In 1996, mortgage rate is around 8%, inflation rate is 2.9%.

Today, mortgage rate is around 4%, inflation rate is 1.1%.

Over the 20 years, inflation rate decreases by 1.8%, but mortgage rate decreases by 4%. We got an extra 2.2% bonus.

Fed target inflation at 2%. Suppose we’ll reach 2% inflation in the next 2 years. In 1998, inflation was 1.5%, but mortgage rate was 7%.

Apparently the yield spread is very thin now in historic standard. If Trump can really jumpstart economy and make economy grow at 4%, which is similar to 1996 or 2004, mortgage rate could increase to 6% or even 7%.

I think that current mortgage rate might be too low and we could get a 6-8% mortgage rate during the Trump presidency.

Mortgage rate increases from 4% to 6% is equivalent to 20% price deduction. If income can grow 10%, then home value only needs to decrease 10%. But inflation expectation could still make the housing price flat.

Mortgage rate increases from 4% to 8% is equivalent to 35% price deduction. If income can grow 20%, then home value only needs to decrease 15%. But inflation expectation could still make the housing price flat.

So higher economic growth and higher mortgage rate will not cause a housing crash, but it could cause a flat housing price, or a slight drop.

The question is how economic growth can be achieved when base line interest rates are increased? It may take longer duration than Trump’s presidency, assuming two terms or at the end of 8th year. It all depends on how he (his team) directs the economy !

House prices are more about demand than mortgage costs…As long as supply is outpaced by demand prices will go up…Mortgage costs are only part of the equation, plenty of cash buyers and many that are willing to put more than the minimum down…

If Trump can not grow economy, interest rate will not go to 6% or even 8%. We do not need to worry about mortgage rate and inflation at all in that case. I only show that we do not need to worry about 4% GDP growth in case Trump can magically reach 4%.

FED is applying rate increase one quarter per year. They are unable to increase it faster than this. If I guess, the economical growth will be very slow.

I use to think buyers paid a high % of downpayment (from RSUs plus parent help) and a moderate mortgage loan. However, looking through Redfin, I am wrong:

Sunnyvale: Median Sale Price $1.26 mil, Avg Down Payment 13.3% i.e. $1.09 mil mortgage. PITI = $102k per year

Cupertino: Median Sale Price $1.75 mil, Avg Down Payment 20% i.e. $1.40 mil mortgage. PITI = $126k per year

Assuming household income should be at least three times PITI, Sunnyvale = $306k, Cupertino = $378k

Hard to believe right? I got a feeling they are stretching or need to sell RSUs regularly.

At 4.25% rate, 1.1M mortgage has a PI paymen of $5411. Assume a $1.375M purchase price, tax and insurance might be $1500. Total monthly PITI is under $7000. Annual PITI is $84k.

RE price is a lagging indicator. Decline usually starts at the end of the fed tightening. But sudden mortgage rate surge is definitely impacting the market. I am not worried about fed tightening now, I’m more worried about the mortgage rate rise much faster than inflation rate.

When last time FED raised rate, mortgage did not raise. This means lenders margin on their borrow and lending rate is reduced, but not any more.With Trump coming in and releasing the bank control, lenders are left with whatever they charge, hiked the rate to increase their margin. This leads mortgage rate goes faster than inflation rate that results higher profitability for the lender. It reduces borrower eligibility affects real estate competition.

No. RE price is a leading indicator. The fed increases rates in response to inflation. They don’t increase based on forecast of inflation. Inflation means prices and wages have been increasing. The whole reason we’ve had low inflation since 2008 is wages have been stagnant until very recently. RE decline is a leading indicator of future rate cuts, because the economy is slowing or in a recession. Interest rates lag, because the decisions are based on prior data of what happened. If your thesis of prices dropping when rates increase was true, then prices should have gone through the roof in 2008 when they were cutting rates fast. They cut rates by almost 4% that year.

Also, the idea that without GSE’s rates would be higher isn’t accurate. Other countries don’t have that and they have lower mortgage rates than the US.

The headline hype is dead wrong and anyone that’s done actual research on this knows the truth. It just goes to show how useless the media is at informing the public.

RE prices are changing based on various factors, not restricted to rates, but it is one of the factors affecting. Mostly, it is affordability, demand and supply.

But, RE price is not leading indicator. Rates increase decrease affect entire economy, that in-turn reflects in stock prices, then it lags to real estate. This cycle takes 6 months to 12 months. This is the main reason, when rates are raised,in booming times, stock prices and real estate prices are going up !

Take 2000 or 2008, when FED rates are increased every alternate meetings, stocks were going up and real estate was at its height. The FED rate is like loading the fast moving carrier every ton after ton until breaking point comes. FED loads the economy until breaking point and then wait. Since our economy was not so strong, FED waited almost an year, since Dec 2015, to hike another qtr point now. Presently, they do not want to go until breaking point, but see the economy is properly strengthened.

The focus of the FED is to have healthy growth economy rather than exploding/breaking in future. Since the outlook or aim is different, they are giving a long pause between each rate hike so that they can manage in case of future failure.

That’s exactly my point. It’s not just interest rate and price. That’s why home prices have never fallen in a year when rates were increased. Also, rates aren’t changed in a vacuum. Rates are increased/decreased based on lagging data. If rates are increased, then you can guarantee there’s inflation which comes from wage increases. If wages are increasing 3-4%, then people can afford higher home payments which drives home prices up. Gradual rate increases aren’t going to decrease affordability compared to the wage increase. Also, if rates are going up then you can bet the stock market has had a big run, so people have more for down payment.

