I happened to see a good thread on Roth IRA ($5500). Not all people eligible for Roth, but whoever eligible this is best way of saving for retirement as Roth IRA grows tax free forever.

1 Like

Wow, that’s amazing for people that are above the income limit to be able to deduct IRA contributions. I haven’t done a IRA In years, since it’s not deductible. I could do it then backdoor it to a Roth. I wouldn’t have to pay income taxes, since I couldn’t deduct the contribution.

Yes Jil, a good idea, but knowing what I know, I would suggest a better vehicle when it comes to check many different factors. I brought an illustration not long ago to show the benefits of IUL. You pay a life insurance benefit, and then you put as much money as the IRS can allow but you only pay fees on the premiums for the life insurance, not the extra $ amount. Probably, you will get a 7.5% return according to the latest results given to me last days.

IULs loans and death benefits are tax free.

These are some of the facts on Roth IRA and IULs:

1- Limitations on contributions. $5,500 on IR, unlimited on IULs.

2- Market risks. The market crashes, so it’s the 100% of your money. IUL never risks your money.

3- Management fees even when you pass the 59 1/2 age and don’t cash it out.

4- No liquidity. IULs allow you to loan 75%–80% of your premiums.

5- Age restrictions for cashing out. Most of your money is captured until you can retire. IUL from first 30 days.

6- Roth IRA, you pay management fees for the whole amount. IUL cost of insurance.

7- No living benefits. You kick the can, they bury you in a hole. IUL you get lots of $ so your family can survive your departure. That’s all.

Since this is a market where everybody pushes their own agenda, you need to make your own research.

I have read this guy’s book the power of zero.

ROTH IRA OR IUL?

By DAVID MCNIGHT

Ever take an IUL application on Friday afternoon only to get a voice message from your prospect on Monday morning saying he’s had a change of heart? Over the weekend he researched what the online “gurus” had to say about IUL and, based on his findings, he’s not too eager to proceed.

If you’re in the IUL market and this has never happened to you, well, just give it a little time. The truth is 90 percent of your clients are doing online research on you and your recommendations between appointments. And when they research IUL online, they all walk away with the same conclusion: IULs have high fees. Because of those onerous fees, they contend, they’re much better off steering their retirement dollars towards a low-fee, tax-free alternative like the Roth 401(k).

