Here FS tells you why buying a 4.5M house is nuts.

Here’s a good way to look at your down payment:

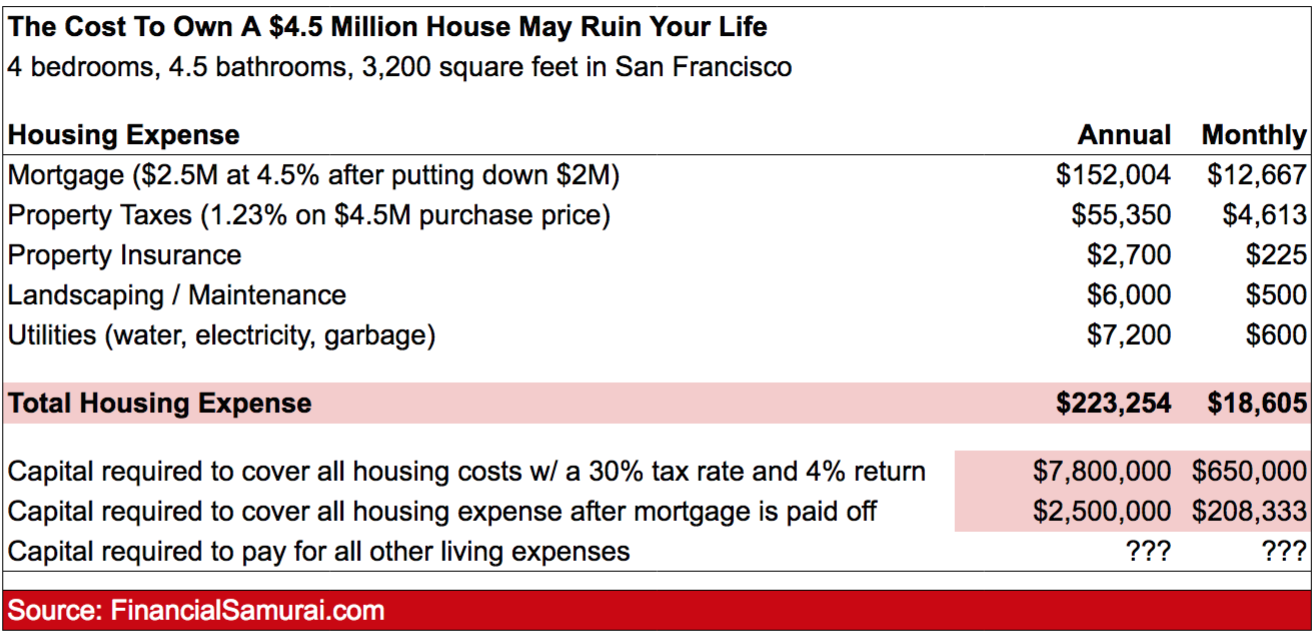

The $2 million downpayment is guaranteed to earn $62,000 a year in state tax-free income if it was invested entirely in a 10-year government bond. Hence, one could easily argue that the total annual cost of owning this house a year is not $223,254, but actually $223,254 + $62,000 = $285,254.

My bar is lower than FS’. For me anything over 2M is no-no.

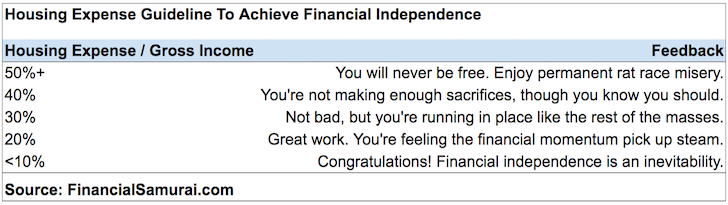

This table is more useful than the absolute price of the house. Some people can buy a $4.5M house, and it’s low percent of gross income. Personally, I think it makes some sense to stay in the under $1.2-1.4M range where homes are the most liquid. Granted, I think that range keeps moving up, but you can usually see based on DOM where the price is that homes start to sell slower.