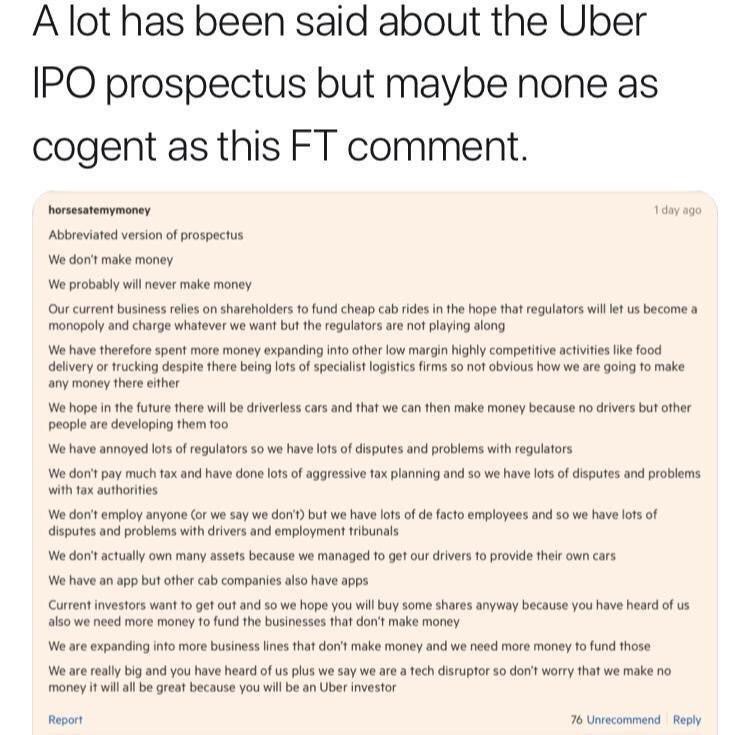

My guess: UBER is better, at good dipped price - which I do not know, for long term. I may wait for 6 to 12 months, esp to see price after the lock period 180 days over.

This is very common for 2019 IPOs. There are lot of IPOs coming, all hyped with full marketing swing by news/media…etc, but overall none worth the IPO price.

Rarely good companies come out with proper or low IPO price. That is the conflict of interest between wall street and investor.

I am just staying away from these IPOs, but will grab some when I see good dip in prices. If I buy any of these IPOs now, It is like gifting my money to those founders/promoters.

Deep dive into the unit economics of Uber vs Lyft:

Author’s conclusions if you are too lazy to read the whole thing:

- Lyft has made impressive progress at increasing the value of rides on its platform and increasing the share of transactions it gets. One would guess that, Uber, within established markets in the US has probably made similar progress.

- Despite the fact that Uber is rapidly expanding overseas into markets that face significant price constraints than in the US, it continues to generate significantly better user economics and driver economics (if Q4 2018 is any indication) than Lyft.

- Something happened at Uber at the end of 2017/start of 2018 (which looks like it coincides nicely with Dara Khosrowshahi’s assumption of CEO role) which led to better spending discipline and, as a result, better unit economics despite falling gross profits per user

- Uber’s new businesses (in particular UberEats) have had a significant impact on Uber’s share of wallet.

- Lyft will need to find more cost-effective ways of growing its business and servicing its existing users & drivers if it wishes to achieve long-term sustainability as its current spend is hard to justify relative to its user growth.

“ Long-term unit profitability is more than just how much an average user is spending, its also how much of that spend hits a company’s bottom line. Perhaps not surprisingly, because they have more expensive rides, a larger percent of Lyft bookings ends up as gross profit (revenue less direct costs to serve it, like insurance costs) — ~13% in Q4 2018 compared with ~9% for Uber.”

So much for being new age companies with a better financial model. That’s terrible. Most public companies have that much net profit. They’ll never cover operating expenses with that little gross profit. The only way to increase gross profit is increase prices (killing demand) or lower expenses. That won’t happen as long a people are driving the cars.

What happens to Lyft an Uber in a major recession. Lots more drivers and less riders. Lower revenues and more losses.

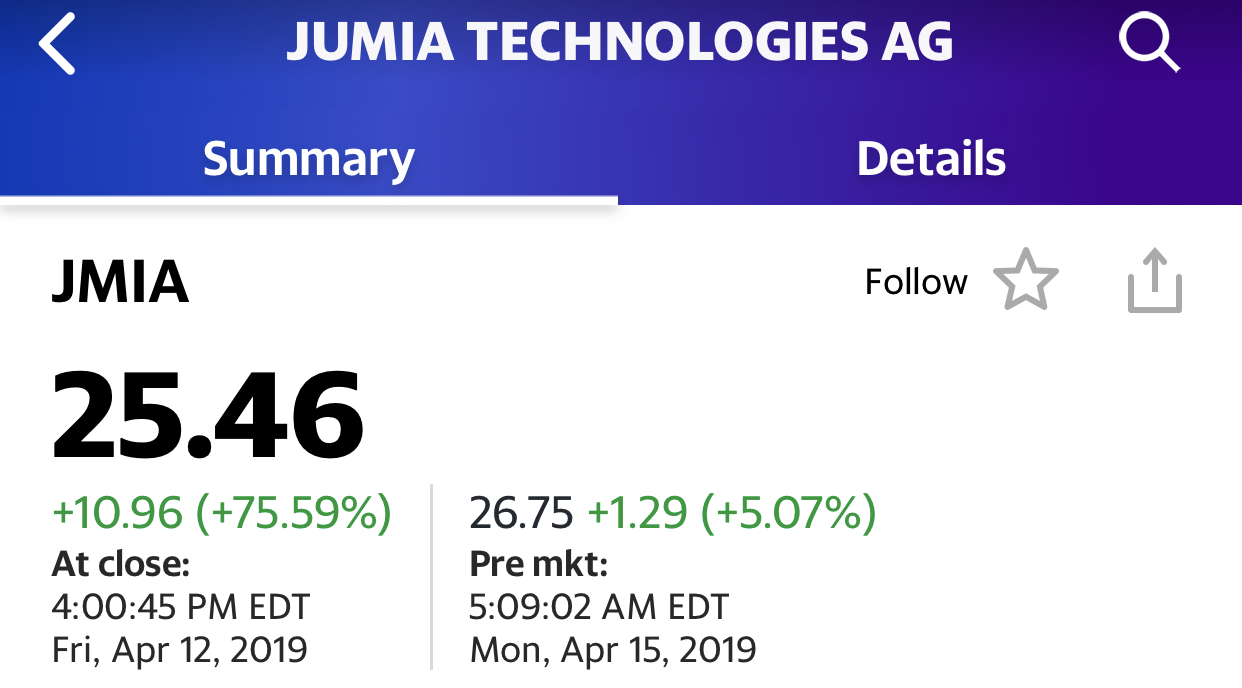

This is applicable to all loss making IPOs coming into market with hyped values. Any buyers of these IPOs are gifting them generously now.

Buy buy buy.

Wrong ! You should have said “Bought, Bought, Bought” ![]()

Zoom prices IPO at $36 per share, valuing it at $9.2 billion: Source

Icahn is intelligent ! He already sold his stake profitably to George Soros during Pre-IPO stage.

what is the profile of a Pinterest user?

and…

why does she/he use it?

Sell clouds buy IPO