I just found out as a business owner I can set up a pension plan for myself. And the tax saving is eye-watering!

Here is an example I found on “Dedicated DB”, a local company providing these kinds of plans:

RETIREMENT PLAN SAVING LIMITS For a Client Age 52 Earning $265,000

Jesus, so the taxable part is only 43K out of 265K!

W2 income sucks, unless it’s one you pay yourself. US tax system is rigged let me tell you… If you think corporate America is hurting for paying too much taxes, think again. You as individual may be paying too much, most certainly not businesses.

Like Trump said, Romney made the fatal mistake in showing his tax return. Trump’s return is 10x worse so he never showed it. Anyway I talked too much here and elsewhere I can never be a pol.

I heard of this defined benefit plan but did not spend much time to understand the details.

The fees for the plan might be very expensive. Also you are required to forecast your income so that you are able to contribute enough to fund your pension. There is penalty if your income falls and you can’t afford contribution any more.

Also if you have any emoloyees, you may have to provide the same pension to your employees.

It’s a tax deferred plan, you will pay tax when you retire and start getting pension income.

Can landlord qualify for the plan when you have sized net rental income?

Is this pension contribution also free from California income tax?

Business tax is not a good idea. I think we can get rid of business income tax and only tax for personal income, capital gain, sales tax. Business tax is a double tax that discourages job creation.

The best tax plan is owning rental real estate. …Depreciation and 1031s allow you to defer most taxes till you die…then its your heirs problem. .And when you are as rich as the Donald even that problem can be solved. .In fact his children are already part owners…And of course he plans on eliminating the etate tax…no taxes ever…

For flippers even cap gains advantages are disallowed…ordinary income, baby…But if you have a W2 income and flip only one or 2 a year, you are probably safe…Or you can use the Trump approach. .catch me if you can, push the envelope. …I think thats the main reason he doesn’t release returns…If he did every amateur accountant in the country would be looking to catch him up. .Like he and Leona Helmsley feel…Only the litte people pay taxes…

What’s the “catch me if you can” approach? I think Trump had a billion dollar loss during the Atlantic city bubble burst and used that loss to offset income in later years. Is there any other techniques?

Also there is the risk of tax audit. What’s the legal cost of tax audit? If there is a big legal cost and wasted time, it may not be worth it to use some approaches that attracts audits. The tax savings might be less than legal cost.

Fee is 2-3K per year. We are talking about potential savings of 60, 70K in taxes a year. Yes, you do need to predict level of income, but the plan years can be as short as a couple years. You can just make up another plan after 4 years as your income changes.

Here you grossly underestimate how much Uncle Sam hates workers and loves business owners. You can contribute peanuts to your employees but keep most to yourself. I will post an example later.

So you hate 401K too? That’s the same idea. There are all kinds of trickery you can play when you start getting distributions. I will worry about it when I hit 70 years old.

Sure. You guys should pay all the taxes and I should not pay any.

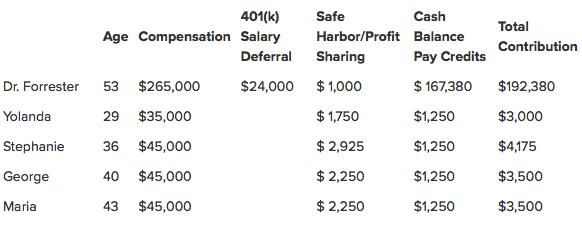

Objective

Maximize owner contribution and tax savings while controlling cost of benefits for employees

Profile

Dentist, age 53 pays herself $265,000 from her successful Periodontal and Implant Surgery practice. She is willing to make contributions for her four employees but wants to receive the lion’s share for herself.

Solution

OwnersPlus Cash Balance Plan + Safe Harbor 401(k) Profit Sharing Plan

Total 2016 Contribution $206,555

Estimated 2016 tax savings $78,490*

Dr. Forrester will receive 93% of the OwnersPlus contribution toward her own retirement.

