The long overlooked corner of the broad stock market — value investing — has started to gain momentum lately amid escalating trade tensions and an aging bull market.

The outperformance came mainly from disappointing earnings from some of the high-profile tech companies, including Facebook FB, Netflix NFLX and Twitter TWTR, that took a toll on the growth stocks. Additionally, rising U.S. debt and deficits combined with escalating trade tensions are weighing on economic growth, raising the appeal for value stocks amid improving fundamentals.

Growth investing dominated since 2009, time for value investing?

This company provides various gaming headset solutions to various platforms, including video game and entertainment consoles, handheld consoles, personal computers, and mobile and tablet devices under the Turtle Beach brand. With a market cap of $441.4 million, the company has an estimated earnings growth rate of 625% for this year. It belongs to a top-ranked Zacks industry (top 22%).

HEAR is a value play? WOT? How come it only mentions the earnings growth rate in the article? 625%?

What they call as value is like buying a home below its appraisal value. Same way, Hedge Funds and other experts calculate the value of a company and buy them. They analyze the company various ways and find out what is its current worth (just like appraisal - if they sell the company now) and derive at share price.

There are two difference ideas.

One Efficient market theory, i.e. market corrects itself by its value.

Another - Efficient market theory - is market, at times, skewed and not aligned its value.

It is not about blind buying, but buying a stock when it is below its value. This is where I admire WB after he purchased BAC for $5, AAPL at $99 and TEVA at $14.5

WB says AAPL is cheap, AMZN is expensive and has no comment on FB. Don’t try to be cheeky, you well know how intrinsic value is computed. It depends on your assumed no risk interest rate, net cash flow over at least 10 years…

Like appraisal needs analysis of various facts, company valuation needs lot of analysis. Like real estate no two appraisals match the same, no two analysts come up with same values. Since most of them predict what the company likely produce next 5 or 10 years, valuation may vary easily.

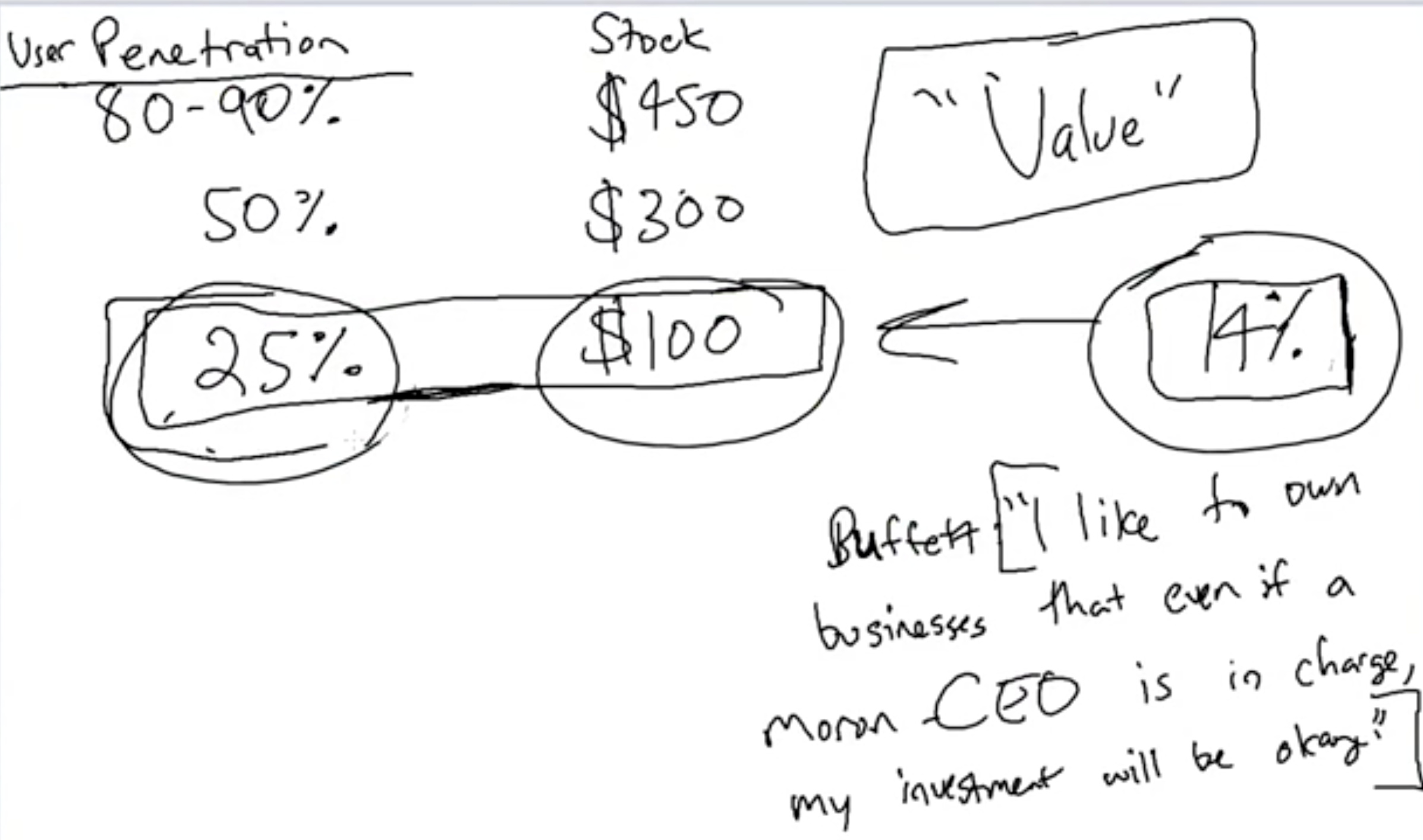

Very complex, but really good one from Martin Shkreli. Note, this guy is shrewd on the wrong side, now jailed (IIRC). This video is one hour, he teaches how to value netflix. https://youtu.be/HTM05cVOEDY

Whatever they do are just guidance for us as the ultimate trustworthy person we can see in the mirror !

BTW: There is no short cut, as this is pure appraisal of a company like AAPL, FB and AMZN

This is what WB or Seth Klarmann or any other fund managers do before they buy/sell equities. Their own analysis are confidential and is not available for outside world.

That’s his projection from March 2016. He said for the stock to go to $300 Netflix’s user penetration needs to be 50%, so it’s pretty nigh impossible. Fast forward to today NFLX is trading at $364.