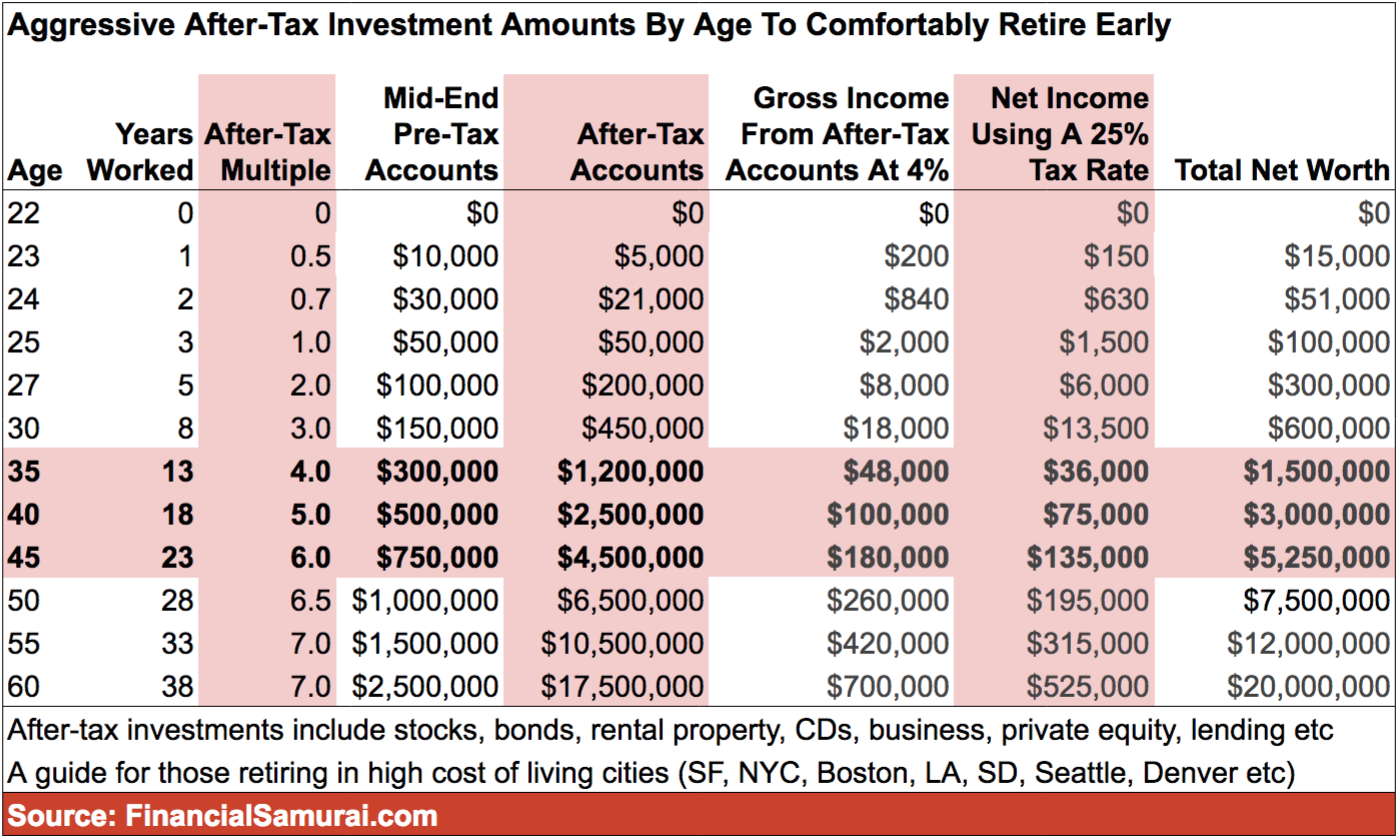

If you retire at 40 with $2,500,000 in after-tax investments, you’ll only be able to generate $100,000 a year in gross income or $75,000 in after-tax income based on a 4% rate of return. Is this enough? Not according to the Department of Housing and Urban Development, which considers $100,000 a year “low income” for a family of three living in San Francisco, for example.

Buy $2.5M of AAPL.

Yield 1.31%.

Sell some AAPLs when 1.31% dividends is used up.

Don’t worry about capital reduction since AAPL appreciates at annualized rate of 22%.

He’s assuming 4% return on the $5M. You can get that with tax free muni bonds which then eliminate the income tax. He’s also assuming zero principal reduction.

This shows that income gap and wealth gap is actually much smaller now than centuries ago. The so called “rich” people are not that rich at all. The key reason is that labor cost is becoming expensive. The difference between a “rich” person and an “average” person is very small, or much much more smaller than 100 years ago.

Take last 5 years of credit card statement to find out how much year over year we spent. Calculate average expenses (all expenses) using the five years.

Say 100k/year, then this is your expense.

Multiple Teslas and multiple Euro trip is your own desire to enjoy, there is no limit.

Unless 5M or 10M is from lottery win, most people will continue to invest after retirement at 40 or 50 and even 60. It’s a good habit it’s hard to stop completely.

If you are worried, just use your 5M to buy 10 apartment buildings in SLC or Phoenix with 50% leverage, or 5 buildings with no leverage. Hire a PM to manage for you. It’s still a good retirement with a small amount of work to manage the PM and think about your strategy.

Many 75 year olds are still working on high stress jobs. I think it is nice to retire at 40-60.

It’s hard to imagine a retirement where you do nothing but eat, sleep, exercise and travel. You may like 1 day of taking care of your investment or finances per week.