Profile

Architect, age 48, has an S-Corp and pays himself $185,000 in W-2 income in 2016. He wants to save as much as possible this year but he wants flexibility as his income fluctuates.

Solution

OnePersonPlus Defined Benefit Plan and an OnePerson (k) that he funds only in high income years

Defined Benefit only Defined Benefit + 401(k)

2016 Contribution: $136,600 $165,700

Tax Savings@ 38%: $51,900 $62,900

Projected Defined Benefit Accumulation at age 62: $2.24 Million

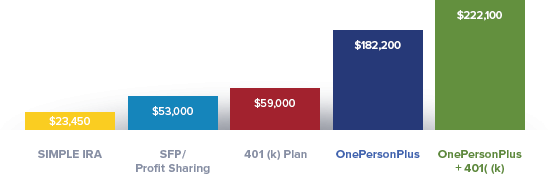

This is the most straightforward. High income year after year and no employees:

OWNER-ONLY BUSINESS

Client Objective

Maximum contribution and tax deduction

Profile

Business Strategy Consultant age 52, set up an S-Corp for his solo practice. He wants to grow his retirement assets quickly and reduce his tax liabilities. He pays himself $300,000 in W-2 income.

Solution

OnePersonPlus Defined Benefit Plan for 10 years, combined with a OnePerson (k).

Defined Benefit Only:

2016 Business Contribution: $182,200

Tax Savings @ 38%: $69,200

Defined Benefit+ 401(k):

2016 Business Contribution: $222,100

Tax Savings @ 38%: $84,300

Projected Defined Benefit Only Accumulation: $2.54 Million in 10 years

Very attractive plans. Who’ll control the investment decisions of the pension fund?

I need to have a business and generate a lot of business income before considering this. It’s definitely worth the cost of a couple thousands a year.

I hope they will increase 401k limit to the same amount for self employed. Of course, self employed people are creating jobs for themselves, and some day, they may start creating new jobs for others.

Found an old NYTimes article on these pension plans.

The fees is not as high as they claimed. That’s what I read from the company I referred to above. Not sure if there is any hidden fees. Seems you need to stick to it for at least 5 years, and are free to roll it into your other retirement savings account afterwards.

Yeah!! That is absolutely one of the best reasons to be self-employed if you have a spouse who is regularly employed here in CA. I am always on the lookout for tax-deductions whether it’s donating clothing or whatever. My husband thinks it’s weird (well, I think it’s weird that he’s so happy paying a buttload of taxes). If I can GIK it, I do. But my income on top of his would be taxed crazy amounts. In fact, I really wish I could just have no W2 at all and put it into retirement, but apparently you do have to pull in W2 income to get the 401K and retirement tax-deductions.

I set up my business as a LLC and all the profit is filed on Sch C as income. I don’t give myself W2. To do that I’d need to file as an S Corp. There are pros and cons between LLC and S Corp. I may go S Corp in 2017 or 8.

I have also set up an 401k for my business. If the business’ profit is high enough, potentially I can put in over 100K of contribution into it. Every. Year. I will look into setting up a defined benefits plan too in 2017.

For people who are younger than 50, they can only use SEP or 401k.

If you have a W2 income and already contribute to maximum 401k, can you still contribute to SEP and self employed 401k? It could be a good tax solution for second source of income.

For those with W2, now-a-days most employers offer After-tax 401K that has additional limit of 35K (53K yearly limit regular 18K 401K and this 35K). But beauty of that is it can be converted to Roth IRA. It is after tax but tax free gain for either stock or realestate (with SDIRA).

You can be an independent contractor in your own business? Someone advised me that that is not possible. I issue myself a W2 for that reason. And a K1. (LLC taxed as S-Corp)

I will look into setting up a defined benefits plan too in 2017.

I will look into setting up a defined benefits plan too in 2017.