Hard to see how the risk is one of liquidity and not solvency. For years now banks have been writing 3% paper. We’re in a 7% market and it may not be transitory - these types of moves can go in super-cycles that last decades. Top of the last rate cycle was about 1982; low was in the 1940’s. Last 10 years or so may have marked the rate bottom for this cycle.

Note second paragraph, last sentence.

.

Is what insurance is for ![]()

The Fed put out not one but two lending facilities. Banks can put up their underwater agency and treasury papers as collateral and take out loans (very critically) at par. No haircut no nothing.

Some say the unofficial QE has started again.

![]()

3 Likes

United States of Crooks will never change.

Privatize the profits and socialize the losses.

https://twitter.com/michaeljburry/status/1635060780042457088?s=46&t=VR3a2_t7NGq2guWtXAVrzA

This plunder has been going on for years and sheeps still don’t get it and wonder what’s causing this inflation.

This country needs a revolution to get back to track else it’ll die a slow and painful death.

Janet Yellen has balls to go on national TV and lie through her fake teeth’s that it’s not a taxpayer bailout. What a disgrace.

In reality it is a bailout at taxpayers expense. The taxpayer is buying SVB investments at face value which is a premium over market value. Taxpayers are losing money because government could be buying other investments at market value and not for a premium.

2 Likes

Haha so funny. There is zero evidence of contagion. It hasn’t been 48 hours. This is like a white woman calling the police because she saw a black man in the neighborhood. Zero evidence the gov’t needs to do anything, and here they are calling out the SWAT team. But they’re doing it, because can’t have anything bad happen to the rich even if the rest of pay the price.

Well another bank in NY collapsed over the weekend. So in one week 3 banks failed. I wouldn’t call it “zero evidence” of contagion.

Better be safe than sorry. Imagine if Lehman wasn’t just casually allowed to collapse. Probably the single worst decision in modern finance.

On September 12, Timothy F. Geithner, then president of the Federal Reserve Bank of New York, called a meeting on the future of Lehman, which included the possibility of an emergency liquidation of its assets.[18] Bankers representing all the major Wall Street firms were in attendance. The meeting goal was to find a private solution in rescuing Lehman and extinguish the flame of the global financial crisis.[19] Lehman reported that it had been in talks with Bank of America and Barclays for the company’s possible sale.[18] The New York Times reported on September 14, 2008, that Barclays had ended its bid to purchase all or part of Lehman and a deal to rescue the bank from liquidation collapsed.[20] It emerged subsequently that a deal had been vetoed by the Bank of England and the UK’s Financial Services Authority.[21] Leaders of major Wall Street banks continued to meet late that day to prevent the bank’s rapid failure.[20] Bank of America’s rumored involvement also appeared to end as federal regulators resisted its request for government involvement in Lehman’s sale.[20] By Sunday, September 14, after the Barclays deal fell through, the news of impending doom swept through Lehman, and many employees arrived at the headquarters to clean out their offices. By Sunday afternoon, the government summoned Harvey Miller of Weil, Gotshal & Manges to file for bankruptcy before the markets opened on Monday.[22]

By the way, because how the Lehman episode unfolded, central bankers everywhere now lean heavily towards saving big banks than not saving. The horror of 2008 is still fresh in many people’s minds. Powerful people at the helms today like Powell and Yellen had front row seats watching the whole thing went down in 08.

Crony capitalism & fear-mongering reign supreme in America. The FDIC only insures deposits up to $250,000. By selectively changing the rules after the fact for SVB, the U.S. government now incentivizes greater risk-taking by banks & depositors in the future, teaching large depositors at smaller banks that they can simply throw money at risky banks without diversifying or conducting diligence (just like many tech startups did here). Smaller banks like SVB lobbied for years for looser risk limits by arguing that their failures would not create systemic risk and thus would not merit special intervention by the U.S. government, but Secretary Yellen’s announcement reveals that argument to be a farce.

And it’s surprising that some people support this day light robbery from Taxpayers to enrich the rich again.

1 Like

Banking system as a whole is in a very bad shape because of Fed’s crazy rate hikes.