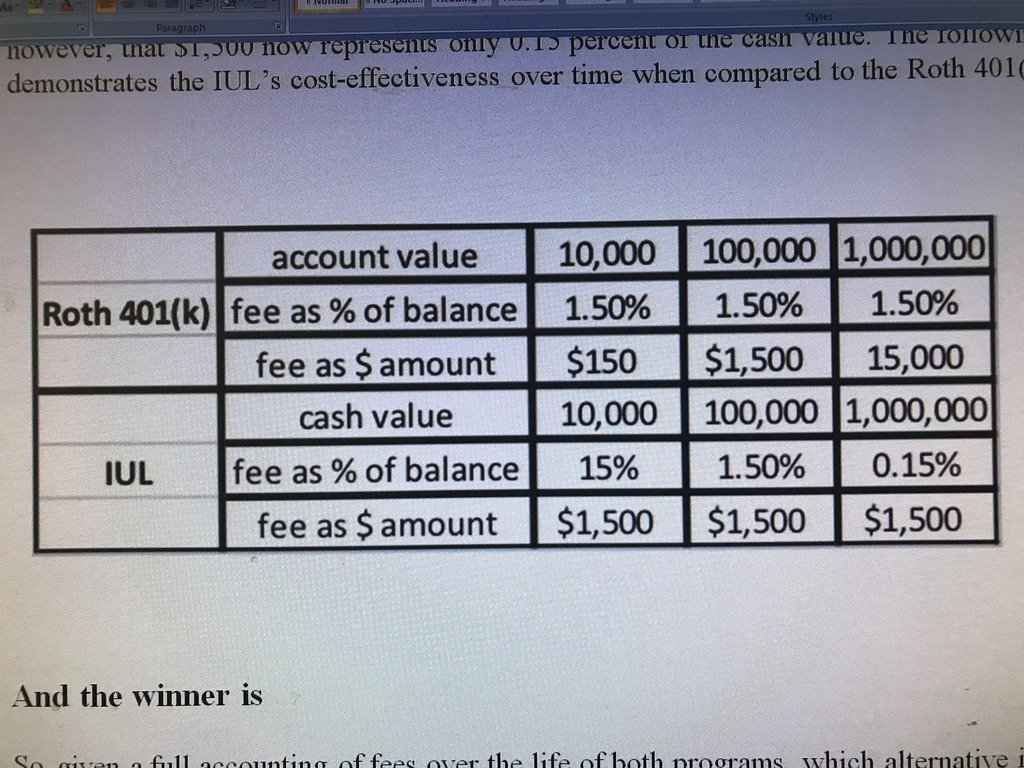

The Roth 401(k) vs the IUL

This of course begs the question: Is the Roth 401(k) really less expensive than IUL? Comparing an IUL’s fees to traditional tax-free investment accounts can be a tricky proposition, especially if you fixate on first-year expenses alone.

Let me illustrate with an example. According to USA Today, the average expense ratio of a Roth 401(k) account is about 1.5 percent per year. So, if you make a contribution of $10,000 to your Roth 401(k), your first year expenses will be $150. Conversely, if you contribute $10,000 to a properly structured IUL, **your first year expenses might be closer to $1,500. **

Based on this comparison alone, the Roth 401(k) seems the obvious winner. But comparing first year account balances hardly tells the whole story. Here’s why: The fees inside the Roth 401(k) are low when taken as a percentage of the first year’s balance (in our example, 1.5 percent per year), but when measured in actual dollars, the story changes dramatically over time. For example, if that $10,000 Roth 401(k) grew to $100,000, the annual fees would jump from $150 to $1,500. If it then grew to $1,000,000, the annual fees would balloon to $15,000. In other words, the more money you accumulate in a Roth 401(k), the more fees you pay.

Contrast that with the ongoing fees of a properly structured IUL. Generally speaking, when an IUL is structured to maximize the cash accumulation within the growth account, the fees stay relatively level. This is accomplished by buying as little life insurance as the IRS requires while stuffing as much money into it as the IRS allows. Under death benefit option 1 or A, the amount of insurance you have to buy under IRS guidelines actually decreases as your cash value accumulates. Even though the internal cost of insurance is rising, you’re actually buying less of it as time wears on. This keeps the IUL’s fees relatively stable over the life of the program.

Even though the fees in the IUL are stable, they grow smaller over time when seen as a percentage of the overall cash value. For example, when an IUL account value grows from $10,000 to $100,000, that same $1,500 fee now represents only 1.5 percent of the total account value — the same as the Roth 401(k). When the cash value of the IUL reaches $1,000,000, however, that $1,500 now represents only 0.15 percent of the cash value. The following chart demonstrates the IUL’s cost-effectiveness over time when compared to the Roth 401(k):

And the winner is

So, given a full accounting of fees over the life of both programs, which alternative is the least expensive? By looking at the trajectory of fees in either scenario, it appears that, given enough time, the IUL eventually wins out.

But how can we be certain? A surefire way to determine the least expensive alternative is to perform a side-by-side comparison where you contribute equal amounts of money to both programs over a fixed time period (say 10 years). Next, distribute tax-free dollars from both programs for another fixed time period (say 25 years) starting in year 11. Be sure to apply the 1.5 percent expense ratio to the Roth 401(k) while letting the life insurance illustration system account for the internal expenses of the IUL.

In most cases, you’ll find the IUL can distribute tax-free dollars just as productively as the Roth 401(k). Equal distributions, by definition, mean equal fees. In fact, when you run the internal rate of return (IRR) on a properly structured IUL, you’ll find that its annual expenses, averaged out over the life of the program, are around 1.5 percent.

