@pandeyathotmail When a stock is near an impending correction using TA, you have pundits talk bearish about the business and its stock. The given reasons don’t matter  what matters is the timing

what matters is the timing  After the declining have started, if it didn’t meet their clients’ target, more bearish news would be thrown out. Pump n dump. Dump n pump. They would use FA or TA or both as reasons but those are just for putting a persuasive story.

After the declining have started, if it didn’t meet their clients’ target, more bearish news would be thrown out. Pump n dump. Dump n pump. They would use FA or TA or both as reasons but those are just for putting a persuasive story.

2 Likes

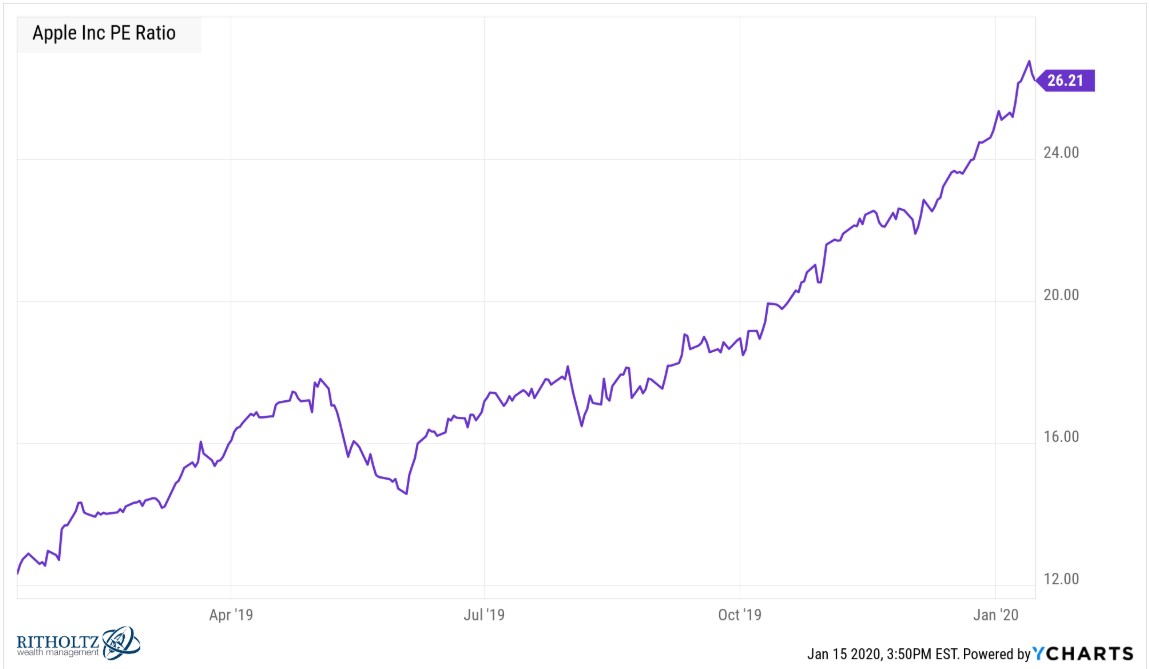

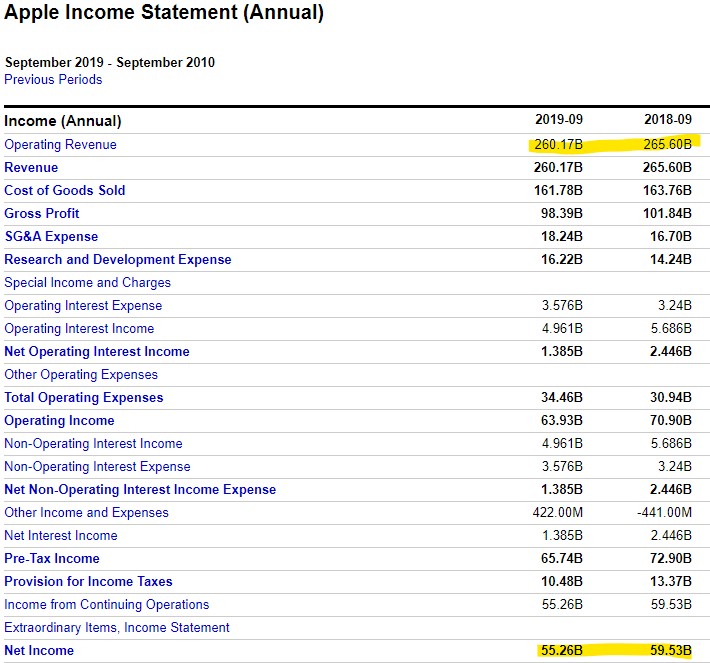

Apple’s share price gain is entirely due to multiple expansion, while revenue and net income actually fell yoy. Maybe AAPL is the modern day Enron. Who cares about old fashioned stuff like revenue and profit growth? Just financial engineer all the way.

