Opinion piece ![]()

Thinking aloud, may be should move all SVB articles to a single thread.

Someone should write an article, what individuals can learn from this event.

Opinion piece ![]()

Thinking aloud, may be should move all SVB articles to a single thread.

Someone should write an article, what individuals can learn from this event.

Fact check: true.

I want to know who knew what and when. They didn’t disclose anything until March 8th. All the regional bank stocks start to take on March 2nd or 3rd. They were in free fall a full 3 trading days prior.

Does FDIC insurance have enough funds to cover ALL depositors like they did for SVB? My guess will be NO.

Woke policies go against bonding by men. Men bond by insulting ![]() and fighting each other.

and fighting each other.

That is what I worry about. We’ll know a few months down the road. Could have a Lehman Bros moment after this Bear Stearns event.

Ok let me rephrase that. The Qn was incorrect.

Does FDIC insurance have enough funds to cover ALL depositors in @10 small/medium banks like they did in SVB?

FDIC has about $130B to work with insuring depositors at the $250K level.

Deposits at US Banks equals $22T.

There isn’t a genuine backstop other than Printing. Printing = Inflation. Printing will at sometime may = Weimar Republic levels of hyperinflation.

We all know what followed thereafter.

My .02c

Didn’t FDIC return for all accounts in SVB even return above $250K? Can they do exactly the same for 5 other banks-Answer NO. So, by doing what FDIC did with SVB what is the message it’s trying to send to the rest of the economy? To me it’s just a message which has no legs, i.e. PR/marketing exercise and short term fire fighting. In fact by sending this message what kind of long term down stream effects it will create long term who knows.

OR

Is it now the case that large corporate deposit holders(I hear many corporations/llcs/startups had lots of money at SVB) are now more important than Moms and Pops @$1-2M accounts?

This is not how it works. FDIC only has to pay the difference between liabilities (what the bank owes the depositors) and the bank’s assets. Remember, bank has assets too. Because of regulations it’s likely to be high quality assets.

At SVB I saw estimates assets can cover more than 90% of the claims. So that 130B of FDIC fund can cover more than a trillion dollars worth of assets.

Government guarantee is not simple PR. Because of the guarantees bank runs are far less likely to occur in the first place.

Almost.

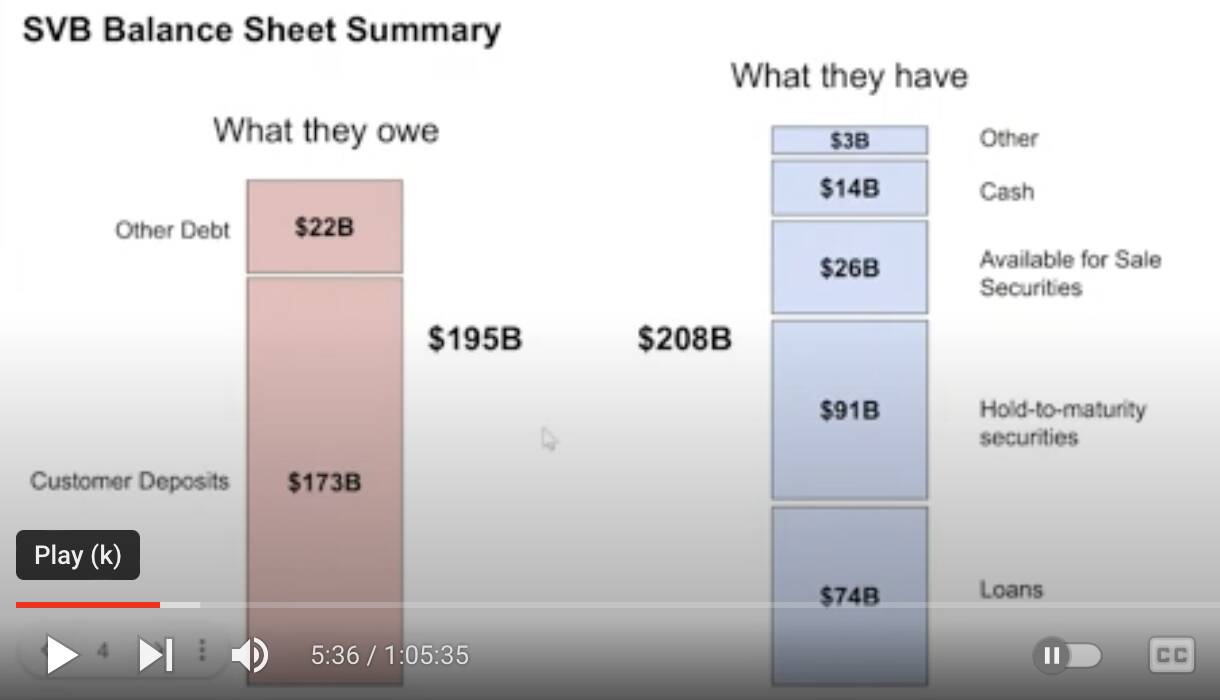

There is an assumption here that an asset will first be of any value, and secondly that there will be a buyer for that asset. Treasury obligations have value, but not in a rising rate market and buyers for those Treasury obligations will not go forward at X value if it’s not real. This is the key reason SVB fell. They sold assets of value (at the time) by discounting them from their face value. Thankfully there were buyers for some of those assets. You can’t count on buyers willing to pay for a declining value asset as a possible backstopping bridge of the FDIC’s shortfall in coverage.

