4 Likes

Yeah! Our IULs are predicting at least 8% returns this year.

The way indexing works, no way you can miss the train.

January you get 8%

Feb 8%

March 8%

April 8%

May 8%

June 8%

July 12%

Now, the market can go to hell for the rest of the year. You made 5%, and your principal is safe. 0% returns until the market goes through another recovery and bust.

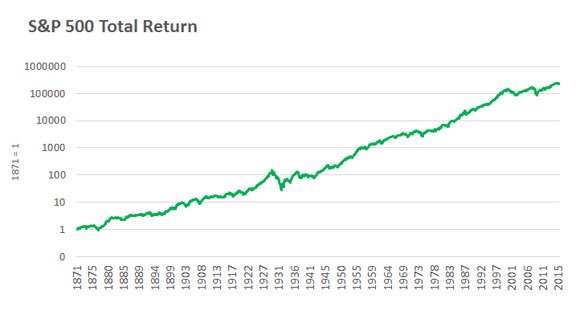

What is the 2015 figure? 300,000?

That would be an implied annualized return of 9%, is well documented that annualized return falls between 7-11% i.e. 17000 to 3,361,000.

[quote=“buyinghouse, post:2, topic:2760”]

Now, the market can go to hell for the rest of the year. You made 5%, and your principal is safe. 0% returns until the market goes through another recovery and bust

[/quote]Paltry return when compare to 7-11%.

Huh? What’s your take on 11% after taxes?![]()

Can you beat 8% tax free with a $1M death benefit? (if you get a premium of at least $1K a month).

Warning. Made up numbers alert. There should be a 10-page disclaimer on that.

[quote=“buyinghouse, post:5, topic:2760”]

Huh? What’s your take on 11% after taxes?![]()

Can you beat 8% tax free with a $1M death benefit? (if you get a premium of at least $1K a month).

[/quote]7-11% doesn’t include dividends, it refers to the appreciation of the index, not index fund. In any case, index fund guys are good, they know what to do, no tax payment involved.

[quote=“hanera, post:7, topic:2760, full:true”]

So, you don’t pay capital gains at all? Well, good for you! Keep the good job! ![]()

Now, you can lose all your money, can you? I bet you don’t have a conservative approach, right? We do, we don’t risk people’s money. Insurance companies work on what’s called options. The rest, doesn’t matter.

I like to debate with knowledgeable people like hanera. Very humble and never a conflictive attitude. ![]()

@buyinghouse What do you think the life insurance company does with the premiums? Where does the money go?