What does level 4 mean?

it does not mean anything to me, other than that is their company’s name:

1 Like

I see. I didn’t realize it was a company’s name. I thought it was some kind of industry thing.

Thanks.

I got this information from a guy I know. It sounds to good to be true.

Commercial loans, from $250K+

Initial deposit of 3% of the total amount.

10,20,30 years loan.

Fixed rate of 3.5% to 6.5%

There’s a 7% broker’s fee at the backend of the loan, which means there are no “out of pocket” expenses for the clients.

Residential loans $250K+ and no cap

1% fixed amortized interest for 30 years

Initial deposit of 3% of the total.

Clients are elegible for loan forgiveness. Loan will be forgiven after 15 years if paying on time. Late one time, the deal is off.

They offer this for a refinance loan too.

2 Likes

That has scam spelled all over it

1 Like

Apartment loans.

No way! ![]()

![]()

I used to get such letter bait, just to get buyer’s attention to call them, that directly lands to Trash can.

Unless someone really get a loan, we have no way to know whether these letters are genuine.

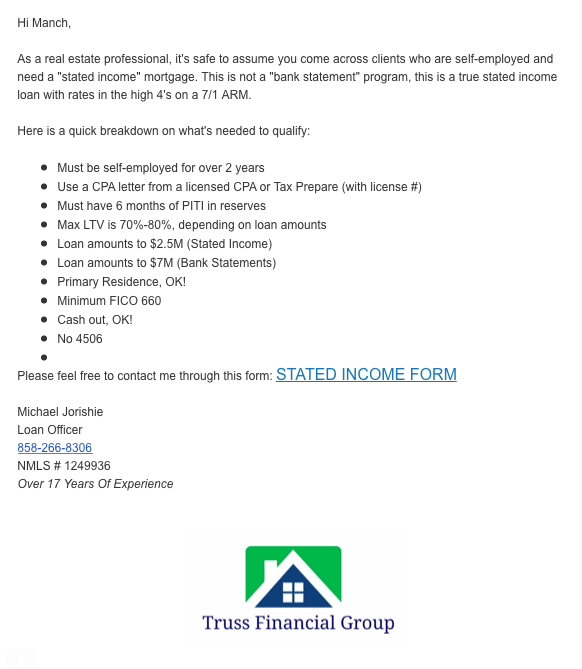

It’s only for self employed and needs CPA letter.

For bank statement loan, maybe you can have a bank account to deposit the rent but no withdrawal. That way, your gross rent would become your income to get a bigger loan

I think this is legitimate and a qualified borrower would be able to get a stated income loan, but probably not a total liar’s loan

Citadel Servicing Corp. (CSC) has announced a new one-month bank statement program. The new program will let a self-employed borrower qualify for a mortgage based on just one month’s bank statement.

“This is probably the most innovative way to put a borrower in a home if they’re self-employed and take full advantage of the US tax code, and they show they’re responsible with paying their bills,” said Will Fisher, CSC’s senior vice president of national sales and marketing. “If you’re a solid, self-employed borrower with good credit – you pay your bills on time, but maybe you don’t fit into traditional income qualification rules – then this qualification type is designed for you.”

The new product, however, isn’t for everyone. The one-month bank statement program is geared toward borrowers with a consistent history of financial responsibility.

“This is geared toward borrowers with very good credit,” Fisher said. “The minimum score is 700, and additionally there can be no credit events in the last five years – no charge-offs, collections, or tax liens. On the bank statement, there can be no NSF fees.”

The program is geared toward the purchase or refinance of an owner-occupied home. It’s not limited for cash-in-hand for a refinance, to a maximum loan amount of $3 million. Maximum loan-to-value for the program is 70% for purchase loans and 65% for refinances.

So, we should use the month we get a big bonus or have RSU vesting to inflate out income? That’s insane. I guess they are ok taking the risk, since they require 30% down.

As long as it’s not widespread and it’s kept on the books of the bank, stated income is fine. Banks are not stupid and they will be careful if the mortgage is not resold and not securitized

But the problem is that as mortgages are easier to get now, price has gone up. If everyone can buy, you lose an advantage in purchasing. For investors, it’s becoming a better time to sell, not buy. You want to buy when others can’t get a mortgage to buy