Clark is crazy good. His ability to process info and ask questions is amazing. You will not anticipate all of his questions, and they aren’t the typical dumb it down for the exec questions. I’m amazed he isn’t CEO somewhere. He’s the Amazon warehouse and delivery operations equivalent of what Tim Cook was for Apple.

What many people do not appreciate is that Amazon in not just a website, but also a very sophisticated supply chain and fulfillment system.

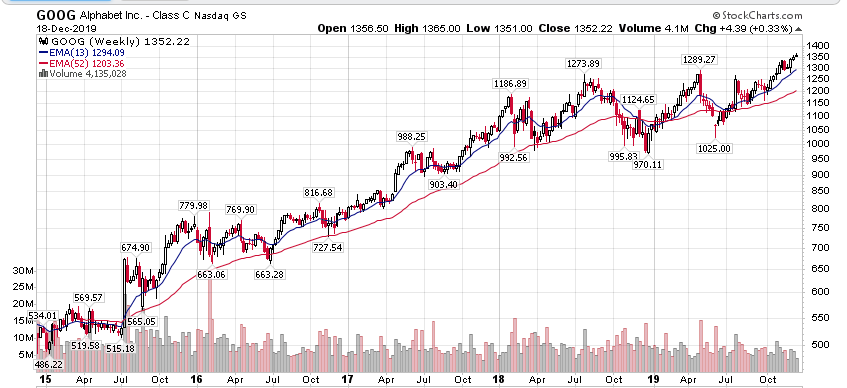

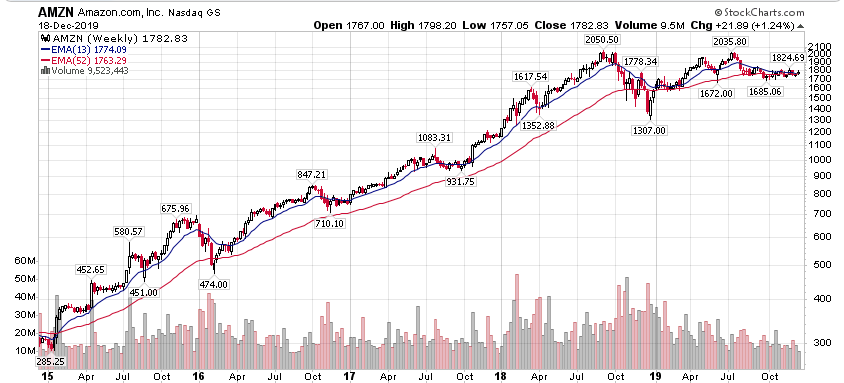

How do we explain AMZN stock behavior? What is holding the stock back?

Mid last year, FANG started to decline. GOOG has recovered yet AMZN is still going sideways.

Investors are concerned that the next-day-shipping pledge is too expensive. In October, Amazon reported its first year-over-year quarterly profit decline since early 2017 because building new delivery capacity was costing more than expected.

After Amazon covers all the big US metros with one-day shipping, it’s game over for Walmart and other big retails. No one else can come close.

It’s Bezos’ famous strategy: focus on the known. Everybody knows customers want faster delivery. Do that and you will win.

@manch Are you saying WS is short-sighted in punishing AMZN? So buy now and wait (copying @Elt1 saying)?

No worries, I won’t continue to comment assuming above is true

Amazons share of total retail is about 5% (and e-retail about 49%). Will the share become near 100% with one day delivery? Sounds like a leap of faith.

Keep commenting.

I want to know what is meant by win? How do investors like us ride on this win?

Please remember, this is a forum of RE and stock investors, is all we want to know.

According to Barron, MSFT would crush AMZN in cloud computing. @manch Sell your holdings before it is too late.

Just read an interesting article on amazon. Its share of US addressable retail market, that is excluding stuff like gasoline and cars, is only 6%. It’s even lower than Walmart’s.

I have both MSFT and AMZN. I am fine either way.

What is Jeff up to?

AWS And Azure: Racing For The Best Business Opportunity Of The 21st Century

If the cloud platforms are becoming the corporate IT platforms of the future, then they should be valued as platform and SAAS companies. AWS recorded $9 billion in revenue in the third quarter, up 35% year over year. That puts AWS on $36 billion revenue run-rate. Microsoft doesn’t disclose Azure’s revenue level but we do know that Azure revenue grew 59% in the third quarter (as an aside, I believe this lack of disclosure specific to AWS and Azure contributes to the market not understanding their evolution).

Public SAAS competitors such as Coupa (COUP), Atlassian (TEAM) and ServiceNow (NOW) all post similar growth figures to AWS and trade for between 15 and 24 times forward revenues. Assuming AWS growth decelerates to 30% over the next year, its revenue run-rate a year from now would be $46.8 billion. Applying a 20 times forward sales multiple gives a $936 billion valuation for AWS. That’s more than Amazon’s current enterprise value by itself, which of course doesn’t factor in any of Amazon’s other businesses.