1 Like

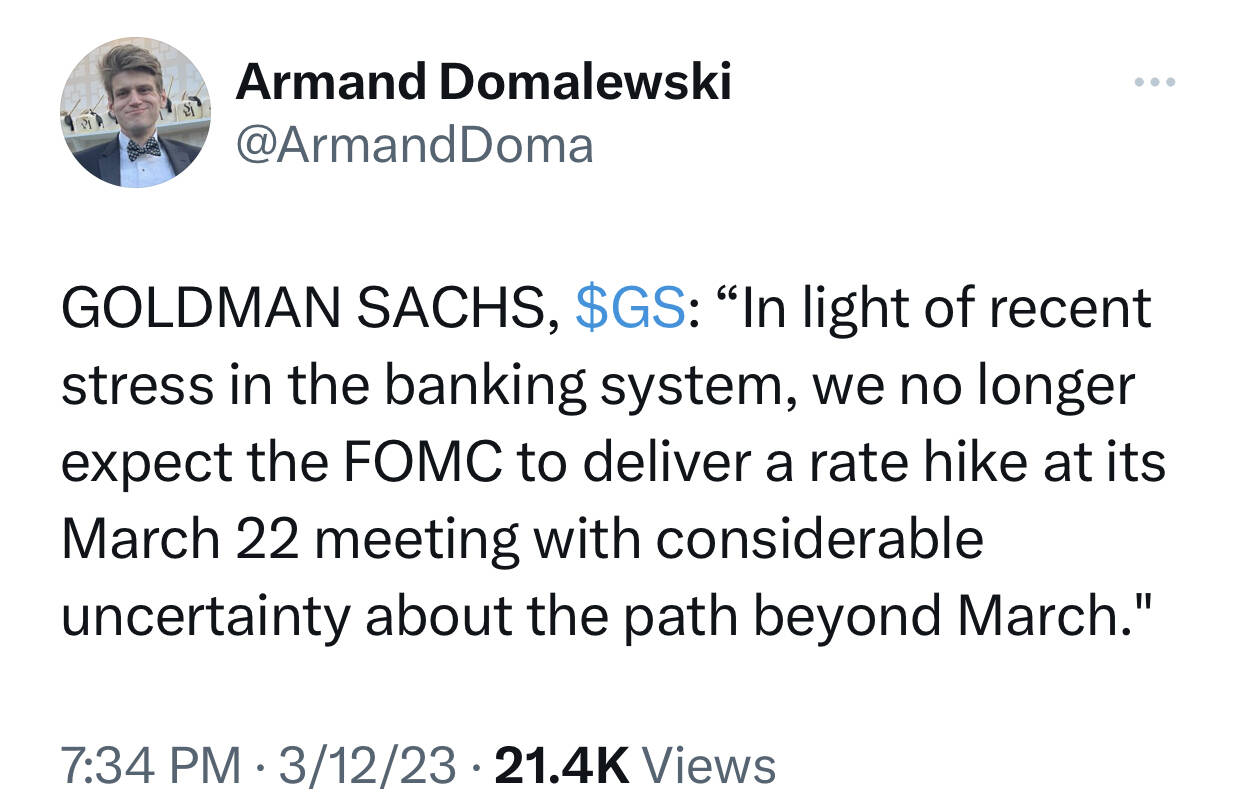

Goldman now predicts Fed will pause rate hike altogether in the next meeting. I am not sure I will go that far but HUGE if true.

.

More like rich and politically powerful. Rules of law are for ordinary folks. Certain people has unequaled rights. The leadership of SVB will go scot-free.

That’s missing the point. They probably did intend to hold those bonds to maturity. Banks are regulated in how much cash they need to have.

10% is nothing. They had $174.5B in deposits, so they needed $17.5B in cash. The withdrawals were $42B or more than 2x their legally required cash. They had to sell assets to raise the cash.

That’s also not an instantaneous process. It takes time for transactions to clear and cash to electronically transfer.

The fed had to step in, since I’m sure most banks would fail if they had that rapid of withdrawals above the required cash amount. The only thing holding the banking system together is people being calm. Imagine if one of the major banks had to start liquidating bond assets to meet withdrawals from depositors. They are so massive that it’d crash the bond market creating a snowball effect.

2 Likes

Contagion going international.

The sale of $26B bonds that resulted a modest $1.8B loss was before the $42B withdrawals. The practice pointed out by the twitter is pre-$42B withdrawals (and pre-$26B sale).

Is it a prudent practice to hold $120B of securities vs $173B deposits?

$57.7B HTM vs $173B deposit, prudent?

Is $151.5B uninsured the correct number? Media reported 3% insured. 151.5/173 = 87.5% uninsured. Total 3+87.5 is less than 100%, there are some classified as not insured and not uninsured?

Commercial banks usually try not to borrow from the lender of last resort because such action indicates that the bank is experiencing a financial crisis.

Did SVB try to borrow from Fed or other banks before the sale of the $26B T and during the fast $42B withdrawals?

They let the regulations. Someone should have done analysis when they determined the regulations. I’m sure they have data on max percent of deposit is withdrawn in a day, week, and month. What happened is an extreme statistically outlier.