After Debt is removed, we can go for Home Mortgage and that should be the only loan !

1 Like

Why pay off your debt if interests rate is lower than investment return? Shouldn’t you funnel the money to the investment instead of paying off debt?

1 Like

There are good debts and bad debts. Some of the debts, especially investment based on loan/student loan, leads to bankruptcy. Even the student loan at 2.8% is not so attractive like mortgage. Other investments (like stocks, etfs) are riskier, not good to invest loan amount into those investments. This will put the borrower double negative mode and domino spiral effect during downturn or correction.

All debts are not good except mortgage debt.

1 Like

Having too much debt is swimming naked in high tide. Investing in SFBA’s RE since 2009-2011 is high tide… doesn’t make you a genius… survive the next downturn, then we talk. Financial prudence means your lifestyle should not be affected by the downturn. Make sure you don’t lose in any situation. Winning is a bonus.

3 Likes

I wanted to do similar but my better half lives the house very much. Based on logic only, what you did is the wisest but humans especially ladies are very sentimental😞

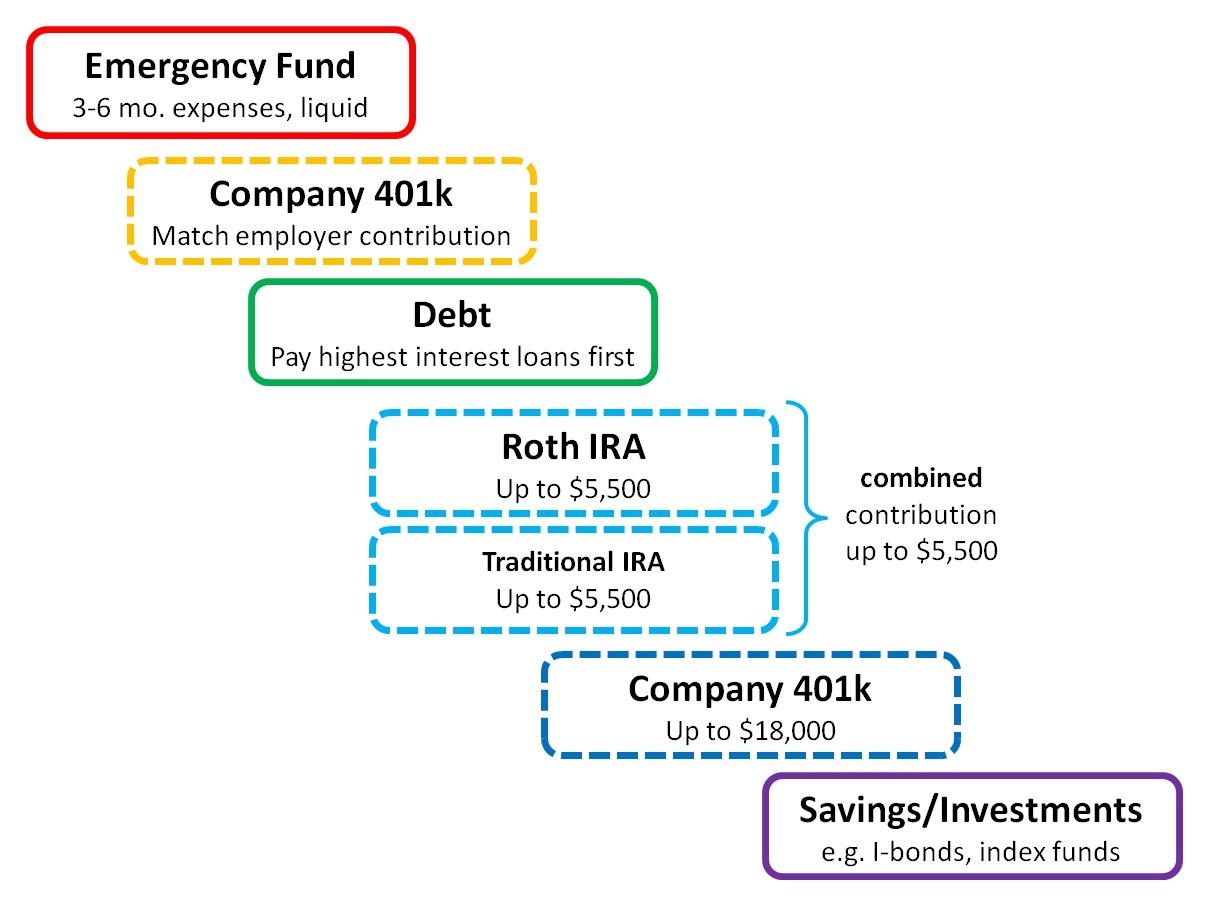

Is 401K that I can borrow against to cover my 3-6 mo expense, good enough as emergency fund? Do I have to have cash in checking account to be considered liquid?

That is what I am doing. I do not have any emergency fund but I know I can borrow if I need them. Am I the only one doing that?

I say just have a few credit cards you can take cash advances is enough. After all, it’s “emergency” so a point or two should not be a big deal.

I never had any major emergency other than down payment for a home.