The moral of the story: Whether you put your money into a Roth 401(k) or an IUL, someone is going to be making 1.5 percent. The real question is, what are you getting in exchange for that 1.5 percent? In the case of the Roth 401(k), you’re getting money management, third party administration and advisor fees. By the way, you pay those fees rain or shine, even in a down market. In the case of the IUL, you are paying 1.5 percent of your account value on average over the life of the program, but you’re getting something very useful and impactful in exchange for it.

Upside market potential with downside protection

For starters, the IUL allows you to participate in the upward movement of a stock market index while guaranteeing against market loss. To illustrate how powerful this is, I ask my clients the following question: “If you lost 50 percent in your Roth 401(k) this year, what would you have to accumulate next year, just to break even?” Nine times out of ten, they say 50 percent. The truth is they’d have to get 100 percent just to get back to square one. For those who lost 50 percent in 2008, it took them an astounding six years just to claw their way back to even. The guarantees in the IUL can safeguard your clients against market loss at a period in their life when they can least afford to take the hit: at retirement. Many IULs have back tested rates of return of nearly 8 percent. After netting out the 1.5 percent average fee, that’s a 6.5 percent rate of return. If your clients can get a 6.5 percent rate of return without taking any more risk than they’re accustomed to taking in their savings account, that can be a very safe and productive way to grow their money.

A life insurance death benefit

That 1.5 percent average annual expense in an IUL also goes towards the cost of life insurance. Many of our clients have already budgeted for the cost of term insurance. Instead of sending that term insurance premium off to an insurance company in the form of a premium payment, why not recapture it, divert it towards their IUL bucket, then let a portion of it drip out in the form of expenses? In other words, when our clients pay for the cost of term insurance, they’re paying for much of the cost of an IUL, they’re just not taking advantage of the unlimited bucket of tax-free savings the IUL affords them. The tax-free life insurance component of the IUL is one of the great benefits that 1.5 percent fee provides.

Doing double duty: life insurance as long-term care

There’s one final benefit that clients get in exchange for that 1.5 percent cost: long-term care. Most IUL companies these days allow the tax-free death benefit to double as long-term care insurance at no additional charge. The stipulation is this: If somewhere down the road you can no longer perform two of six activities of daily living, and can find a doctor to write a letter to that effect, they will give you your death benefit while you’re alive, for the purpose of paying for long-term care. Contrast this with traditional long-term care insurance where you could pay for 20 years, die peacefully in your sleep never having needed it, and then never get your money back. With IUL, you do pay the cost of insurance, but if you die never having needed long-term care, your heirs still receive a death benefit. So, there isn’t the heartburn associated with paying for something you hope you never have to use.

When we fail to put the IUL’s fees in the proper long-term context at the outset of the sales process, our clients often turn to the one source over which we have very little control: the Internet. And when the take their cues from the Internet, the IUL invariably gets painted as a clunky, onerous, fee-laden means of saving for retirement. The best way to neutralize the online naysayers is to illustrate how the IUL’s fees compare to those of a Roth 401(k) when considered over the arc of one’s retirement. Once you’ve demonstrated the IUL’s cost effectiveness over time, you can spend the rest of your time explaining how its many compelling attributes make it a dynamic addition to a balanced, thoughtful approach to tax-free retirement planning.

Of course, this venue is for positive thinkers, not for negative people, not for those who never check their balances or don’t even know how much they put in and how much they should have by now, or those who are so sick that they can’t/won’t qualify for life insurance.

