Saw this on Financial Samurai today. It looks like a very interesting product. You take out a loan in exchange for a percentage of future appreciation. Loan term is 10 years 0%. If you don’t sell your house after 10 years you simply pay back the loan, 0% interests.

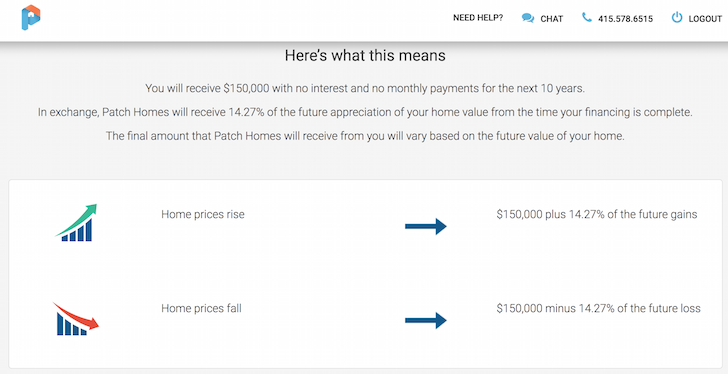

The Johnsons received $50,000 through Patch Homes. In exchange for $50,000, the Johnsons agreed to share in 25% of the future appreciation or depreciation of their home value.

Definitely, they will not award HELOC on depreciating home. They evaluate good appreciation homes and award HELOC.

My home appreciation (5%-7%) is higher than HELOC prime+0.25%. I would not sign up giving my home appreciation, rather pay HELOC interest rate just 0.25% over the prime.

IMO, this is risky one, esp for prime bay area homes.

One way they make money is upfront % charge for going through the process, and hope you haven’t sold in 10yrs so they get the appreciation% with new appraisal … its definitely risky for those who are not on top of their finances…

you need to have solid plan to pay it back within 10yrs…

The yield on the 10-year is 2.25%. They clearly think that either they’ll earn a higher return or it’s lower risk than a 10-year treasury. I wonder what their modeling for it is in terms of percent appreciation and default risk. If the owner stops paying the primary mortgage, then they are in a crappy position similar to any other secondary mortgage.

They must do something in the contract to make refinancing difficult. If not, then it’d be really easy for the home owner to refinance to pay them off and pay 0% interest to get 10 years of free money.

I thought about the same, but these are at their own discretion they can deny or accept the loan or change their terms of HELOC.

First, appraisal is always working against a borrower as most the refinancing appraisal comes 10% less than actual price. Lender have built-in advantage on low appraisal value.

They can estimate appreciation and bet on safer appreciation potential homes than others.

Similarly, they can choose borrower who is wealthy and better for long term than going with anyone less than 700 FICO.

They still have the risk of 2nd lien when economy goes south.

However, my question is who wants to give appreciation to them, esp well placed investor or primary owners?

If you want to keep your primary as a rental, but you need equity for down payment on the next home. This loan has no payment, so it won’'t impact DTI ratio.

If you want to use equity in your primary to buy an investment property without a HELOC which impacts DTI ratio.

From their website, it looks like you’ll have to pay back the loan, plus the portion dependent on home appreciation, at the time of contract exit(before or at the end of the term).

Quote from the above link: Can I exit the contract before the end of the term? Yes. You can exit the contract at any point of time before the end of the term. The final payment amount will be based on the home value at that time and the percentage share of the appreciation. There is no prepayment penalty or additional fees if you exit before the end of the term.

This almost sounds like a scam. If some borrowers sue them, this company could be closed quickly.

If you have a million dollar home, get 100k loan from Patch. Later your house appreciates to $1.5M. How much appreciation will they charge? Is it 25% x 500k x 10% = 12.5k? Or 25% x 500k = 125k?

They leave out an important detail… There is a “risk adjustment” to the initial home value, which can be 10% or more. So if you start out with a $1m home, the appreciation is based on $900K (or less). Which means that even if the house doesn’t appreciate it can still turn out to be an expensive loan (and hardly 0%).