If your 401k has loan (up to 50k) provision, Yes, 3-6 months emergency funding is fine. Only true emergency, you will get 401k loan.

HELOC can also be used for emergency fund. If someone has home, just have HELOC as your emergency reserve. I have been doing this for almost 10 years. Unless you withdraw, there is no interest and also tax deductible.

This is the main reason, I do not touch 401k loan, but use HELOC. Nowadays, I have cash in taxable investment balances. No need to touch 401k or HELOC.

401k is not an emergency fund. Odds are you only need the emergency fund if there’s job loss. If you lose your job, then you can’t borrow from it. You’d have to withdraw, take the tax hit, and pay the 10% penalty. If you do a 401k loan and lose your job, then it’s usually due in full within 30-days. That happened to a co-worker. He used a 401k loan for the downpayment on his home then got laid off. That has to be brutal.

3 Likes

Not an expert, but you know, going to seminars, listening to people with 30+ years in the field you learn one or two facts.

There’s this theory that 401K is going to be your savior when you retire. Wrong! Why? Because of taxes to be paid and the logic that is an account that has to be withdrawn at certain age or you will be taxed the hell out of it. Also, you may not be contributing into it anymore, but the management fees will be charged until you cash it in. They will eat your 401K up to 50%.

I may add, the market goes up and down, and most often down than up, killing what you made in a long time with only one day of bad trades in the stock market. 2008 has the best example, people lost about 38.5% that year. Add to it the tax bracket you are in at that moment, which certainly won’t be 0. Remember, you are an investor, so all your income from rentals, 401K, bank accounts, stocks, any taxable investment or return, whatever they can throw at you will count. You won’t be 0 tax bracket, believe me.

People about to sign their retirement in 2008 were forced to return to work for Walmart or McDonald’s.

The best thing you can do with your money is to put it into indexed accounts. Your principal is safe, and still you got a cushion of 0.25 floor, more or less, but you won’t lose your money.

It is established that you will deplete the 401K $ in the first 3-5 years of you pulling money out of it. Money used, money spent, gone, no replenishment. Management fees still apply. About 24 different fees not shown but charged to your account. Google it.

I have suggested a few of you to get a life insurance policy with living benefits.

I will be back later, I am going to meet some clients right now. See ya!

Thank you for the scare. However, I don’t have social security and 401K  but paid a lot of taxes. I really want to get out of USA

but paid a lot of taxes. I really want to get out of USA

1 Like

That some funny stuff. You talk about 401k management fees. What are the sales commissions on the life insurance policy? That’s the same as management fees. That money is paid from the investors money. I always roll my 401k to an IRA. I pay zero management or maintenance fees. Most of it is in SPY with a low expense ratio.

2 Likes

As of now, 24 trillion dollars are there in 401k. 401k is a big subject. There are many ways to make use of it.

You will be taxed the hell out of it:==> Not right, you have Roth 401k, Roth IRA and Backdoor Roth. These are tax paid when put money, but not taxed when you take it. This can be done with earned money alone.

Here is how I asked my son to follow, he is in his early 20s. When he was in UC college, he earned money through summer jobs. I asked him to max his Roth IRA. Since his pay was less than 15k, he paid very less tax, but $22000 went to his Roth IRA in 4 years.

This year, he has got full time job, but 4 months pay alone. Bingo, his tax will be less than $2000 this year ! But, I asked him to fully max out Roth 401k, yes another $18000.

Eventually, he makes $40000 in Roth by the age of 21. If the money grows at 7% for 40 years, he gets 600k, 8% is 868k, 9% is 1.25M and 10% is 1.8M. He gets tax free money at 61 or after. He won’t pay any tax on it when he takes it !

Even if inflation is 2% - 3%, his retirement money is set at the age of 21 !

When I told him about this, he could not believe it. When his friend, UC Berkeley graduate & Vanguard trainee, told him the benefit of 401k, he understood completely and agreed to max out Roth 401k.

You need to master this art of savings,investment and tax advantage schemes.

1 Like

Put your money in real estate not 401ks…If you get employer matched funds go for it…Otherwise buy real estate with a self directed sep ira

1 Like

Real estate is good for experienced people and high cash initial requirement.

401k is good for normal savers, beginners etc. Once a comfortable stage is reached in 401k, people can dive into real estate.

Of course, early primary home is important step in real estate before making real estate investment !

On any case,balancing both will give better learning and opportunities.

More important to buy your own home first before worrying about retirement. .

2 Likes

Jil has already bought that for his children ![]() , me similarly for my two sons

, me similarly for my two sons ![]()

401k is good for high earners, since you immediately get 40% more for your money. You pay taxes when you withdraw, but you can organize withdrawals to minimize taxes. If I’m in a higher tax bracket during retirement, it means I did really well and I will gladly pay those taxes.

For high earners, $18k max of 401k is just a tiny portion of your investments. Plenty left over for RE.

1 Like

Start your own business. You can put more than 100K into your own 401k. Right. 100K.

You mean including a spouse? Cause self-employed max is still only $59k including 50+ catch-up.

Anyways, yes I would love to put that much in. If I had the ability, I would do it.

1 Like