One more thing, eps, revenue, unit sale, dollar sale, installed base and share price are not the same. Investing is about the future, is about the future share price. Smart phone market might have stabilized from 2015-2017, it doesn’t mean a company can’t make money selling other products or share price would stagnant at 2015’s level.

Update the title, modify content slightly, use current date, and re-publish the article from 2016-2017. Many AAPL investors sold their AAPL holdings after reading the 2016 article and missed the 7x jump in share price. Would this time be different?

iPhone and watch are bad comparison because everybody know what a handset and a watch are for. However, Vision is like early windows computers (e.g. Lisa), we don’t know what they are for.

A better (though not an ideal) analogy is Lisa (Vision Pro) vs Mac (Consumer grade Vision).

Palmer Luckey was explaining above concept (Lisa vs Mac) upon Vision Pro launch, it seems not many get it.

For reference,

Lisa first released in Jan 13, 1983.

Mac first released in Jan 24, 1984.

First killer app, pagemaker, was released in Jul, 1985. About two and a half years after Lisa was released.

…

Interview of Palmer Luckey posted here on Jun 23. Cut n paste for those who want to listen his comment.

In order to put a negative/ bearish spin on Vision Pro, the estimated unit sale was revised to be 700-800k so they can say Apple has reduced the expected unit sale to 400-450k units.400-450k is 4x Jun 23 estimate. Jfi, 100k unit was also quoted by Mark Zuckerberg during an interview. This type of reporting is why I often ignore the content of the article and focus on the intent of the article. Journalist doesn’t care about the accuracy of the content, the intent is to put a bearish spin on AAPL.

If the rumor that Apple is making a server chip is true, then NVDA won’t benefit. TSM is the one benefiting. Apple would use their own server chip for their own DCs. No need to buy any H100s or B200s from NVDA.

I believe the way Apple implements Gen AI would be similar to Spotlight and Web Search. Gen AI that operates on Apple owned data would be using their own Gen AI tools. For non-Apple data, use tools from the industry e.g. Gemini, ChatGPT, Perplexity, Baidu.

LFG!

EWT: No change in my preferred count (in yellow labels).

Btw, if my preferred count is correct, is start of a multi-year rally (wave (V)) … layman’s term is start of a secular bull run after about 2 1/2 years of correction.

Just a reminder to investors: Investing is about the future, not about the past.

Below is an update of the counts.

Generative AI is still a relatively niche product among consumers. Sure, Google and Samsung offer generative AI capabilities on their smartphones, and PC makers are increasingly leaning into so-called AI PCs, but the applications still feel largely like tech demos rather than game-changing features that will significantly drive sales. Apple has the opportunity to change that.

While tech companies are good at hyping technologies, Apple is the one who know how to employ technology well and deliver real value to consumers. Traders love hyping, investors should evaluate carefully. By investors, I mean those who have a timeframe of at least 5 years.

Btw, one of my son replaces his 6-year old intel-based MBP with a M3 Pro MBP… guess his purchase contributes to the increase in sale of Mac Incidentally, I am typing on a 2013 Intel Xeon Mac Pro. Apple products are just too well built I also has a M1 MBA.

Revenue of services increasing means installed base is still growing.

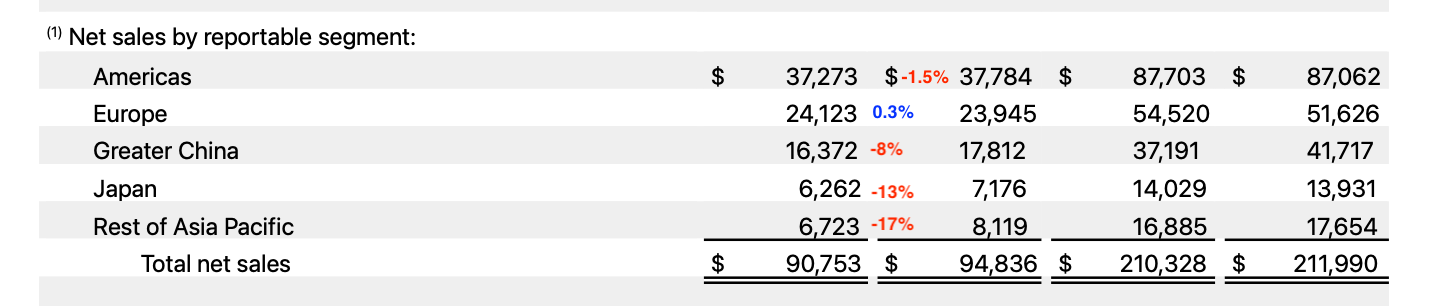

Sale reduction in greater China isn’t that bad at all… less than in Japan and rest of Asia Pacific. So much FUDs sprout by mainstream media and AAPL haters.

If a stock has been in decline for a long time, a death cross could signal a bottom soon. It is time to pay attention to the development of a bullish divergence to go long.

Look like Apple doesn’t intend to be self reliant for DCs.

Wondering Aloud: Who make more money from the other? AAPL or GOOG? Apple buys compute services from Google and Google pays Apple for default search engine.