Did not know this Munger quote. But it sounds very Mungerish:

Other people are trying to be smarter. All I’m trying to be is non-idiotic.

- Charlie Munger

At today’s close, market cap of AMZN is $927B hence AMZN is undervalued by $9B. Other businesses of AMZN is worthless, we all know that right? Btw, why is the author comparing the P/E of tiny companies to AMZN?

He tries to be cute and you like it. I would rather be 大智如愚.

Tiny companies are usually valued higher because they tend to grow faster. But in this case they are just growing as fast as AWS and not any faster. Therefore they should be valued lower because smaller companies’ market positions are less secure than duopolies like AWS.

Munger’s quote is actually actionable if you think about it. Yours is not.

Are you sure? How come you still behave like you’re very smart?

Sound logical but is not how psychology works. Most of us think in terms of large number theory for market cap*. So investors pay higher price for smaller companies.

Most of us think it is easier to grow a market cap from $1B to $2B than from $500B to $1T.

Jassy started by citing research that shows that 97% of the $3.7 trillion IT market is still on premises and not yet in the cloud.

Can you tell me what Jassy wants to say? AWS is targeting this entire market? The size of the cloud computing TAM is $3.7T?

Not sure whether you remember I comment on number series, displaying comparison over a long period of time is not good as it hides recent trend which could portend future trend,