The math for depletion alone of $130B at $250k is 520,000 account holders. Let’s say its 2x that number or 1.4 million account holders with at least $125,000 in the bank. It’s pretty easy to accept (in my view) that there are at least 1.4m people in these United States with $125k in their insured account.

I’m not sure how many account holders were at SVB, but Wells Fargo has 70m account holders, BofA has 46m account holders, Chase has 18m, etc, etc, etc. A panic starts, and 1.5 percent of account holders in just these three banks alone could drain the FDIC’s ability to guarantee funds.

MBS

CMBS

Loans to startups

Not sure about what the message is on this. I’ve read that MBS and CMBS were some of the “bonds” in the Vox article SVB had to sell at a discount - along of course with long term UST’s. Loans to Startups are vaporware - fungible if the idea works, not so much if the idea is really akin to Beanie Babies or Tulip Bulbs in their relative value to an idea like YouTube. Yes, there is a buyer for everything, at what price is another story.

Large US banks inundated with new depositors as smaller lenders face turmoil

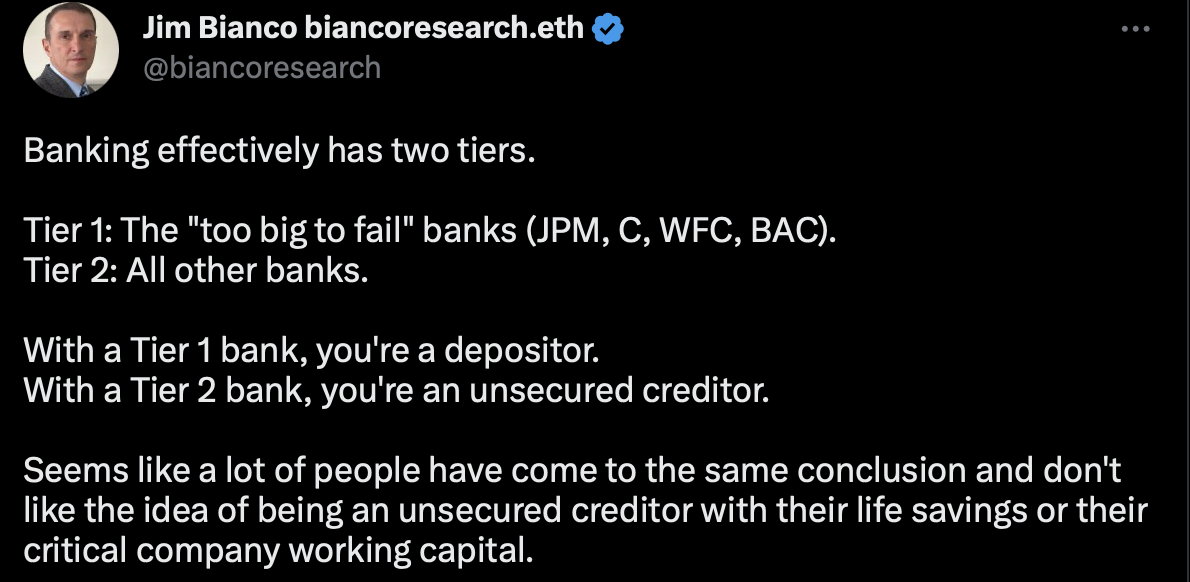

I learned that from 2008 GFC. Anyhoo, you can increase FDIC coverage per account using all kind of techniques. I have accounts with JPM, C and BAC (dropped WFC) and each account is insured up to $1M. I closed all the accounts with Tier 2 banks.

In a statement to DailyMail.com, Will Hild, the executive director for Consumers’ Research, said: 'The bank suffered from a combination of senior officers more focused on identity politics than risk management and investments in unprofitable virtue signaling boondoggles, like reportedly financing 62 percent of all US solar projects.

‘It’s also poetic that SVB would be the first bank to fail from “going woke,” as the general business culture in Silicon Valley itself is notoriously far left and similarly out-of-step with the rest of the country,’ he said. ‘Let this be a warning, not just to other banks, but all of corporate America: Focus on serving your customers, not woke politicians.’

Meanwhile, Republican presidential candidate Vivek Ramaswamy wrote in an op-ed that ‘SVB intentionally decided not to hedge its interest-rate risk.’

‘Either SVB was incompetent or this is a case of moral hazard, taking excessive risk and expecting political favors and bailouts,’ he wrote as he railed against the idea of a bailout for the bank — something Treasury Secretary Janet Yellen said on Sunday is not on the table.

A risk flying under the radar is that so many people will move their money from small community banks to larger “too big to fail” banks that the industry will effectively be monopolized. This will allowing them to charge whatever fees they like. Worse still, they will only fund “woke” investments. The incestuous relationship between media, social media and government will spread to the banking industry. No freedom of speech followed by no access to capital. Folks should be encouraged to resist this.

That has been happening since the financial crisis. They said the problem was banks were too big, so they made them even bigger. The public has the attention span of a goldfish, so the government can do that type of idiotic behavior with zero consequences.

The government really shouldn’t ban TikTok. People might have more free time and start paying attention to the government’s incompetence.