Looking for some opinions. We’ve got a property purchased in the SF Bay Area during the Great Recession for ~$275k. Property value has now increased to ~$625k. We moved out around two years ago as our family outgrew the place and have been renting it out ever since. Rental income is ok, we probably make around $500 a month after expenses, but for the amount of equity locked in the place we feel like we could be doing better.

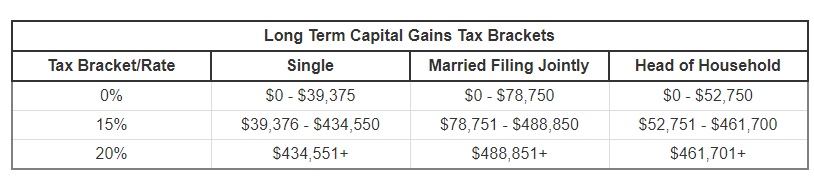

We’re now debating whether we should sell or hold on to it as a rental. On the one hand the property taxes are locked in at a favorably low rate due to California’s prop 13. On the other hand, if we sell within the next year we could come close to maxing our our tax free capital gain ($500k for a couple - we’re not quite there yet but given how Bay Area prices jump around it’s not inconceivable).

For the sake of argument let’s say we’re able to max out the $500k tax free capital gain upon selling. Would it be better to sell, or hold onto it as a rental and reap the benefits of prop 13 in perpetuity?

@Jil, yep it’s a 30 year fixed mortgage. You’re right monthly gain is actually $500+principal. Principal portion is about $300 a month. So total maybe more like $800 / month or $9,600 / year. I agree on the tradeoffs you list there.

@acre / Jil my initial thought was to re-invest the proceeds into more real estate. Sell while i can to get the tax-free gain, and roll that money into a bigger property with a larger mortgage (or two smaller properties). Basically more mortgage = more leverage which in theory means more appreciation gain down the road. I’ve tried to run the numbers and it seems like that works out if Bay Area real estate continues to appreciate by a healthy clip (~10% annually) but the problem i’m seeing is it’s hard to find a property that would be cashflow positive or even neutral at this point without a massive downpayment. And i really don’t want to buy a property that’s cashflow negative, holding on to it just for the appreciation… seems too risky…

You are right, it is risky to sell and reinvest it unless you want to have capital gain tax exemption.

If not, leave it as it is. If you lose the capital gain tax exemption, later use 1031 exchange for rental to multiplex where cash flow positive.

Presently, you can refinance (as mortgage rate is low) with cash out and use the cash out in any investment. But, you should be careful on investment whatever it may be.

For 1 & 2, he has to evaluate. If he puts everything in excel, he will definitely know which one is better.

without knowing his primary-rental conversion financials, I can only guess that by holding the home, he will be better with ever lasting cash flow (like annuity) for life as he locked 30 year fixed and locked prop-13 benefits. The home return (with mortgage benefit) will be better than cash investment in stocks (or at least same)

It is hard to exactly calculate without his financials and without his alternate proposal to gain better than current rental.

The 110k capital gain (lose when holding as rental) vs no of months * ( cash flow benefit of mortgage + prop 13 benefit )

If he calculates number of months, that is the break even.

For those who purchased homes between 2008 and 2011,locked with fixed mortgage, selling is not favorable unless they need money. Consider cash out refinance that may benefit. This is true for Bay Area homes, but not for outside as it depends on market

So far we have Just only calculated the cash flow, but not the appreciation. If the 650k home appreciates at 5% YOY, it comes to $32500 per year. With his initial investment $55k (20% of total purchase $275k), this is huge return.

He is almost getting $42100 yearly return with initial investment of $55000.

For those who purchased homes between 2008 and 2011,locked with fixed mortgage, selling is not favorable unless they need money.This is true for Bay Area homes, but not for outside as it depends on market.

All BA homes, bought during 2008-2011, are like your AAPL purchase 1998, ever lasting cash flow with decent BA growth.

I think that question came up a few time in the forum. Buy and hold/1031 til death is the way to go. If you hate risk, save the $500. If you love risk, cash out refinance and buy another rental. prop 13 Is going to save you more if you can make up your mind to hold perpetually.

Most of the old timers , retirees, are living in the home with prop-13. They live as long as they can and sell when they need money. This is their indirect retirement savings. Count in your home street how many are there and will they vote against prop-13? They are less in cities, but lot in suburbs. They are huge in numbers, silent but strong party of the economy.

Any changes, bills introduced against prop-13 will likely be voted down by people.

You only get to keep Prop 13 tax basis during your lifetime. When property is passed to the kids, it will be reassessed to market price.

It’s a good policy to keep roof over tenant’s head and owner’s head. I think Prop 13 has prevented millions of homeless people. Many tenants will not able to afford the rent without Prop 13. Many old owners will not be able to afford property tax on their SS.

I am convinced that Prop 13 is the most popular regulation in CA.

These is a proposal floating now to repeal Prop 13 for commercial properties. I think people are smart enough to reject that. Divide and conquer is always in their evil mind.

Don’t forget there are Prop 58 and Prop 193, which extended Prop 13 to exclude from reassessment property transfer between parents and children (58) and grandparents and grandchildren (193). So technically you can transfer your property to your niece and nephew without reassessment provided that your parents is still alive and cooperative . That show you how strong the Prop 13 voters support is.

If the advocates can get rent control established at state level, I don’t think prop 13 (and 58/193) are still that safe. The way things are going it’s just a matter of time.

The liberal politicians will keep trying. They have very little cost to keep introducing the same bills. It’s not like the anti-rent-control group can raise $100M every time. Even though voters have defeated prop 10 last year by a wide margin, it didn’t seem to mean anything to them and they just come back and try it again. One of those times it’s going to stick.

The political climate in CA has shifted. It’s the reason the liberals can keep coming back again and again simply because they can. To get something to pass they just need to overcome the technicality.

Prop 13 is stronger. Politicians can not change it behind the closed doors, it requires voter approval.

I think Prop 13 is very easy to keep since its impact is very direct. The senior citizens would be mobilized if someone wants to challenge it. The problem is that the evil mind is targeting commercial property only now, so it requires education for people to understand their evil divide and conquer trick.

Rent control can be changed by politicians and it doesn’t require voter approval. Also some voters don’t think deeply so they may naively think that rent contort has no impact on themselves

Media is trying to brainwash people and badmouth about Prop 13. But pocket is more powerful than the media. It only takes 5 minuets of thought to make a wise decision

If i were to sell i would intend to re-invest in real estate. I did spreadsheet it (or tried) and it seems like selling and re-investing in more Bay Area real estate could work out better than holding on if historical trends continue. But yeah i hate to give up the property tax rate.

I like the idea of using a cash-out refinance (or HELOC as someone mentioned in another forum) as an alternative way to leverage the equity without giving up the property tax rate. I’ll need to look into that more.