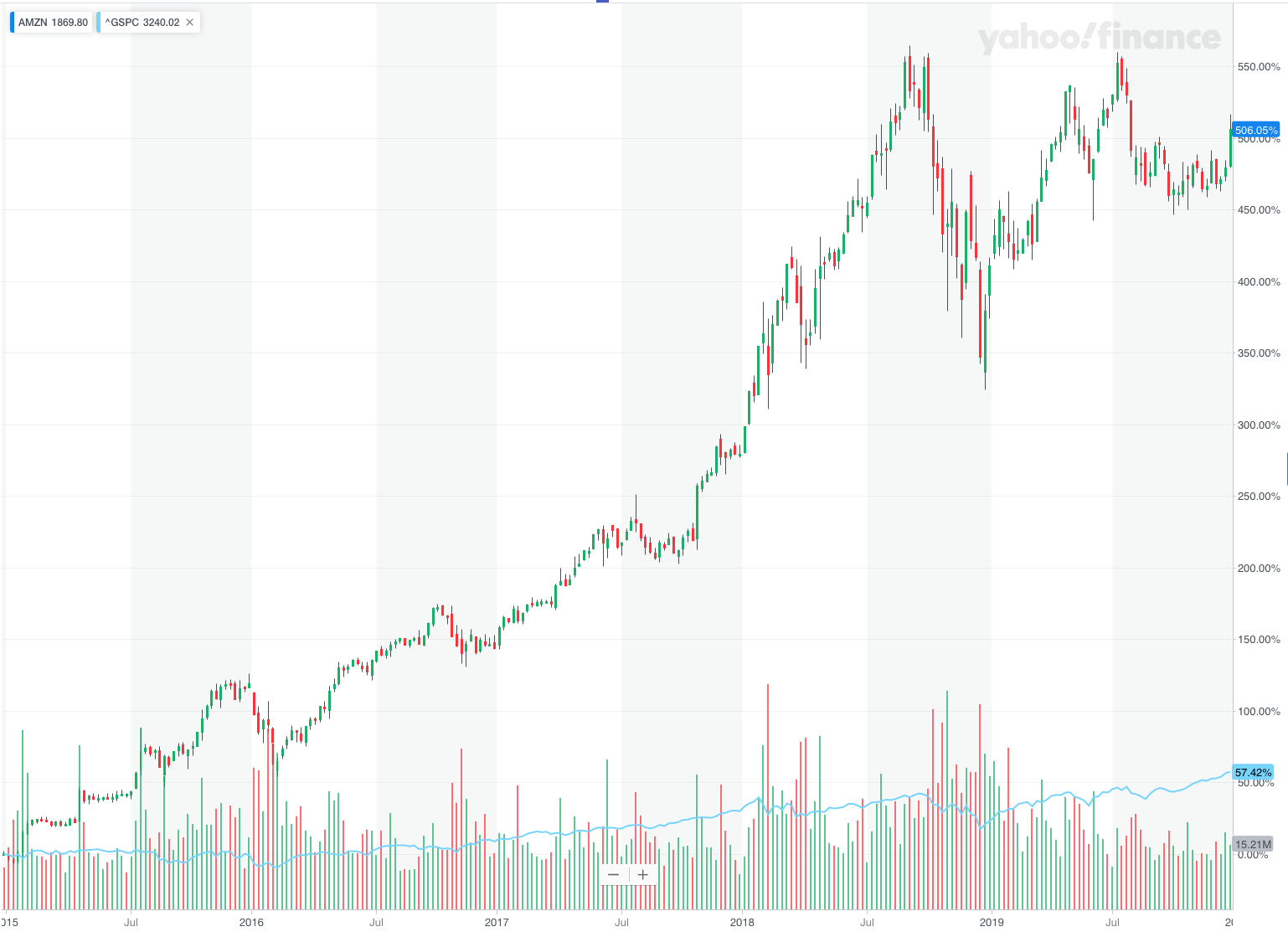

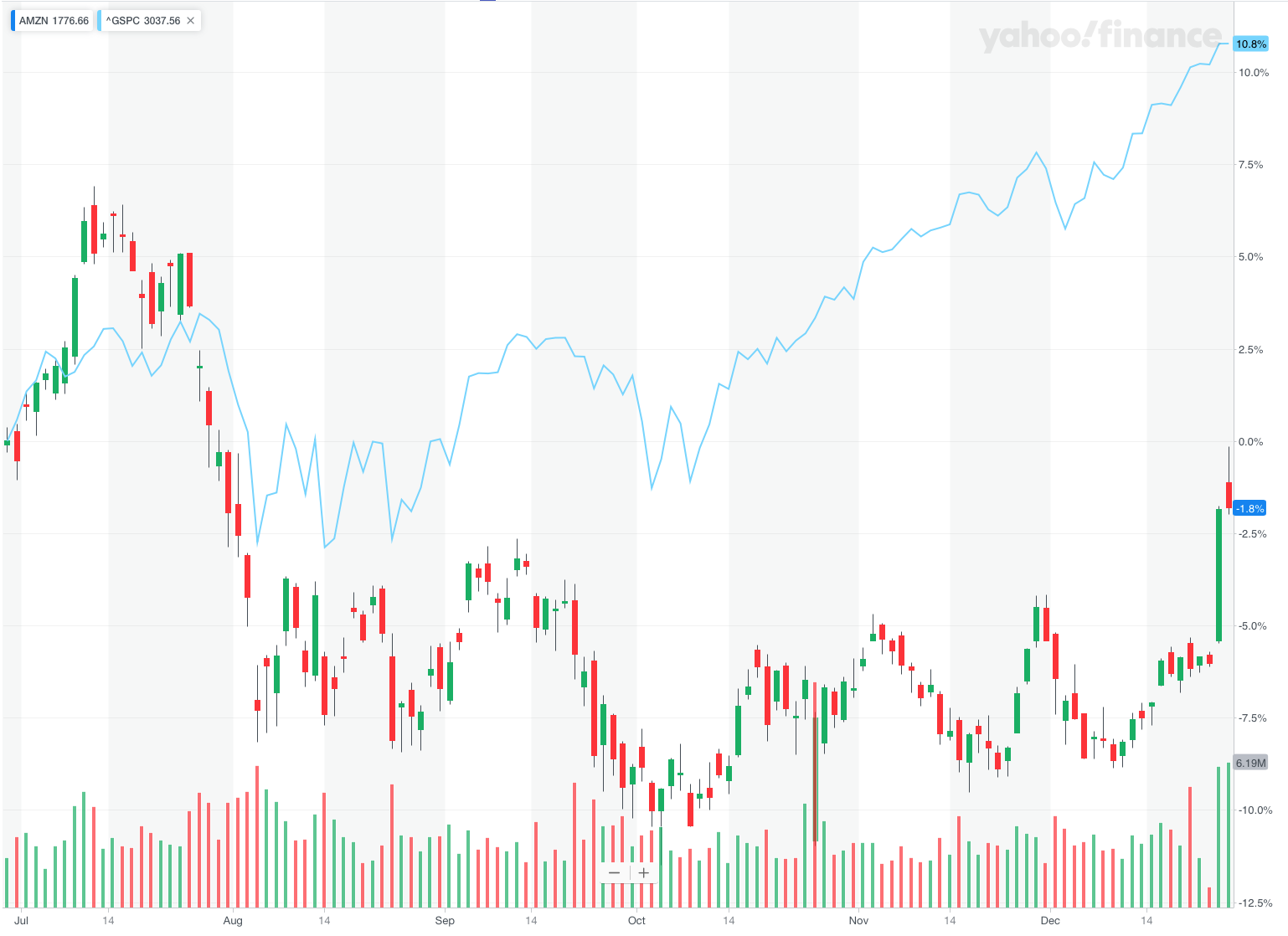

Look at 5 years timeframe, AMZN was amazing…

But its recent trend is not that great…

Investors know about AWS for a long time, so is not something new and have paid handsomely for AMZN. Why is AMZN underperforming recently? This is what we should focus on and not delve on its past success.

I remember when HP was valued as less than the printer business would be worth as a separate company.

Are you a believer in market efficiency at any and all time? Was Apple stock price a straight line upward?

All have reasons e.g. last year because of depressed iPhone due to tariff war. So what is the reason that WS gave to depress AMZN? Cost of one-day delivery is too high and can’t be recouped? We need to know the reason and then assess whether AMZN can recover from it.