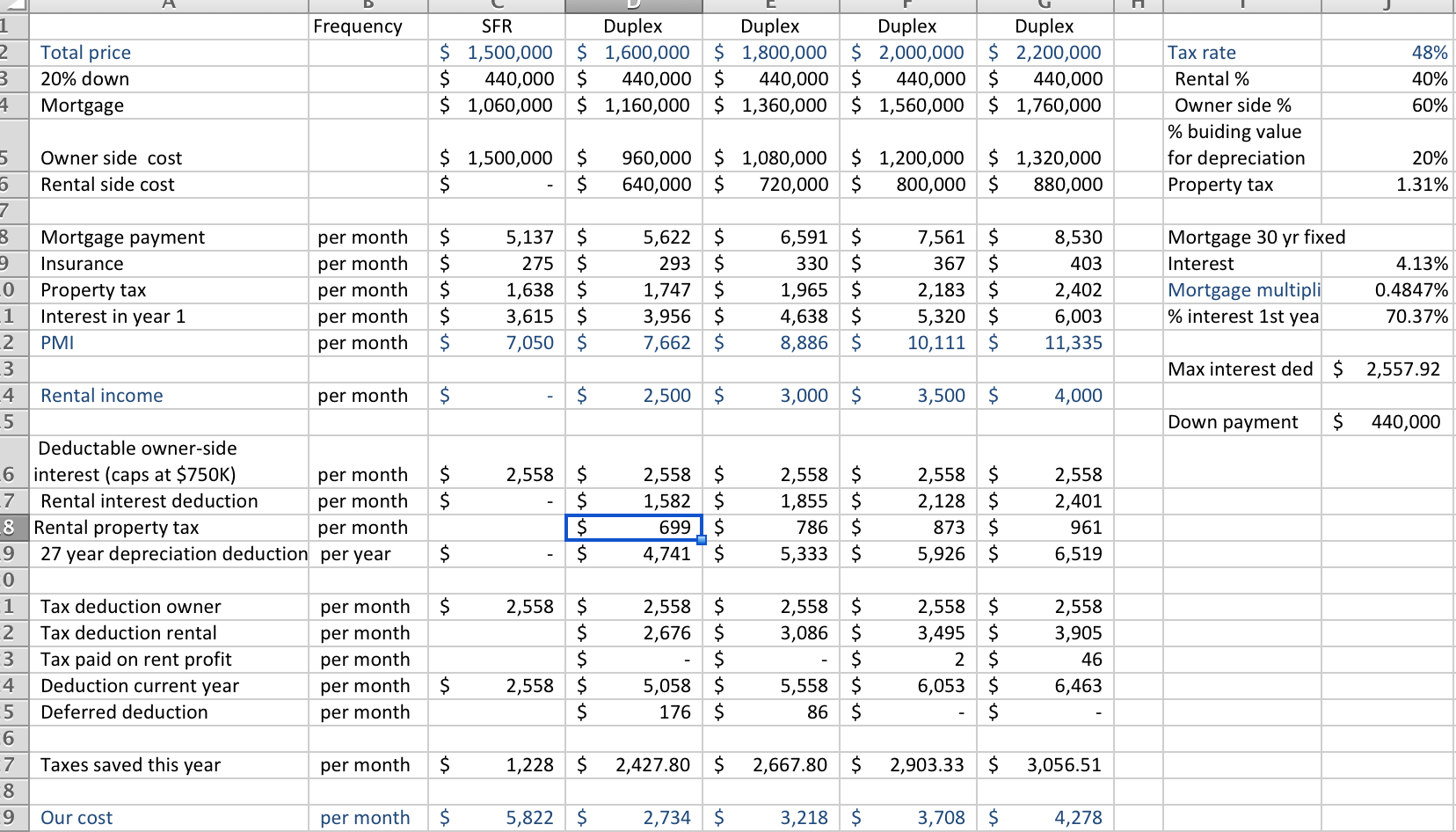

Ok. Can you guys critique again? I added the rental property tax, and I’m assuming the owner side is included in the standard tax deduction for married filing jointly. (I also made the down payment the same for all options rather than 20% down.)

In your deductible owner side for the Duplex scenario, it shouldn’t be the same. Assuming it’s an even split duplex, you can only deduct 50% of the interest, so your numbers for the duplex should go up a little.

edit: oh I see, you are assigning higher value for the owner side. Just saw those rows.

2 Likes

Can it be proportional to the sqft of each house?

Yea I think that’s what she’s doing since it shows the owner portion significantly more. So I’m imagine like a 3/2 on one side and like a 2/1 or something I guess?

2 Likes

I thought that people generally did it by square footage. I thought I’d asked here, but definitely that’s what two of my friends have done.

I was assuming 3/2 1800 sq ft (owner side) and a 2/1 1200 sq ft (renter side). Garages not counting.

A couple of things to add to the comments that others have noted -

a) I would do as you imagine - split the depreciation as a proportional %-age of each unit against the total square footage of the duplex. I have a condo building where I bought both units in the building as one transaction (as opposed to two separate transactions) and I split the depreciation as a proportional %-age of each unit against the total square footage.