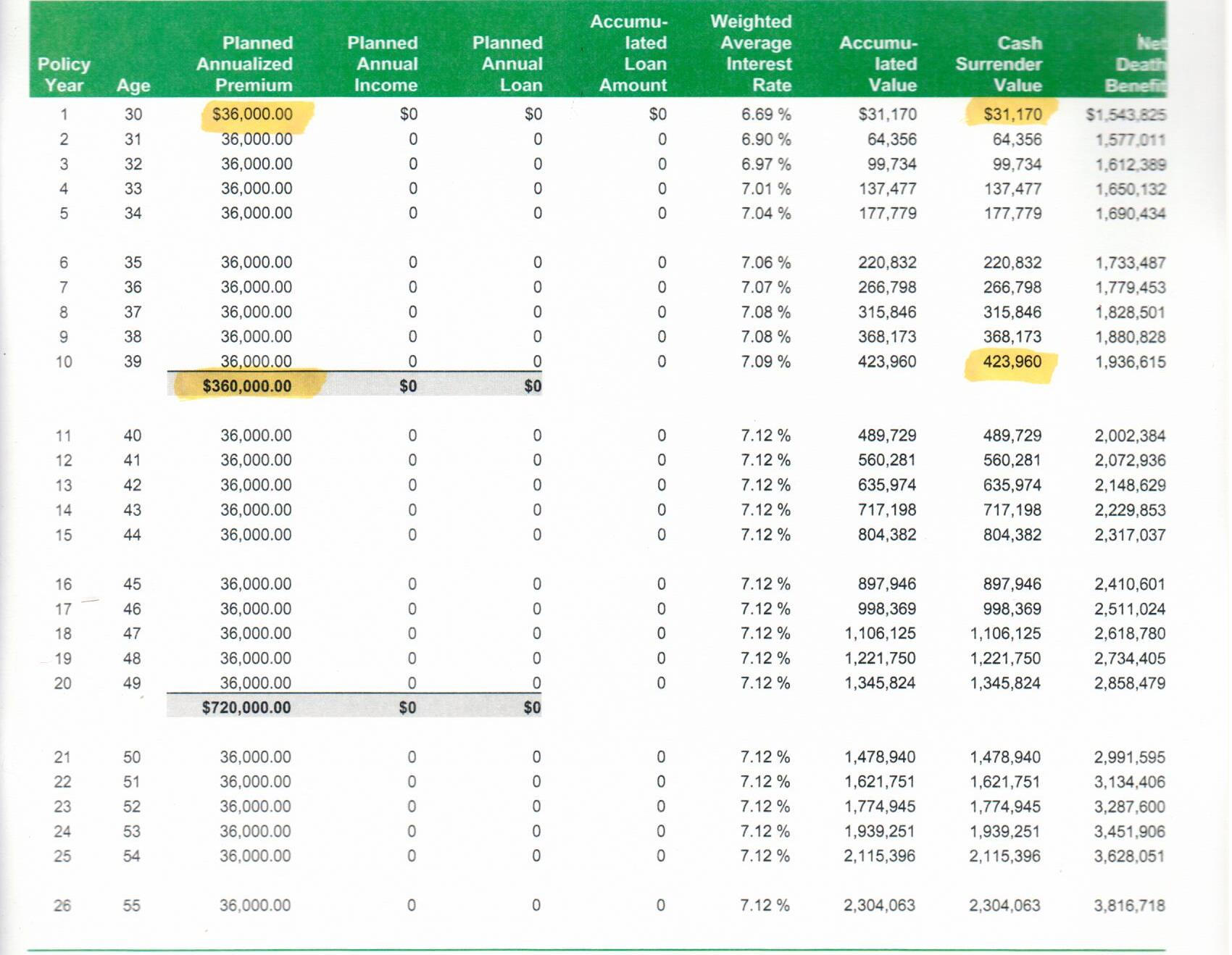

Here it is, an illustration of a person being 30 years of age, showing cost of insurance (COI) of $6,623.52 a year out of $36K premiums a year for 30 years. Then stop contributing at age 60. That is about the same as putting $5,500 annually on a Roth IRA.

Note that by paying $551.xx a month, you can get an advantage by increasing the premium to $3K a month. You loan close to 75% out but you still have $3K earning compound interests. Plus you get 4 living benefits in case anything happens to you.

