he Federal Reserve raised interest rates for the third time in six months on Wednesday, showing it believes the U.S. economy is growing, albeit slowly.

Economists expected the hike, which brought the target range of the federal funds rate up a quarter percentage point to between 1 percent and 1.25 percent.

The central bank said it still expects to increase rates one more time this year, despite weak inflation and weaker-than-expected U.S. retail sales.

In addition to rate hike, they wind up QE money too.

The Fed said the moves would begin later this year “once normalization of the level of the federal-funds rate is well under way,” but did not specify a date.

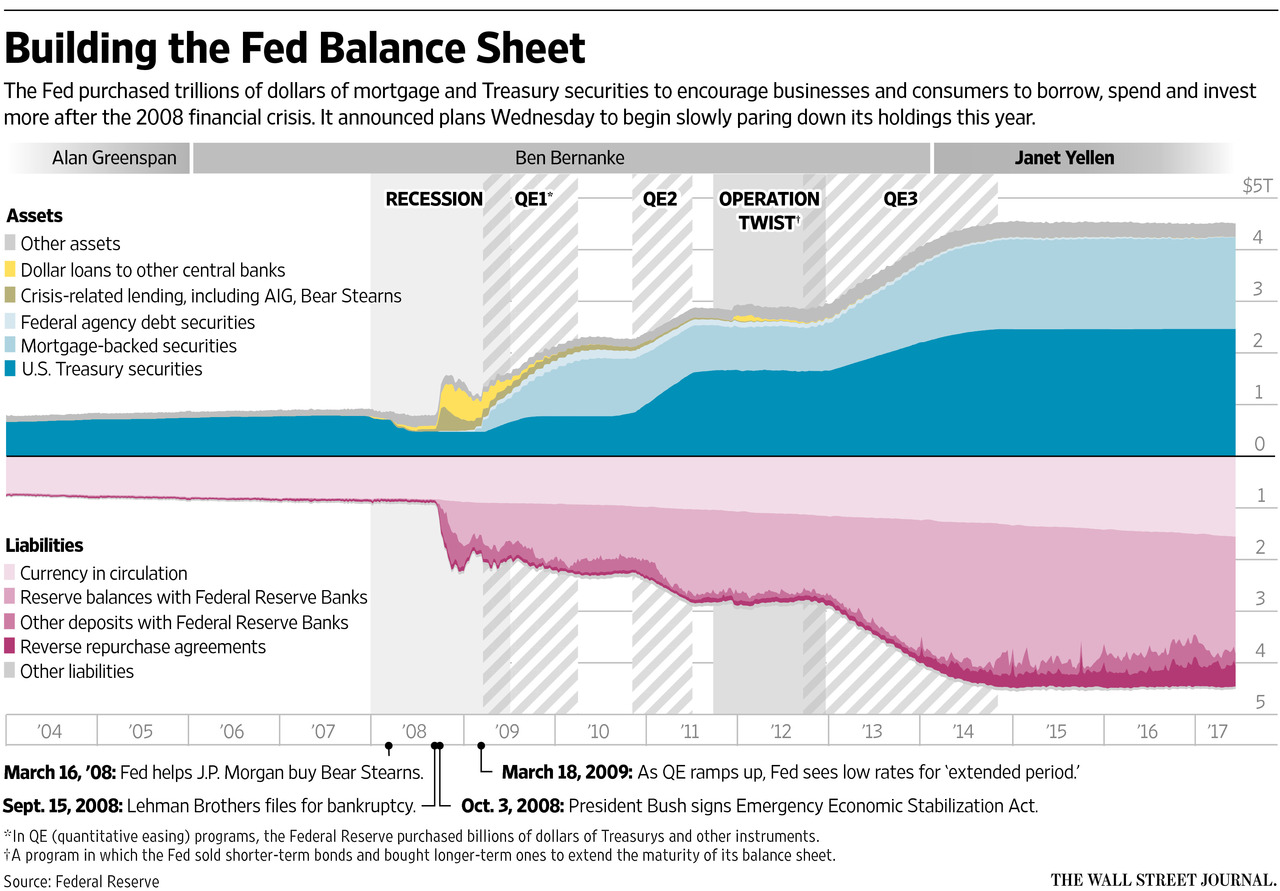

The Federal Reserve said Wednesday (06/14/2017) it plans to slowly shrink the pile of Treasury and mortgage-backed securities it accumulated during three rounds of asset purchases, marking an end to a key strategy it took in response to the financial crisis.

