Wellsfargo and Bank of America are the toughest companies even though they account RSUs. The way they calculate DTI is entirely (very conservative) different and multiple approvals. It took me 85 days to get cashout refi which I am closing next week. This is for my CDTI=19.81% and Primary DTI=15% with Primary LTV=75%.

According to http://www.usnews.com/education/best-high-schools/california, the ranking is:

Monta Vista #11

Lynbrook #17

Cupertino #63

Homestead #113

Fremont #304

This is SF’s rankings:

Lowell #3

Ruth Asawa #49

Lincoln #87

Washington #97

Galileo #99

Balboa #147

Wallenberg #169

Plus 11 more that totally suck with no ranking. So I guess SF is not that bad, huh?

The catch with Lowell and Ruth Asawa is that you need to take exams to get in.

I am seeing strong duplex pricing in Redwood City still, but more rentals on the market as I drive around. Perhaps there’s a lag, but seems like the two should not go together.

Met with a mortgage broker and the realtors I’ve talked to recently have said things are slowing down. I think that’s probably true, but it’s not lowering the prices in RWC from what I see. Surrounding areas, yes. PA and MP have gone down a bit on median price. Atherton is low right now, but those stats are always fuzzy anyways in an area where a handful of houses sell for $3M to $20M.

Why are Gunn and Saratoga high unranked in this list?

By looking at top 20 list, most of them are really Charter schools.

FUHSD listed 3 schools.

Although I am not completely happy with current FUHSD leadership, it is quite amazing result given that those are all neighborhood schools of which admission is purely based on school boundary.

1 Like

It’s not amazing to me. Houses in that neighborhood are selling at 2M a pop… It’s not testing kids for admissions. It’s testing the parents’ pockets.

2 Likes

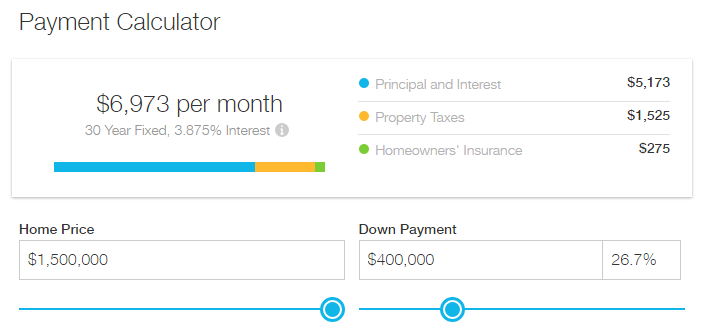

what is the safe mortage loan [ live comfortably ] that we can take , if total income is 300k per year and 400k downpayment for the house.

28% of 300K = 7K a month

That’s around the PITI payment of a 1.1M loan amount. Add the 400K DP = 1.5M house price. Maybe a bit conservative and buy one around 1.4M.

2 Likes

Already Manch has given 28%.

Any range between 25% and 35% is fine, but it depends on your age. At young age,less than 30, you can confidently take 35% as your earning likely increase over decades. As you grow older, reduce the DTI so that you will be mortgage free when you retire or when you reach your 60s.

I hate that kind of generic advice. How many kids? Do you plan on paying for their college? Are you going to send them to public or private K-12? Those 3 questions alone can vary your spending plan by hundreds of thousands of dollars.

Do you have a pension or is it 401k?

Personally, my target is to max 401k (especially living in CA), save 10%, then have housing be 50% of remaining net income.

1 Like

The ratio depends on whether you are single or have a big family…A single person can always get a roomate and can easily afford a 50% loan/income…When I was single I bought houses with no reportable income at all…Once I had three roomates pay the mortgage and lived on employment. .The government wants to put everyone in a box and drive us all into poverty…There is no room for entrepreneurs in real estate. .too highly regulated. .Just think how fucked up tech would be with a straight jacket of regulations. …All government knows is taxes and regulations. …can’t produce wealth…

2 Likes

Thank you everyone for your advice.

One Kid now in 1st grade and planning to have another kid. Will send the kids to public schools. Have more than 200k in 401k , 500k in vested/unvested stocks [ not going to use it for home buying ]

Where do you want to buy?

300k might be only wages. If you have RSUs, you can get a bigger mortgage and use stocks as savings.

Or take 28% of wage+stock as the monthly PITI. It’s better buy a primary home at the lower end of your affordability and purchase a rental home as investment.

Also consider the job stability. For doctors, nurses and other really stable jobs, take a bigger loan. For tech employees, be a little more conservative since employment is a little less stable.

I think you can go towards the higher end of affordability then.

This is a big part of personal financial plan. Regarding home buying limiting less than 30% with 5% up or down DTI is healthy.

It depends on the company (like google, Apple and Facebook) and its growth. Stocks are liquid while real estate is not liquid. Have you faced 2000 downturn? If not, read the dot.com bubble period, scary ride for tech companies. At some point of time, you may need to sell those and pay off mortgage, but it is left to you.

Do not pledge or make RSU as collateral as this is risky (dot.com failure). Limit the DTI with Pay+bonus.

First time buyer has to buy max lot and max size possible. Otherwise, they may regret later as they will be forced to stay in small home or forced to go bigger home.

Suburbs are cooling. know few folks who bought in 2014 and decided to refinance due to expected rate increase, and their houses have been valued less then what they were valued when the first took the loans…

This is Dublin and SR…

Zillow and Redfin estimates are higher then the selling price now for properties… not enough new data to correct perhaps…

That’s surprising I’m in the suburbs and see modest appreciation from 2014 based on recent sales. If no appreciation in two years that’s rough. Many homes still selling near the 2005/2006 prices (i.e. No or little appreciation in 10 years!)

My evidence is not very scientific. anecdotal and with limited samples, and only for one region in east bay. Please feel free to disregard.

You are looking at selling price and I am looking at appraisal price. the appraisal prices were higher then list price in 2014. They are still higher but not at the same level. So the folks who decided to refinance were surprised to see the appraisal value coming below the 2014 appraisal value.

A lot of price corrections too in SR. Again, not very scientific but I am seeing the amount of reduction increasing gradually…

I see, but I would think appraisal value is based on recent sales, no? Perhaps they tend to be more conservative during refinance and liberal during purchase