They may declare like this but may not increase further. If they increase, they will have to resolve more issues like SVB, SBNY, FRC…etc.

For banks (or for any one) the safest asset is Treasuries (as this is guaranteed by government) and many will have huge amount in LT T-Notes. More the rate hikes, the value will further go down, they may have liquidity issue and FED has to step on more.

IMO, FED does not have room for further rate hikes as they need to balance rate hike, inflation and banks Huge liquidity issue appx 620 billions unrealized loss.

Think this way, you own a bank, get people deposit money (no interest), you have staff, buildings and other overheads, you are supposed to make money to run the business and guarantee the depositors when they need money!

You can not keep everything in liquid cash as you need to run your business, but to invest in instruments and make profits.

Which one you choose (say for 200B) or how to allocate properly and Guarantee profits and depositors need?

Stocks

Gold

Loans

Real estate

Treasuries

Cash

In the world, no investment has the stable value and no guarantee!

If it were up to me I’d suggest a temporary increase of the FDIC insured limit to $10M for the next two years. This would allow the fed to follow through with their rate increases and give the banks some breathing room to work through their underwater bond portfolios.

Yes, I was referring to interest rate hikes. Inflation is decreasing. The banking system is on the verge of collapse.

It’s the position formula from physics. We have current inflation rate (position), we have the decreasing trend (velocity), and acceleration seems neutral. I wonder if they think the current velocity is too slow, so they have to hike to create acceleration? Do they think without a hike the velocity will decrease? Is the hike to create some acceleration in the current trend?

I think the intent is to put the nail in the coffin on some of these bubbles – housing, employment, compensation, crypto, etc. The trend is in the right direction but they want it to accelerate.

FDIC limit will be increased soon, but this is interesting to know why banks, big funds are forced to sell their investments during rate hike environment.

Not only FED rate hike, even market rate changes affects some one or some group during the regular days.

SVB gave good insight on such issues. Hmmm, we should have gained this knowledge at 20s !