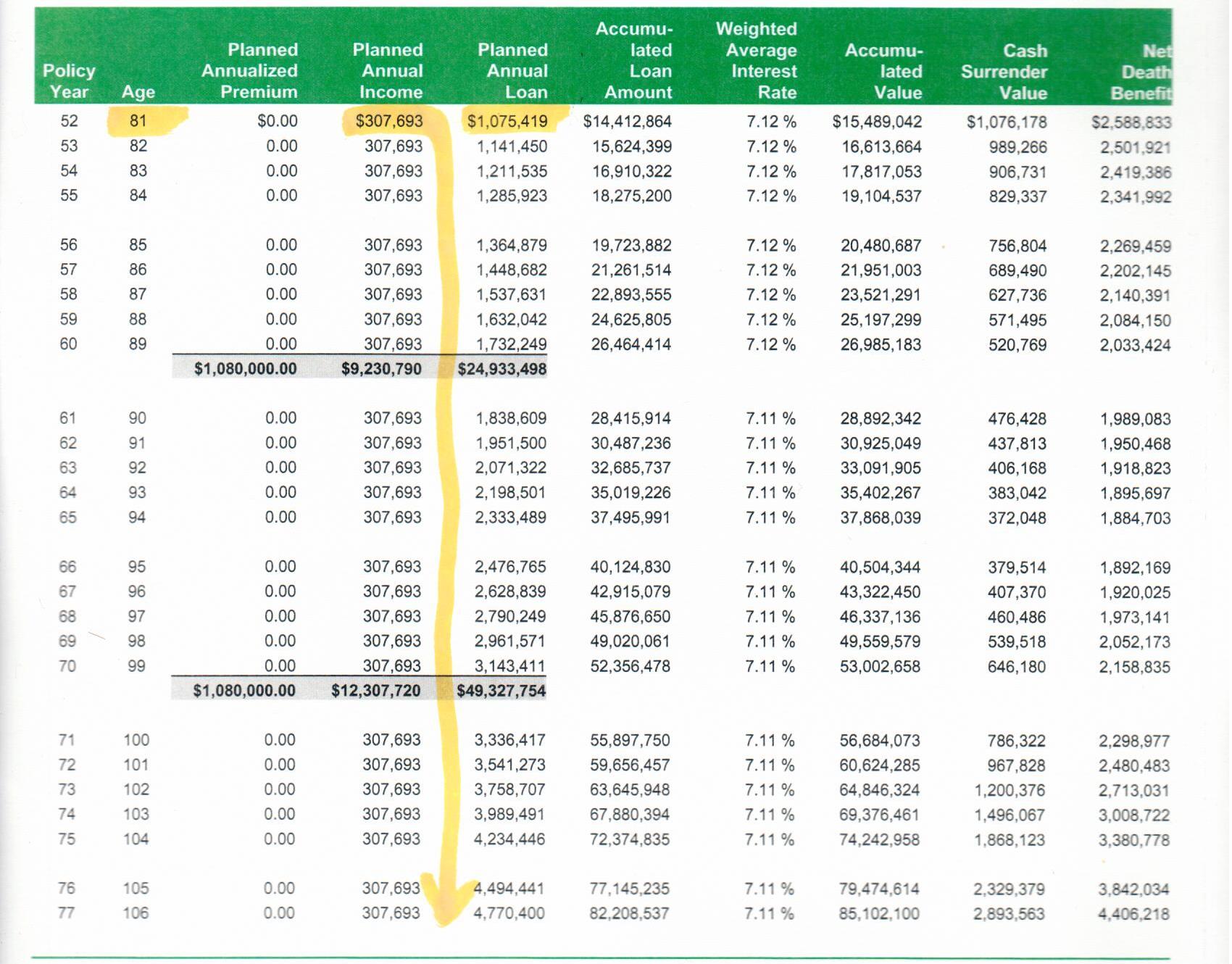

The illustration runs at 7% return. Can get 12.5% or less. The market dictates if you get that or 0% but your money is not invested at all so you never lose it, you only lose what is the cost of insurance. I could tweak it a little bit, but no time, just a general idea of what it could be $307.693 a year, tax free, from age 60 to 120 Death benefit of $1,512,656, which will increase and from where the beneficiaries will pay the interests of the loan. Basically, they will receive the initial death benefit aforementioned. Who cares, we all are going to die.

Not bad for close to $200K you paid for cost of insurance in 30 years, right?

Check the column of accumulated value, year 10 shows more money than what the total amount of your premiums are.

