Heya. Can you guys save me some time and headache and tell me what the best 529 plan is for college savings that I want to manage myself (I want to be able to buy/sell stock/index funds like I would for any other stock account).

And while we’re at it, can anyone tell me what the advantage is of a Coverdell ESA? You can only put in $2K/yr. Hardly going to make a dent in college costs.

Greenblatt, Joel You Can Be a Stock Market Genius: Uncover the Secret Hiding Places…

Lynch, Peter One Up On Wall Street

Graham, Benjamin The Intelligent Investor: The Definitive Book of Value Investing

Hagstrom, Robert The Warren Buffett Way

Klarman, Seth Margin of Safety: Risk-Averse Investing Strategies for the Thoughtful Investor (read this last ! this is avl internet as pdf)

I have these physical books and scan them daily some pages.

The main difference between Coverdell ESA and the 529 plan is that Coverdell allows the use of tax free dollars towards K-12 expenses, whereas 529 is strictly for college expenses.

If you knew how to play it, 529 is good, but I’ve heard it has many complications, kids may not make it into a college, parents will go instead of them, can do this, can’t do that. That money also can be lost in a crash, I may be wrong, not my field, we never suggest that product.

Best you can do, open an IUL ($1 million dollar baby) and hand them the policy at college age, you can loan $20K+ here and there at that age. Time is the essence, it should have been open long time ago.

Look at the benefit of life insurance, not the “I die my beneficiaries get $” but the ones that also allows you to pay a premium and on top you can put an extra amount of $, which can be loaned within 10 days, never to be paid (deducted from death benefit at the end) and that amount is still earning returns, about 8% in the last 20 years and you never lose that principal.

This is a conservative approach, not your addicted to stock market games personality wearing Gucci one night, asking for $ for a cup of coffee the next day at your favorite corner.

Really? So if I started investing in a Coverdell for my 7yo now, I could use it towards private high school later? That’s good… except for the income limitatations.

Whatever I have given is appx (almost minimum), the actual amount may increase.

I paid UC 45k/year for four years. When my son completed college, I told him the amount as almost one house down payment amount, he did not believe that. Then, I asked him to go through the details, step by step, finally he agreed and said “It is too expensive !”.

After few years, inflation will catch up and colleges/universities always hike the fees.

One big mistake: I should have bought a condo for him to stay (remember it was 2011), now I can easily make it work as nice rental.

DEFINITELY. College town rentals are a sure thing for the next 20 years. And after that inflation will make it still a sure thing. (Another reason I want a duplex here–if any of my kids go to Stanford, I want them getting an apartment-mate and covering MY costs, rather than me forking over $$ to you guys to house my kid.)

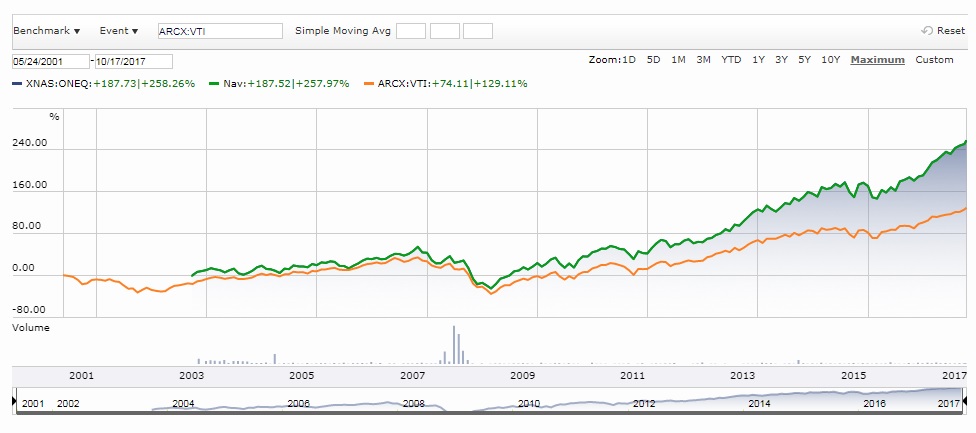

For someone based in California/Nevada, one of the best plans is to use Vanguard 529 plan. It gives you access to all low cost ETFs from Vanguard. I put a fixed sum every month in that plan and dollar cost average VTI.