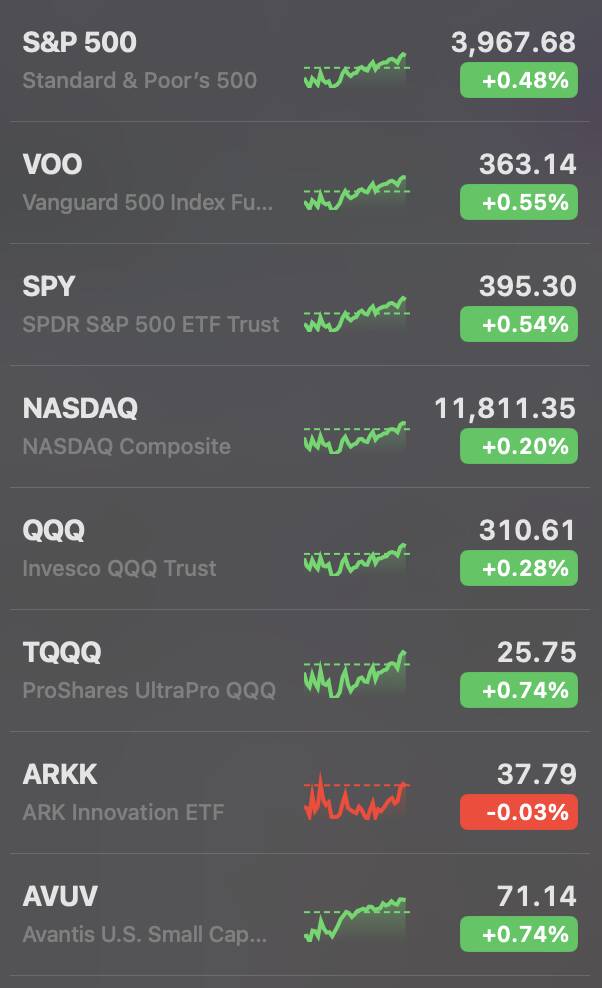

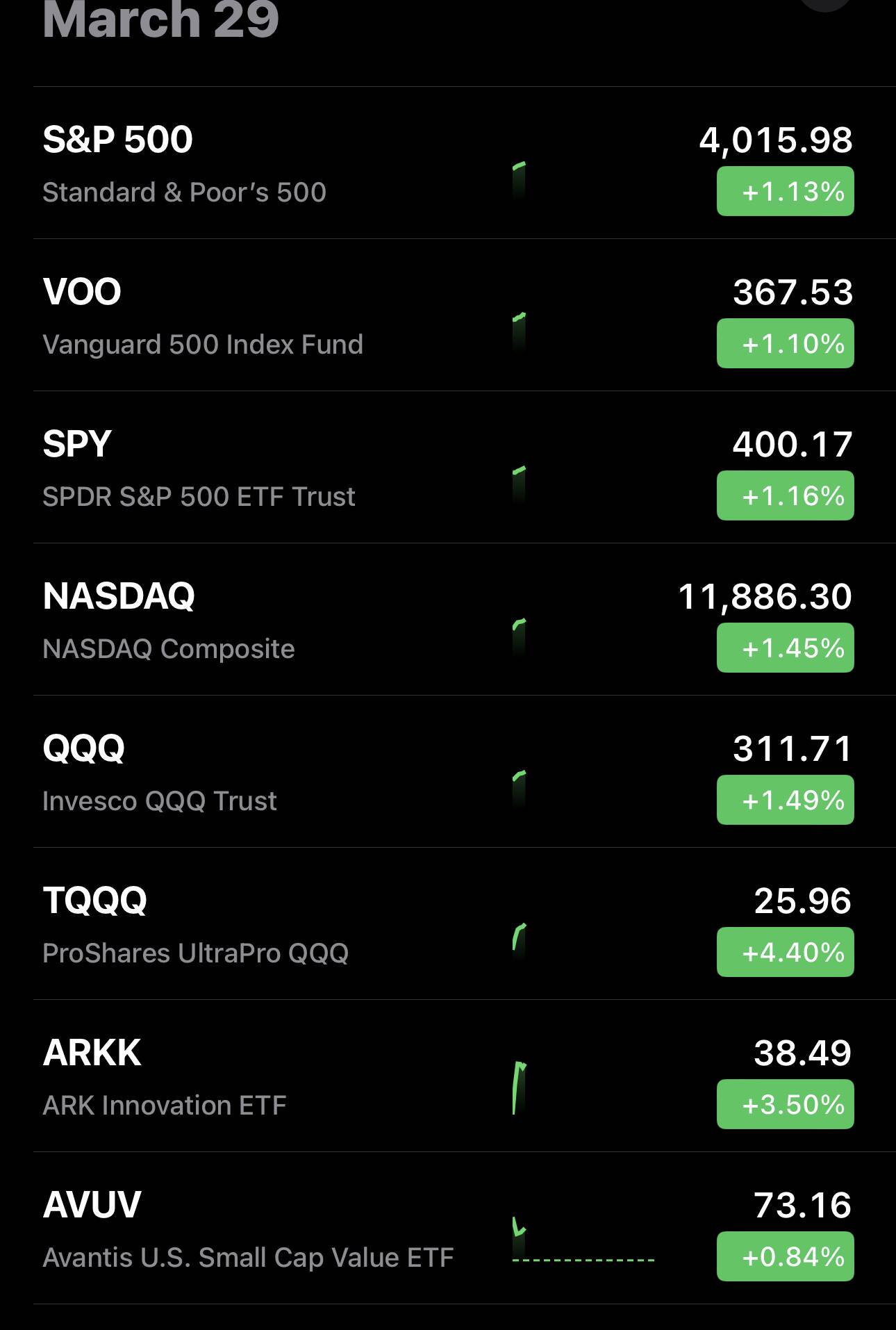

Next 3 or 4 days it is supposed to take up to SPX 4050 (nothing guaranteed, remember nothing guaranteed as future is always unpredictable, everything is guess/hope only).

True, you need have trading strategy and do not buy/dca and hold long days.

You have seen the above diagram I showed you, market may go like that wave. The only way to make money is buy at low and sell when it jumps certain percentage and wait for next low.

For example, my partner and I discussed this few days before. If TQQQ jumps over 25% from the current bottom, it is good to sell 30% of holding, when it goes above sell another 30% and further goes up sell all.

Same way, for DPST, we set 40% mark to sell 30%, then 60% to sell another 30% like that.

These percentages or formula changes then and there, depending on our review.

Now, I am trying to automate it, hands free, but too hard for me to automate such complex market conditions.

I know what you mean. My cost basis for TQQQ is 18. I could’ve sold some meaningful amount when it hit 27 in Jan. I did not.

I keep selling covered calls and cash secured puts to manage the decay.

For example, ADBE and GLD May likely crash nicely soon. More than ADBE, GLD has higher probability of dropping/correction, but do not know how much they drop and when they drop!

Since I do not go for puts or shorting, I just ignore but wait until they crash for buying opportunity.

Btw: future is always unpredictable and do not trade anything based on this comments.