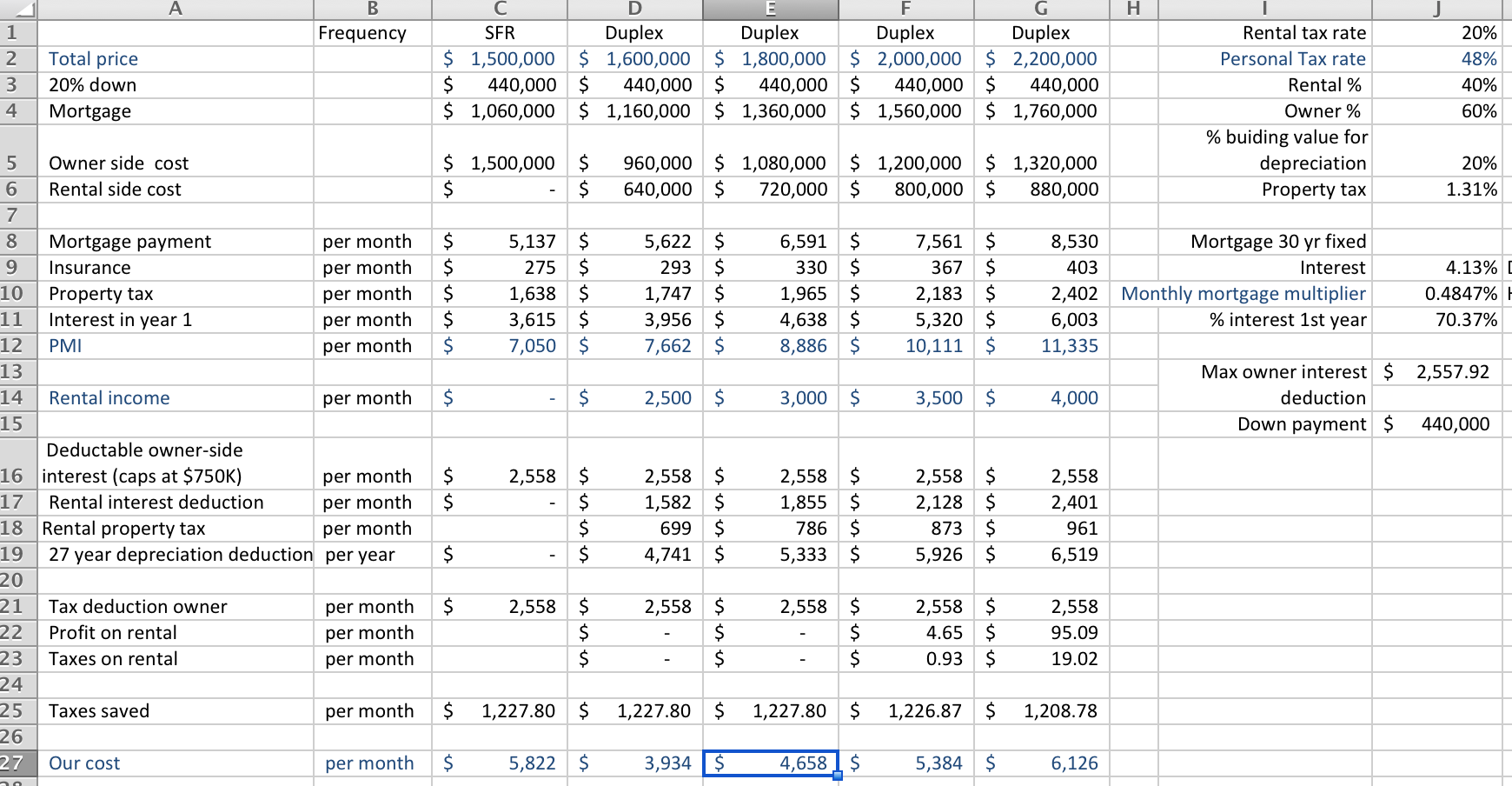

b) I see your tax rate of 48% but please note that the tax rate that your “owner side” interest deducts against is different than the tax rate that your “rental side” interest deducts against. This is because the rental side is passthrough income and therefore qualifies for, among other things, the 20% passthrough deduction for 2018.

c) In SF right now building value is typically 30% as noted by the assessor’s office. However it is possible to argue higher - does the building have, perhaps, lots of unpermitted work that the city does not know about but would add value to the building?

Oh no! I thought these deductions were coming off our regular income.

Although, now I’m realizing I did something wrong as I didn’t subtract off the rent either… So if the rent is $4K/month and the costs are $4K/month, it just cancels doesn’t it? So you’re not actually getting any deduction at all, you’re just not paying income tax on the rent. Is that correct?

Correct. In that case Schedule E would not add anything to line 37, AGI.

Crap. That wrecks that plan.

So… what’s the point of getting a (owner-occupied) duplex then?

Rent out both sides. Cap rate is usually better than SFH. The conventional wisdom is appreciation is lower, but I’ve seen data that says it isn’t. I think @manch was the one thst posted it.

I guess the other way to look at it is that you’re getting a rental for “free”.

Because if you are patient, you will be able to enjoy some good income. The goal is to make it so that rental income = actual costs + depreciation. Since depreciation is a “paper loss”, that depreciation actually represents a cashflow you can take home today.

Eventually when you sell the property, you will have to pay tax on all those years that depreciation shielded the income stream from tax (depreciation recapture) — unless you don’t sell (or 1031 exchange or pass away)

Also remember, over time, your loan costs are fixed. Your property tax will go up but at a rate capped at 2% courtesy proposition 13. And, rent will track (or perhaps outpace) inflation. As well, after at least a decade of record-low inflation, we are headed into an inflationary environment again - rising deficits, tariffs on imported goods, and a demographic shift that increases demand (lots of millennials) will all contribute to inflation.

Hmm. So it’s not the initial payments I should be calculating, but the later ones…

Well, the good news is that at least I have the numbers straight. That would’ve been a heart attack in the making.