Unless IUL providers either constantly beat the performance of an index fund, or dole out their own money to the insurees, I don’t see how IUL can provide more appreciation than a Vanguard index fund at 0.05% fees. I don’t have to understand all the intentionally complex footnotes or details of IUL. The basic math doesn’t work out the way IUL makes us to believe.

1 Like

If you have after tax contribution too, you can make it backdoor Roth using the principal amount without paying tax(as this after tax money). I contributed some after tax money too.

1 Like

After-tax is the only way I make my contributions. I carry a regular IRA with 0 balance. I first fund it with my after-tax contribution every year Jan 1st week. Then a week later move everything to the Roth.

Also there is something called Megabackdoor Roth which allows you to contribute upto 35000$ per year. Only a few large companies offer this - Google, Ford, etc.

Do no evil.

There are many benefits I can count.

-

After tax, principle, can be withdrawn after 5 years in case of emergency or any other reasons (company plan allows). This can be used as down payment.

-

For mortgage 6 months cash reserve, lender considers 60% of traditional IRAs or 100% of After tax (if we can produce evidence). You do not need to maintain separate 6 month cash reserve. This became handy many times when I tried financing and refinancing

-

You can borrow 50k (if company allows) from 401k/IRA towards down payment. This will not affect any DTI- for sure. But lender almost count 100k (double of 50k) from your cash reserve portion.

You know how Warren Buffet made billions? He has invested GEICO insurance premium money in companies and stock accounts and got wealthy !

"Rightfully so, much is made of Buffett’s use (more precisely Berkshire Hathaway’s use) of “float”, and Buffett loves to point out its advantages (mentioned 46 times in the 2015 Annual Report[1]and 32 times in the 2015 Letter to Shareholders[2]).

Buffett’s Berkshire Hathaway is unique in that it is a huge multi-national Holding Company that wholly owns[3]many insurance companies.[4]Those companies include Berkshire Hathaway Reinsurance, General Re, National Indemnity, Applied Underwriters and of course GEICO.

The profitable growth of these Insurance Operations over a LONG TIME is what sets Berkshire Hathaway apart"

1 Like

That’s an excellent angle to look at this. Anyone who can constantly beat index funds won’t be in insurance business, he/she can start his own funds and earn a lot more.

1 Like

@buyinghouse Your table doesn’t even match what you’re explaining. You can see the loaned value is zero until age 60. The person would have paid over $1M in premiums. The $307K/yr income after 60 is interest on the cash surrender value plus what they remove from cash surrender value each year less some fees.

At 60, cash surrender is $3,120,709. 7.13% of that is $225,506. The cash surrender decreases to $3,033,236. That’s a loss of $87,473 in cash value. That plus the $225k interest is $312,919. So fees are eating ~$5k.

The “loan” they give you is really just the interest on the money you’ve invested plus some of your principal.

Someone completely screwed up the planned annual loan and accumulated loan amount columns. In year 70, the person is “borrowing” $558k, but they only get $307k in income? The accumulated value column is BS too.

I hope I don’t sound like a dummy to let you know that IULs are indexed universal life policies. I bet you know it, just trying to make things clear.

Since you are talking about indexing against indexing, I can’t speak evil of any Vanguard account or policy because I am not familiar with that type of market, I believe for that I need a special -any- series life insurance license. I don’t need it at all.

It’s hard to ping point which type of account or policy you have or how good returns you would get if you invested the aforementioned $561 a month and compare it to the illustrated policy above, none the less the $3K. I browsed their website and all I could see is that they mention mutual funds a lot. As I said, I need a series license to have worked or known one.

Since IULs are first of all an insurance against unpredictable life situations, I can’t tell you to use it as an investment tool, I just point at the real fact that numbers don’t lie since insurance companies project their returns, some guaranteed it at 4% tax free, then you can decide if you want to get a risky one, a no indexed one where you win or lose everything.

You won’t get a penny from your Vanguard account if you get sick. Nor your family will get a death benefit. Correct me if wrong.

