Paywall, use reader view

That means reduced demand  from this source but since prices are still going up, aggregate demand is still higher than aggregate supply (btw, we don’t know the exact demand). What are the sources of demand for Bay Area property?

from this source but since prices are still going up, aggregate demand is still higher than aggregate supply (btw, we don’t know the exact demand). What are the sources of demand for Bay Area property?

a. Formation of new families

b. Local investors

c. Non-residential overseas investors

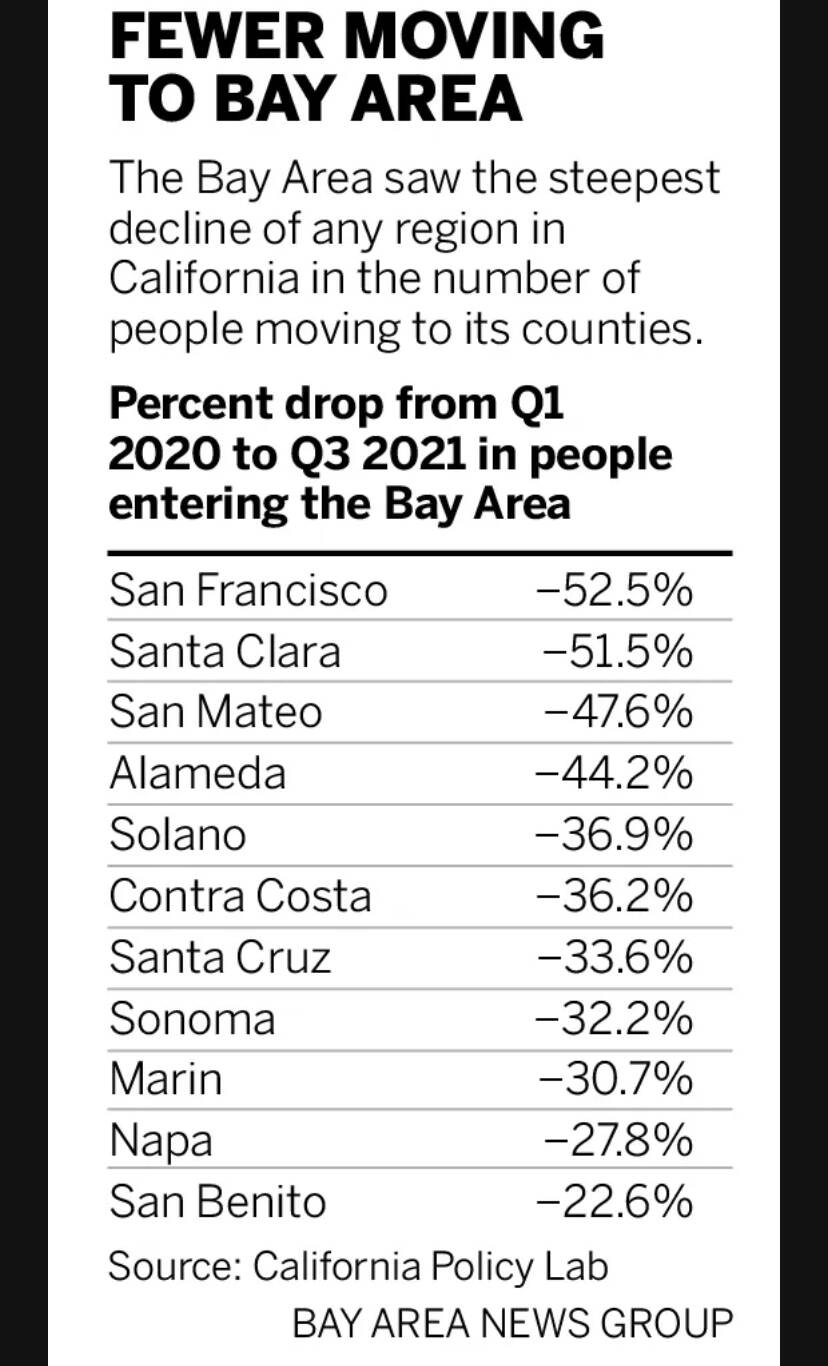

d. Migration (reduced)

Anymore?

The Alphabet unit purchased the building at 1665 Charleston Road in Mountain View, documents filed on Dec. 15 with the Santa Clara County Recorder’s Office show. Google paid $73.5 million for the two-story building with 60,000 square feet that sits on 4.3 acres.

Sold for almost $1M above list price

$1M above list seems to be the new wow factor seller’s agents are pushing for

Just Monopoly money!

Maybe it’s monopoly money, but when I see these houses selling for 20x typical annual salaries of average engineers, I wonder just who are these people that can afford to bid $1M over an already astronomical list price

That is a good question. Who is buying? Buying for investment does not make sense. I assume someone is buying to live in.