Plus, the more confident people are the more likely they are to borrow close to their limit. If they aren’t confident (usually when rates are falling because the economy sucks), then they aren’t likely to borrow to their limit. You can see this when you look at the consumer savings rate which was lowest towards the end of the last economic boom cycle in 2007. People were so confident about the future that they didn’t feel a need to save. Once the recession started consumer savings rate actually increased, because people were fearful. The lack of savings to fall back on and subsequent increase in savings rate magnified the impact of the recession and made it worse than it should have been. 70% of the economy is consumer spending. If the savings rate goes from 2% to 6%, then it sucks 2.8% out of the GDP.

If they do cut taxes, we should get 3+ years of robust growth out of it. We’ve cut tax rates 4 times since WW2. The 3 years following cuts average 4.2% GDP growth. I think technology and globalization are deflationary enough to allow the fed to raise rates very gradually. I also think people under estimate the amount of slack in the labor market. We have the people that have given up on looking shown by work force participation at multi-decade lows. There are also all the part-time workers that want full-time work. It’ll take a lot more growth to put all those people to work full-time.

Back in 2010, people were talking about real estate losing value once rates started to increase. Everyone thought rate increase were around the corner. The fed didn’t increase until 2015. The fed forecasted 4 increases this year. At most, we will get one.

This could be the perfect setup for a massive bull run in real estate and stocks. We’re at market highs with energy and banks both doing horrible by historical standards. That’s 26% of the market. Banks are way below their historic market value compared to book value. Shale companies have gone from needing $80 oil to be profitable to $40 being profitable. Now that we’re getting some stabilization in oil, rig counts are increasing again.

Also, we’ve had a multi-decade bull market in bonds. That was bound to eventually end which will lead to significant cash flow to equities.

It sounds reasonable. How much really workable for US is still doubtful. We have challenging years coming soon.

First, Trump is firm on reducing corp tax to 15% that boosts all companies, but IRS will get very less tax. He wants to replace Obamacare with better (less expensive) ones. He has to subsidize that medical care. He wants to modernize Military, needs huge funding.

Medical care, Military and Social Security are the biggest portion of US budget. Deficit financing (Money printing) is mandatory which sets inflation.

Second, Trump also enforces 35% tax on jobs going outside or imports. This will strengthen US economy.

For both, Congress is very likely road block as it already started doing with vested interest.

In addition, even though Trump intention is good, whether US companies bring back job or bring back hoarded cash from foreign countries? We do not know.

Third, FED raise the rate slowly, may be once a year or twice a year, depends on inflation.

All these will show few years of Trump may be good, but eventually result into correction.

Trump may use various policy tools to boost economy. Even though we do not know the specifics, but it’s a safe bet that he will be successful to bring solid or even superb economic growth. It may take years for his policy to take effect, since companies and people need time to digest, make decisions and take advantage of his policies.

Robust economy will bring higher inflation and higher mortgage rate. Hopefully a strong dollar will help control inflation, but certain products and services which are not importable, will have much higher inflation than cpi. Rent is one of them, rent could inflate much faster than cpi, that’s true even during Obama years.

A rising rent and rising wage, job growth will be good for housing price. Higher mortgage rate will be bad for housing. I think more economic benefit of the Trump boom might go to middle class and middle to low educated people. Tech has been booming fir many decades and trump boom won’t benefit tech industry much, actually it could increase the cost for tech company.

Lowering the tax rate, allowing free repatriation of offshore cash, and allowing accelerated depreciation would create a huge boom. There’d be more capital investment, buybacks, and boosted dividends.

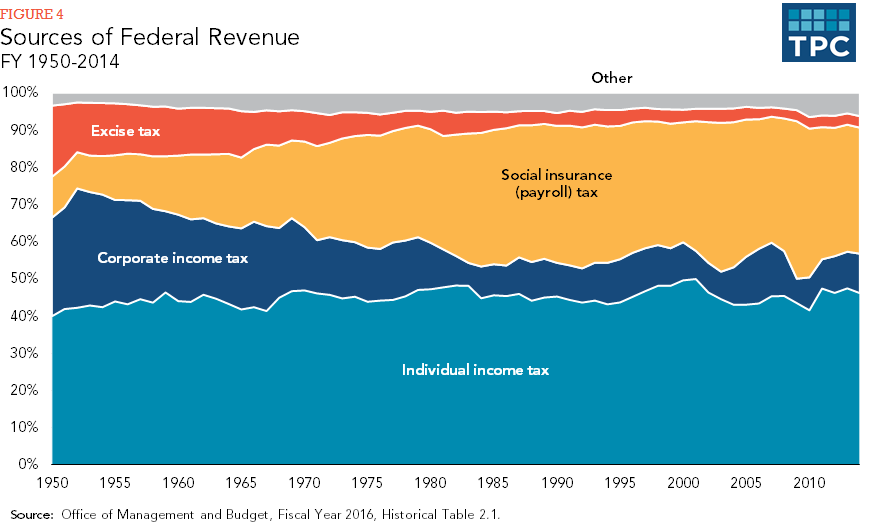

Corporation taxes aren’t that big of revenue generator compared to personal income taxes and payroll taxes. Also, they want to simplify by reducing deductions and credits. If they did that right, then they’d collect the same amount of taxes.