I just thought at the end of the day, IULs are in a business to make a profit. So what ever premium they collect, plus investment profit they make, should exceed the payout they give out to their clients. Maybe I was plain wrong. They are charities after all.

1 Like

Thanks for touching something some people, ignorant on the matter, can’t comprehend.

Behind any insurance company in CA, there are 4-5 other insurance companies acting as re-insurers. If an IC is going down, they will take over, otherwise, the state takes over. And so far, no insurance company has been down, try to find out of one and you will be amazed to see none so far.

States like CA, requires them to have not sure how much, but $1.05 for every $1 insured. The one I showed illustration from, has a $100B in their disposition. Plenty of money to spread around.

Why is Warren Buffet investing in ICs? Because he knows insurance companies are well respected, some are almost 200 years in the business and they have so much $ to cover their projected expenses paying the premiums.

AIG almost went down during the last recession, but not because their life insurance division. They paid out their obligations because I said, the states had them with $ put aside to cover any failure.

Thanks for the questions.

You can see the loaned value is zero until age 60.

I am losing you here? I am going to try to explain you what I understood of your question.

What you see on the column of Planned Annual Income is the money you will be receiving as an income for the rest of your life providing the market is in good stance, and no 10-20 years of 2008 scenario happen. If that happens, I will be eating from the dumpsters.

Also, don’t forget you have used a rider that allows you to loan 75-80% of your premiums already. That rider keeps working and takes some $ out of your income when you are not paying premiums at all. There are a few riders within the policy, some paid, some free. It is what it is.

Practically, from the $1,080,000 of premiums, you used $900K more or less from the policy to pay your mortgage, house expenses, go to Las Vegas, etc. $200K have been paid or retained into the policy as a cost of insurance in 30 years.

We don’t call the premiums investment but premiums.

I can keep explaining what the columns and whatever it is, but my English is not that good. So, I am going to answer this one, perhaps that can explain you the confusion.

“Someone completely screwed up the planned annual loan and accumulated loan amount columns. In year 70, the person is “borrowing” $558k, but they only get $307k in income? The accumulated value column is BS too.”

OK. To avoid I said this, no, I said that, the illustration is done at a perfection that I can’t change anything, I just type age and the pertinent information. This is high tech thing, I can’t change what the numbers are, the state of CA is over this and nothing can change that. It is calculated to give the insured $307,693 a year. Anything more, the policy will lapse.

Also, this is a mathematical calculation, you need to leave some money in the policy to work miracles, you are not longer contributing any premiums, the accumulation is working for you, but if you can visualize it, you can keep contributing $36K a year and the income will be double or triple.

As I said, or I didn’t say it, this is a disciplined method. Not your make me rich in one year or two. For that, there it is, the stock market.

I thought this is subject to penalty charges (somewhere around 20% if I remember correctly).

Penalty is 10%, but does not apply to this case. I read somewhere that we can withdraw after 5 years, esp after tax 401k. I do not think there is a penalty. Need to check IRS for clear answer.

I too converted my 401k and IRA into a Roth-IRA, when it became available… I think in 2010… taxes had to be paid over 2 years April 2011 and April 2012.

Basically, holding the funds in a Roth-IRA is a bet that in 20 years (at draw time) I would pay a higher tax rate than now (or in 2010). This could be because the government has seen the need to increase earned income taxes for whatever reason. It could also be that my income in 20 years is higher than today.

Many people like 401ks and traditional IRAs because it postpones taxation. Their bet is that in their old age, they will be in a lower tax bracket- either because income is lower or tax rates in general will be lower.

In 2010, I decided to convert to Roth-IRA… I assumed that after Bush, we would be seeing the Democrats in power for 20 years… with increased government spending… and increased taxes. It looks like I was wrong on that part. I still think my income bracket likely will be higher in 20 years (all rentals paid off, fully depreciated). So, the ROTH may turn out the right decision.

The biggest worry is that the government can always change laws. I believe they do have the power to break the promise that (at the proper age) all ROTH withdrawals will be tax free. Looks unlikely today, I know.

1 Like