![]()

Potential to climb by 700% ![]()

Chart looks bullish.

Disclosure: Don’t intend to increase holdings. Prefer to ride with 1000 shares.

![]()

Potential to climb by 700% ![]()

Chart looks bullish.

Disclosure: Don’t intend to increase holdings. Prefer to ride with 1000 shares.

Elon Musk is one step closer to the $1T pay package

https://www.cnn.com/2025/11/06/business/musk-trillion-dollar-pay-package-vote

Musk got his $1trillion promised. Meanwhile here’s a treat for those Tesla owners that find themselves homeless…. ![]()

Merry Christmas!

Looks like this forum is kind of dead… oh well.

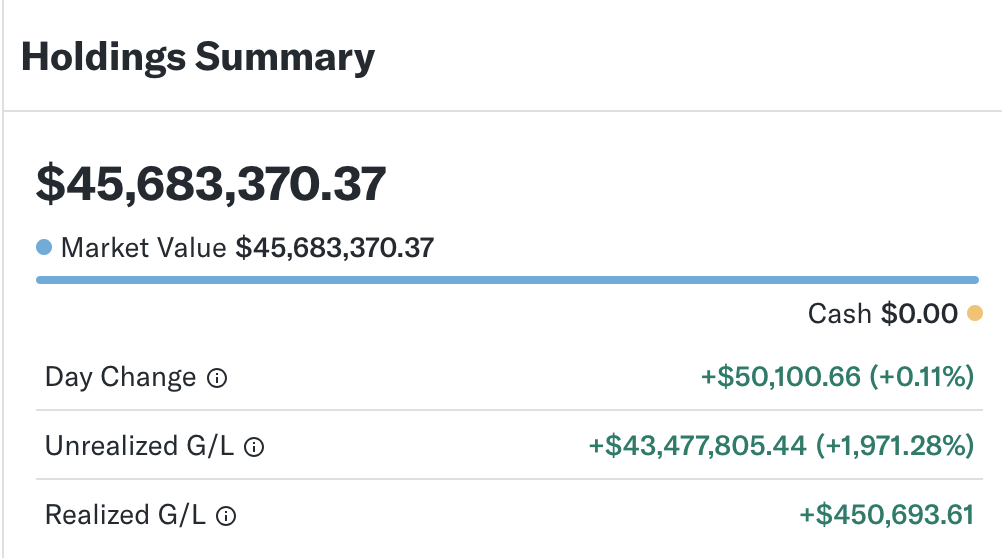

My portfolio is thriving though. Look at it now… ![]()

Merry Christmas.

I’m only at 11 million and I don’t even take that number seriously. Valuations just aren’t realistic.

I did an accounting for the year and I spent less than half of my after-tax dividend and interest (mostly dividend) income. That makes me feel better than the 11 million number.

Of course there’s depreciation to account for but even with that I’m still doing well. My biggest depreciating asset is my body ![]() No expenses in the past year other than premiums but that will change. When I hit Medicare age - with no maximum out of pocket - gotta factor that in just like roof and vehicle replacement only it’s a bigger number.

No expenses in the past year other than premiums but that will change. When I hit Medicare age - with no maximum out of pocket - gotta factor that in just like roof and vehicle replacement only it’s a bigger number.

Are you overweight? You might want to consider a ketogenic diet.

Don’t be a miser to yourself. Spend extravagantly ![]()

I maintain a healthy body weight eating mostly protein and veggies with some fruit. Few carbs. I spent Christmas with relatives in Boulder and they fed me lots of carbs. Made me feel tired. But after 60 your body will depreciate no matter how hard you try to avoid it. Some people just depreciate faster than others.

Second bit of advice is good. Been trying to find a more refined alternative to my Subaru Crosstrek Sport which goes anywhere with nearly 500 miles of range. All the pricey alternatives are just bigger and have more techo-bobbles. They don’t handle as well and have shorter ranges. Only contender is Porsche Cayenne. Trouble is you need a Porsche mechanic to service one and I’m about 100 miles from the nearest one. So I’m still looking for ways to dispose of disposable net worth.

Bigger house? No - you still have to clean and maintain it and I have all the space I need.

Land? Yeah. Talked to an agent about a parcel early this year. Couldn’t get to the asking price of 290k but said I’d offer more that the 210k the owner paid for it. Was told “don’t bother; they’re firm on the price.” Never got a call back. Less than two months later the property sold for 185k. Something crooked? A kickback? Don’t know. But I still search in vain to find something to drop some coin on. A $900 Finnish M28 modified for use by ski troopers and used in the Winter War with Russia (1939-1940) was the best I could do this year.

YouTube used to pitch me mail order wives from Ukraine. When that didn’t work they went with Southeast Asia mail order wives but now they’ve given up entirely.

Critical age when physical health starts to deteriorate rapidly are: 55, 75 and 85. So once you’re passed 55, taking care of health is more important than anything. Btw, peak physical health is 45 even though it takes till 55 for health to decline rapidly.

Taking care of health is as easy as ABC, eat less move more. You can eat any food and drink any beverages, the thing to remember is portion control. That is, don’t torture yourself with diet and don’t over-eat. The best form of exercise is walk and tai-chi. One last thing, get enough sleep.

Those are ex-prostitutes. Better to get one through your favorite hobby community.

Most people don’t need more than $10M. If you’re not staying in expensive cities, $3M is more than enough.

.

RE market is quite dead too. Hard for upgraders to upgrade because mortgage rate is higher than their current mortgage rate. Hard for newly weds to buy because house prices are still high (despite significant price drop after Covid) relative to their pay.

Nowadays, I hardly look at the RE market since I have gifted all my rentals to my children.

Movement is easy when you live rural. Gave up on the wife thing and adopted a wonderful dog. Retriever and Carolina dog mix. Great hiker but also fine with dead days alone at home every once in a while.

There are of course trade-offs. I cannot make a cell call until Jan 2. System is designed for maybe 10,000 users. There are likely over 100,000 vacationers now trying to use it for calls and streaming it so it’s useless for all intents and purposes. Calls start dropping after the first 5 seconds.

Yeah, 3 mil would likely be enough for me but with P/E’s where they are now and SPY yielding just 1.07% I “feel” like I’m worth maybe 5 mil. The 11 mil figure feels like a weird contrivance which will eventually evaporate. No different than silver now at $80 an ounce.

Anywho, here’s Bucky dog.

.

Sell $1M worth of SPY now, you would have more than 10 years worth of expenses.

Afraid to time the market. My SPY positions are so old that I’d immediately lose over 100k to taxes and then have less than 900k left in ever-depreciating cash. Then I’d have to successfully time back in close to a bottom.

Got $10M worth of SPY to compound and 10+ (~18) years expenses secured is not a good thing?

It’s all good. I just don’t put much stock in today’s valuations.

.

Don’t quite understand this comment. The key of my suggestion is to have the cake and eat it too. Sleep well from 10+ years expenses secured yet didn’t lose the growth potential.

Historically worse case scenario for S&P is a lost decade ie no change in price, normal CAGR of 7-11% ($10M to $20M-$30M) and best if printing money continues is 18% ($52M).

That is you don’t give a damn to current and the next 10+ years’ valuation and yield.

Lastly, don’t let income tax affects your decision. Trying to minimize income tax is never a wise decision. At your age, health is most important, minimize stress, trade $ for time, should be doing what you love to do and not tie up time in activities you dislike.

OK, I better understand your initial comment.

Normally I don’t let taxes drive investment decisions. But losing wealth to taxes every time one tries to time the market adds up. Timing must be impeccable.