Most people buy for stability and schools for kids not tax deductions. Most people I know were firmly in the “renting is better”camp until they had a child. Then they quickly became buyers.

You’ve used itemized… $10k for SALT and $40k for Mortgage Interest… I used $24k standard deduction.

Latest combined version allows mortgage interest deduction of old mortgage… so can itemize.

Not even sure we are talking about the same thing. If you’re talking about my 2nd sentence of my previous post, not talking about tax reform. Didn’t realize I have a fairly tax situation.

Not supposed to be here. I was replying to current tax amount versus proposed tax amount using the web site for calculation. My current is only off by less than $200 and I’ve been using turbotax since it’s inception.

Are you saying you’ve a tax savings of $200?

My situation is:

My actual tax paid last year is much less than that computed by the web site. This is what I’m trying to figure out. And the difference is not due to the computation of the fed tax. Is because the web site is too simple for computing California tax rules. I am trying to figure out how to compute tax under the California tax system… seems a lot more complicated than the fed tax system.

The current tax liability as computed by the web site is identical to that computed using my spreadsheet.

No or positive impact?

Current primary residence home owners with an existing mortgage - Happy with tax savings.

Aspiring primary residence home owners who are current renters and want to use mortgage - Very unhappy because of less disposable income.

How do you feel people with this purchase price react after tax reform in place?

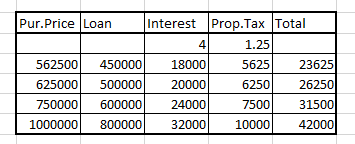

They still get to deduct interest up to $750k loan. That should cover $1M purchase price with 25% down. The property tax will hit the SALT limit, so they won’t be able to deduct state income tax.

The web site says I pay $200 more with the new tax bill. I also did a rough calc on my own and came up with around $200 using 2016 numbers as well.

I’ll join the chorus that say it’s time to get married ![]()

3 Likes

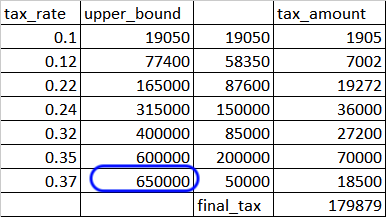

Assumptions?

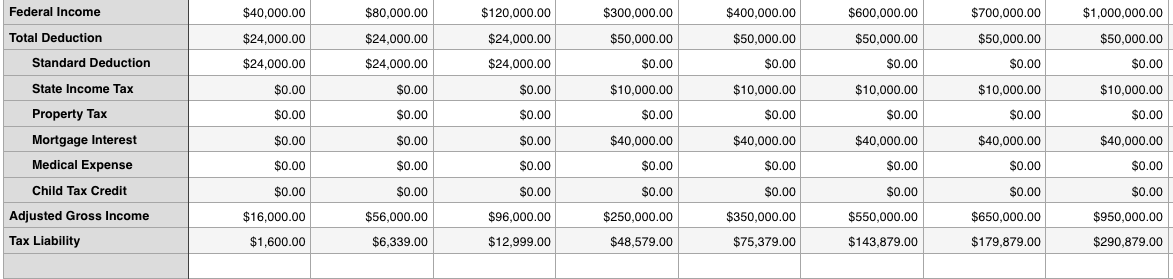

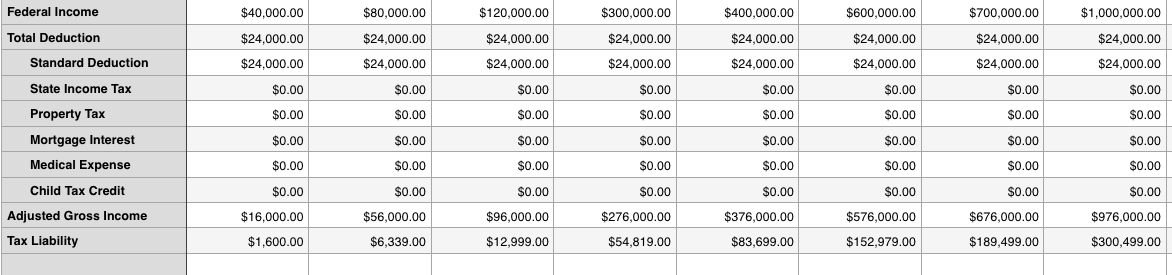

Above table seems to have used property tax deduction of $10k but no mortgage interest deduction. Shouldn’t the table be constructed using standard deduction of $24k?

So every $200k-$1M household income BA primary home owners with a mortgage would be happy since all have tax savings ![]() i.e. dougz’s claim is wrong.

i.e. dougz’s claim is wrong.

Itemized $10k for SALT and $40k for Mortgage Interest of existing mortgage

Standard deduction $24k

Jumped with joy?

This table is for people with mortgage higher than $14k and thus do itemized deduction even after reform.

Now that mortgage deduction is applicable for both AMT and reform (at least for existing home owners. For new home owners, they have not deducted their mortgages so far any way), income in my table really means “AGI-mortgage”. I assumed this to simplify the calculation.

See that Condo buyers, joint filing, may not get tax break as standard deduction are better for them.

With 750k ceiling, max benefit people can claim itemized is appx $40000 (10k property tax and 30k mortgage interest) while standard deduction is 24k.

The max benefit is appx 16k difference. It encourages cash purchases or claim standard deduction.

Hereafter BA homes will take absolute value growth and direct mortgage rate, but not depended on mortgage+property tax benefits.

Forever can’t buy the ideal house unless invested in bitcoin:blush ![]() or buy lesser house with cash

or buy lesser house with cash ![]()

Thought you meant already purchased.

Thought MI for $750k is $15k-$18k.

1 Like

Comparing AGI-mortgage doesn’t sound like apple to apple comparison because marginal tax rate of the earned income at which the mortgage interest can be deductible against is different, higher deduction for current tax code. The tax savings/hikes (preferred this than gain and loss) picture is quite different once you account for the mortgage interest into the computation.

Anyhoo, every households in SV with a household income of $200k-$1M (with or without an existing mortgage) would be happy since all have tax savings provided that the federal and state earned income is the same ![]() i.e. dougz’s claim is wrong.

i.e. dougz’s claim is wrong.

The mortgage is attractive above 400k loan and below 750k with rates ranging from 4% to 6%(future). I am sure lot BA people will take advantage at this range with 10k property tax.

There are chances lot of condos will fall into rentals as investors buy them ,but primary seekers will avoid range under 600k.

This is good, makes it hard for marginal guys to buy expensive houses in SV.

For $1.5M house, need $750k cash ![]() 20% downpayment doesn’t work well.

20% downpayment doesn’t work well.

Long term, more stable RE market.

Short term, may depress the price ![]() since a group of demand is removed.

since a group of demand is removed.

1 Like

90% of people will take standard deduction and not itemize. That means 90% of people could do their taxes on a post card.

1 Like

Most countries have no mortgage interest tax deduction, but mortgage is used everywhere. Don’t underestimate people’s adaptability. Pretty soon, everyone will continue to get 1.6M mortgages without a blink.

It’s going to be nothing in 6 months, no one would care about it.

What percentage of people bought a house for tax deductibility? It’s a media invented myth.