Tesla makes no net income yet it has tripled in price in less than a year. Irrational exuberance?

1 Like

How do you so effortlessly flip flop your criteria? You’re bullish on Uber when it looses tons of money, and their revenue growth is slowing. Even if they hold their fixed costs steady, you’d struggle to map out when they’d become profitable due to their low gross margin. They can’t hold their fixed costs steady either, so good luck determining when they’ll be profitable.

I’ll let @hanera address the share count delta and how the revenue and profit per share are higher.

2 Likes

There is nothing wrong with multiple expansion. As one of the largest company in the world with slowing/no growth, a bit of financial engineering is not necessarily a bad thing if used cautiously.

Will Apple be the next IBM? Probably eventually but when? I don’t know.

From an investment viewpoint, if the multiples are too rich for you then you can sell/short it. But comparing Apple to Enron is pure hyperbole.

Let me post that question back to you. Why did you apply different criteria to Apple vs Uber? After all I am just a FOMO guy, unlike you who did careful analysis that pinned BYND market cap at 6B.

Yes I just exaggerated to highlight the lack of growth (so far) and Apple’s reliance on share buyback to buoy the stock price.

Nothing wrong with multiple expansion but it highlights how much higher investors’ expectation has gotten. It may be that Apple will show phenomenal growth in the next report and all is well. If it didn’t hit it out of the park? Could be trouble.

I will never short any stock. I am not arrogant enough to think I am 100% right. With Tesla, Shopify and Apple, I just don’t understand the bull case. For people who do understand all the power to them.

I was illustrating how WS work

Multiple expansion has been explained by Gene Munster.

You still haven’t shared your analysis for BYND market cap. It’s easy to sit back and criticize without showing anything. Sort of like it’s easy to ignore questions, then question the other person.

I actually don’t believe in predicting market cap, which is almost the same as having a price target. Notice how analysts’ price targets are almost always wrong? Maybe you think you are smarter than all the analysts out there who do this for a living.

In the case of BYND I just ask some simple questions. Is there a big secular trend going on? Does it still have a long run way? Who are the competitors? Does the company have any moat?

Like I said, simple questions that don’t require a calculator let alone detailed spreadsheet. But I am just a simple minded person.

1 Like

The problem with most of these recent IPOs is the runway is already priced in, and they haven’t even executed on it. That’s the point of the math. If they achieve a 12% market share of the US beef market and make 10% profit, then that would be a smaller market cap than the current one. That’s the total beef market too including all cuts of steak, and right now they only have a ground beef product. That’s being generous assuming they can develop and take market share across the full market.

How likely are they to do that with no additional competitors emerging? How many years is it going to take to reach that actual revenue number? You’re paying that price now and hoping then can over achieve vs those numbers. They aren’t a software company with monster gross margins and a recurring revenue model. Customers can switch anytime they grocery shop which is weekly for most people.

There’s almost no moat. They don’t grow any of their own ingredients and none of them are proprietary to them. They literally buy ingredients from farm companies and mix them together. That’s why they spend so little on R&D. Traditional food companies are already developing their own plant-based products. The space is about to get very crowded with many competitors. Those competitors already have distribution through every major grocery store.

It’s $4/lb more expensive than local, grass-fed beef. That positions it as a premium product which is a smaller market. It’s the same reason Whole Foods is much smaller than Kroger or Safeway.

[Removed my analysis]

1 Like

So you model out 20 years of discounted cash flow and are willing to pay that price now?

![]()

Talk is free. Show us your commitment. How many have you bought? @manch You too!

My position: BTO 2 vertical call spreads.

This is my last update => That was related to the analysis/model, I do not want to talk about that subject. This forum is very famous for asking lot of Q & A whenever I post such details.

See your ask which is not right. I repeated in this forum not to display . On any case, I do not like to show what I have !

Second, I am on my own and sharing whatever I know. If you or anyone feels I am talking hyperbole (without showing my positions), I am happy to stay away posting as I am not losing anything.

I am perfectly fine stop posting companies like BYND…etc.

How many shares of AAPL do you own? ![]()

iPhone revenue was up 8% yr/yr. So much for the demise predicted by some…

Congratulations. How much did you make today?