In a document unveiled alongside its post-meeting statement Wednesday, Fed officials outlined separate paths for shrinking Treasury and mortgage-backed assets in its portfolio. Initially, the Fed would allow $6 billion of Treasury securities to roll off its balance sheet monthly once they mature. That amount would rise by $6 billion every three months over the course of year, at which point the central bank will be rolling off $30 billion in Treasurys a month.

The Fed said it would roll off its mortgage-backed assets more slowly, at a rate of $4 billion a month, with the caps rising by $4 billion every three months until reaching $20 billion a month.

(Three rounds of asset purchases, known as quantitative easing, swelled the Fed’s portfolio to $4.5 trillion in the years following the financial crisis. Since then, officials have been reinvesting securities as they matured in order to keep the balance sheet level.)

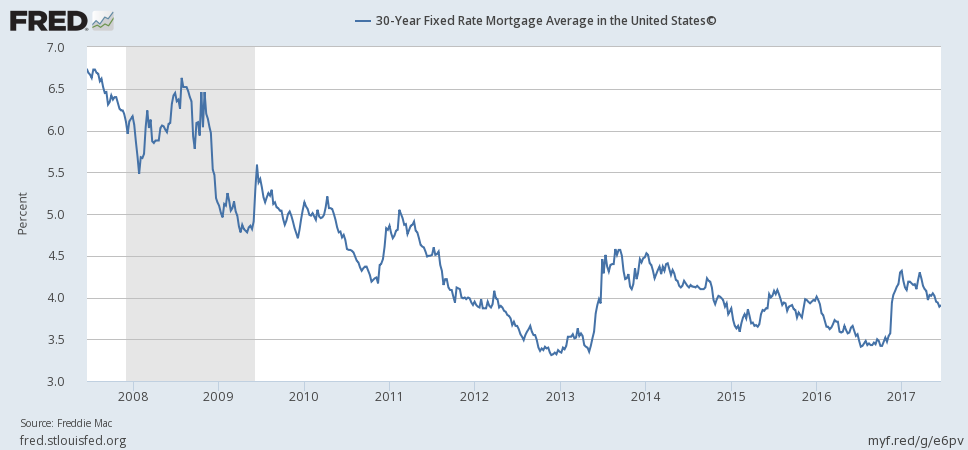

It’s the second increase this year (third overall) yet mortgage rates are lower than they were in January, 2013. Mortgage rates are lower than they were in January, 2017. In 2013, rates went up 1.1% in less than 2 months without the fed changing interest rates. Then they steadily decreased for years without a fed rate change. At this point, interest rates move independent of fed rate moves. It’s a non-event. I’d post a graph, but I don’t want to offend anyone that can’t read graphs.

The rest is just mumbling speculation about things that might or might not happen months from now. No one even knows what it would look like or mean. That won’t stop some people from worrying themselves into the grave over it.

This is something really, really “graphic” worth commenting. $260 a month in savings is kind of an entire month going out to a not so decent dinner over the weekend. Or the payment of PG&E.

Were people ready for this or it really didn’t have any coverage?

Definitely this assumption is wrong. Interest rate affects economy, but not particularly real estate. In real estate, lender’s spread reduces and that affects the service providers bottomline.

Graph reading or inference may not be proper, just the future will tell the story.

We’ve been over this. Fed rate has little influence. At this point, banks are nothing more than paper pushers. They get paid a fee to sell the mortgage, and they get paid a fee to service it. The profit on a mortgage is the spread between mortgage rate and MBS bond rates. It’s not the spread between mortgage rate and fed rate. Fannie/Freddie make that profit since they buy over 90% of mortgages. Banks aren’t holding the mortgage, and they aren’t the ones created and selling the MBS.

