This is the impact of lender of last resort

Someone posted in reddit like this: (I do not understand whole topic).

-

A better way of saying it: A number of financial institutions overextended themselves, and so the Fed exerts its role as “lender of last resort” and bails them out.

-

In a more cutthroat version of capitalism, interest rates would rise to attract more private capital, and along the way, a number of bankruptcies of weak or poorly run institutions would likely occur.

The whole day, I read so many pages of documents why NY FED pumped-in 200 Billions cash, why yield curve inverts (where the demand is) and why J.Powell reduced Fed rate.

In short, the demand is coming from overseas, Japan…Euro banks are buying US Treasuries as US has higher yield than their currencies/countries… That results yield curve inversion…

As long as US keeps higher rate, foreign banks tries to get the rate spread holding US Treasuries. By reducing rates, FED expects the inversion comes down…etc.

It is a big subject and my understanding is half baked.

I bet the fed reducing the balance sheet has more impact than actual rate. Other buyers will demand a higher return on the MBS.

New market expectations of Fed rates

Sep 0.75%

Oct 0.5%

Dec 0.25%

Jan 0.25%

Feb 0.25%

4.25-4.5%

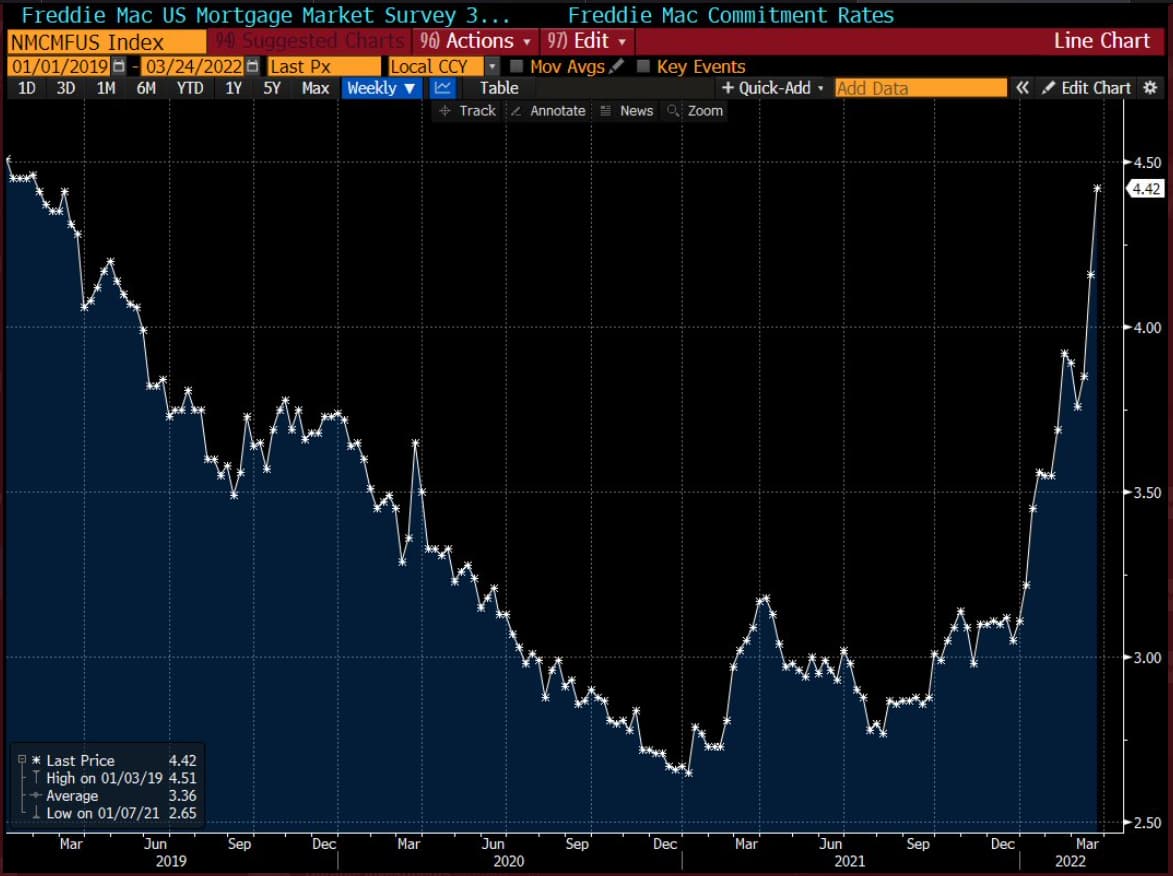

So mortgage rate > 7%

Housing recession + another stock market crash

This is not housing issue, the impact will be like year 2000.

But stock side, we can expect 30%-40% drop from here ( guess work no back up data).

Fed rate and mortgage rates are closely related, with changes in the Fed rate often affecting mortgage rates. When the Fed raises the Fed rate, mortgage rates tend to rise, and when the Fed lowers the Fed rate, mortgage rates tend to fall. This is because changes in the Fed rate can influence the overall interest rate environment in the economy, which can impact the rates that banks charge each other for loans and the rates they offer to consumers for various loans, including mortgages. However, mortgage rates can also be influenced by other factors beyond the Fed rate, including inflation, economic growth, and housing market trends. If you are considering purchasing a home or refinancing your existing mortgage, it is important to monitor mortgage rates and work with a trusted lender to understand how different factors may impact your mortgage rate.

Ok, some good news finally!!!

It’s interesting. They say they want to return to target 2% inflation over time. They never define a time period though. Inflation is clearly decreasing. Whether or not we need more increases depends on the target time period. They also mention they need to take into account cumulative effects and lag though. Then they seem to completely ignore all of that and if we aren’t at 2%, then they want to increase.

Understanding the impact of Fed rates on mortgage rates is crucial for managing your borrowing costs. When the Federal Reserve adjusts its rates, it often affects mortgage rates indirectly. If the Fed raises rates, it can lead to higher mortgage rates as lenders pass on the increased cost of funds. Conversely, if the Fed lowers rates, mortgage rates might decrease, potentially making loans more affordable.