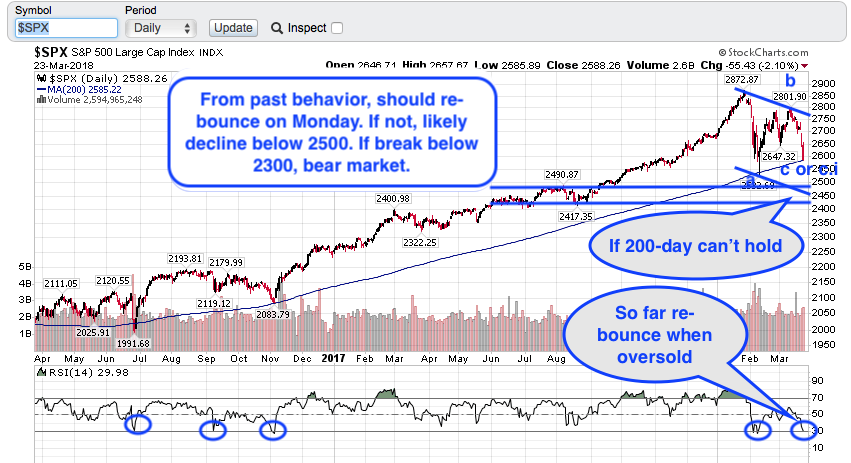

"The Dow may be at the mercy of politicians until earnings season"

If it declines, I will buy more whatever I hold.

Presently, I am trying to get some more money into my account…

Those calls man. Those calls.

If the 200-day holds, then we get aggresivley long. If it doesn’t, then we get aggressively short?

It’s hard to imagine that 200 day breaks now. Could be a great time to buy

@hanera congrats on being spot on in your prediction. You officially are the crystal ball bearer now!

Turns out to be another kind of black - the one after thanksgiving.

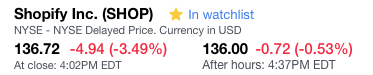

Mad money portfolio went down! SHOP is crushed by Citron. Perils of small cap is they are easily manipulated.

In short, Citron questions how much SHOP pays as commission, to third parties, to get an account/firms. SHOP pays undisclosed amount as commission, which Citron says very high and not worth or unsustainable, which is the core issue.

The issue what Citron says looks reasonable, but the stock is pulled by Bull Market always.

A huge day at Wall Street. Who’s still recoding?

I believe many ads earning companies started this way too or revenue sharing. Haven’t read the Citron article yet.

Are you suggesting it is wise to sell SHOP for now & get back in at $100 or forget about it since its model is not sustainable?

I meant your other portfolio…

4.75%?

Only interested in the amount, not percentage.

So is a trick question.

Sharing is caring.

I am not suggesting that, telling you why SHOP is vulnerable for such Attack.

In many cases, whatever Citron suggested, we are able to know it is was not right. SHOP case, they are not showing clear evidence to public that Citron is wrong. SHOP has been adding accounts, but they have huge expenses too (details are unknown).

When SHOP is touching 130, it is attractive for me to pick up. But the market volatility is high and I am also confused what to do now.

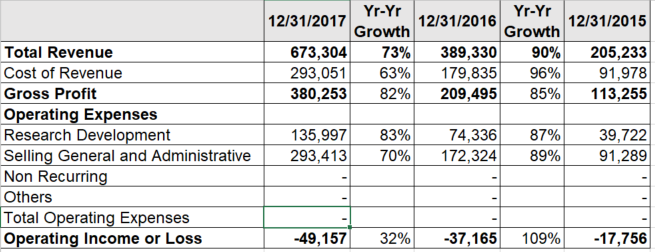

SG&A has been growing proportional to revenue for the last 3 years. If Citron was right, it’d be growing faster than revenue which would make it unsustainable. R&D is growing a little bit faster than revenue. Cost of revenue is growing slowing than revenue, so gross margin is expanding.

Buying calls would be expensive. Long underlying seems to be better. But is it low enough to buy shares? DCA purchase? May is usually soft. Apr is varied. So to buy or not to buy? In any case, I have reduced to only 1 call, so I would wait and see.