.

Depends on your outlook. Some think prices would rise 15% p.a over the next few years, so is ok to buy.

What is basis of that thinking? Prices of homes rising much faster than GDP/Rents/demand/money printing etc.

Later: added money printing as a possible driver of price rise.

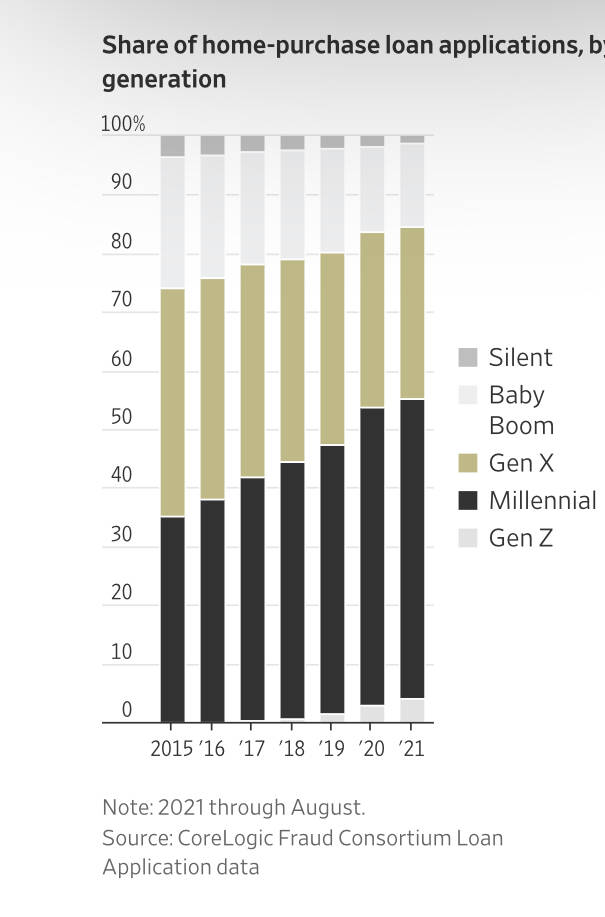

Millennials are buying in increasingly large number, some1 posted an article that claimed 50% of mortgage applications are by millennials and millennials are having two jobs to pay for houses.

Investors got the memo and are buying.

Is total number of mortgage application also rising or just bouncing around the baseline?

- What does few mean?

- Who are some?

This is what I could find. Btw, the following only talks about 2022, so few is defined as 1 year.

- Goldman Sachs is forecasting U.S. home prices will soar another 16%.

- CoreLogic, a real estate data firm, is forecasting just a 2.2% uptick in U.S. home prices during the same period.

- Meanwhile, for the 2022 calendar year, John Burns Real Estate Consulting and Freddie Mac are forecasting home price growth of 4% and 5.3%, respectively.

- There is one notable exception: Zillow. The online real estate marketplace is forecasting a huge 13.6% appreciation in U.S. home values over the coming 12 months.

Is it a different way of saying that inflation next year will be around 16% assuming most of the time REAL ESTATE just catches up with ( inflation + cost of money) ?

Both @erth and @hanera make good points.

Investors may be buying all over US because they see huge demand from millennials in the coming years, as @hanera says.

But in RBA, where SFH prices in family-friendly neighborhoods are almost $3M, I agree with @erth that buying for investment makes little sense (you can only get $5k monthly rent). So, people must be buying to live in - but these people are not from the typical local workforce. Is it all Directors snd VPs buying SFHs these days?

For oldies here, they know that investing in SFBA is for appreciation, rental yield doesn’t matter much.

In 2011, I bot a SFH in CU for ~$1.2M, rent for $3200/month. GRY = 3.2%, mortgage rate = 4.25%

In 2021, value about $3.2M, rent for $5.4k/month. GRY = 2.0%, re-fi mortgage rate = 2.625%

That is, GRY is lower than cost of financing. Including property tax and other running costs, cash flow is very negative. It doesn’t matter since appreciation is far more than these costs.

If rental yield is less than cost of financing over the long term and cash flow is very negative, then you have to put in lot of money on a monthly basis just to HODL your RBA investment property. Then, if and when you decide to sell, you are subject to large cap gains tax (no 500k exemption to cushion the blow). Is such an investment worth it compared to the alternative of just DCA buying a simple index fund like SPY or QQQ?

I still think RBA SFH is better bought to live in, and investment properties are better to buy in places like Austin where the rental yield covers holding costs PITI, and you get positive or at least break even cash flow. I just don’t see the merit in HODLing a deeply negative cash flow property. Especially, when you have to lock up $500k-$1M in down payment up-front just to buy the darned shack…