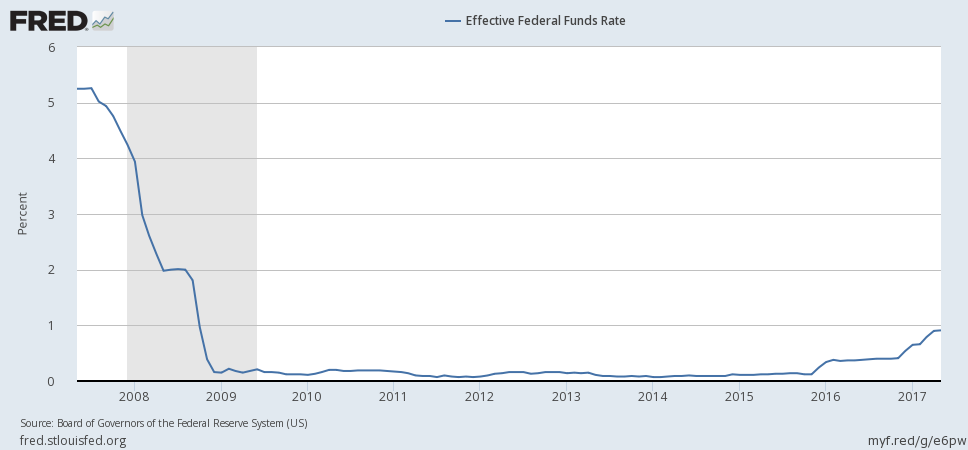

The fed sets the over night lending rate. That’s about as short-term as it gets. Mortgages are much longer term, so the yield curve is far more important to mortgage rates. The yield curve is a measure of how much higher interest rate investors demand based on longer duration. The yield curve moves up/down based on multiple factors. A major factor is inflation expectations. Inflation has been slowing this year which is why mortgage rates are down from January despite 2 interest rate increases on the over night rate. The yield curve has flattened. If inflation expectations increase, then the yield curve would steepen and long-term rates would increase without a change in the over night rate. The yield curve is why mortgage rates could move up and down a full percent without the fed changing the over night rate.

This is what bond gurus like Bill Gross do all day. They look for spots where the yield curve deviates from what they expect and trade it. Us normal people look at it and see mortgage rates go up/down. He’s looking at 1-yr, 3yr, 5-yr, 10-yr, etc bonds and looking at the relationship between yield and predicting how it’ll move. For big picture economics people, it’s where they are most effective investing. It’s also the deep end of the pool in terms of analysis required. It’s one of the areas that’d interest me for a PhD when I “retire” from tech. I think the potential intersection between this and machine learning could be really cool.

Rate increases have an impact on buying a home. Allow me to explain a case from a friend of mine:

He was in escrow for about a month and half he told me. By then, a rate increase was pushed by the feds. When they ran his credit score and whatnot prior to closing the deal, he was short about $100 from the income they filed last year. They had to go to see their tax guy and he found a discrepancy (blink, blink) and they redid the tax returns. They are homeowners now.

Now I got what you think. You are co-relating mortgage rates (mainly primary or investors like us) with FED rate, that is fine as we were used to 5% or 6% level back in 2003-2007.

Interest rate impact to entire economy you need to account. Retail industry, REITs (short term loans) and many other startups and corporation run using term loans…everyone gets impacted. This affects entire economy even though rate hike is good for country.

This will definitely affect stock market and entire economy. If stocks are affected, then real estate will get affected later, as companies close or foreclose or lay offs like the one happened to Nike today (1400 lay off- very minor).

FED is making a deliberate pause, from now to Dec 2017, to see whether so far 1% rate hike (four 0.25% so far) is affecting the country or not. Once they are confident 1% did not affect economy, they may start hiking next year.

Yes, it impacts the whole economy. The last 3 times we’ve done rate increase cycles it was 2.75-3.25% increase when we hit the next recession. If that’s true, we have a long way to go if they keep doing 0.25% increases.

I’ve actually been thinking if there would be a relationship between household debt, interest rate, and median income. Logic would say when the debt * interest rate gets to be too large of a percent of median income then the economy hits a recession. People have to spend less, since debt takes up too large a percent of their budget. This goes to one of my points that the economy doesn’t grow without debt expansion. That’s not real or sustainable. That’s only a trend since the 1950’s. We used to be able to grow the economy without growing debt. At some point we default on debt to reset, or we have a very long period of stagnation to pay down debt.

I think we are 15-20 years from it. Each recession we cut rates to a new low. We never raise them back to prior levels. The chart is a typical lower highs and lower lows. We hit rock bottom rates the last recession, so what can they do next time? They’ll hit rock bottom rates even faster next time then what’s their move? QE didn’t do anything to stimulate the economy. We did trillions of it and still can’t get inflation or growth. I think we’ll pull off something to get the economy crawling again, and the recession after that will be the brutal one. 15-20 years is when the big 3 entitlement programs take up every dollar of tax revenue. A recession with no room to cut interest rates and a government budget crisis. Combine that with state and city pension issues, and it’ll be the perfect storm.

High interest rates are alway detrimental to investing. It just makes borrowing money that much harder. If the FED kept raising rates I might have to start de-leveraging some of my debts…

Those are from the federal reserve of St. Louis website. They have tons of data sets, and let you customize the graphs by desire date range. The federal reserve publishes a TON of data so does the BLS.