Now that’s what I call bombing 2019:

2 Likes

Isn’t it one of Cramer’s babies?

Are they the first cloud company to have a bad earnings report this quarter? It seems most are killing it.

![]()

Just bought a million dollar worth yesterday!

Updated list

I’m really surprised by ring central. Who needs a phone anymore? Zoom is killing it on video conferencing. Twilio solves the customer facing communications issue for text and phone. Slack is the messenger tool of choice.

Clouds are been dumped recently, out of vogue or overvalued?

Rotation. It happens periodically and is the time to buy.

1 Like

As number of bullish articles on TWLO increases, the harder TWLO falls!

The 4th Industrial Revolution Is Upon Us: Prepare Your Portfolio

3 Growth Stocks to Buy and Hold for the Next 50 Years

Twilio Gains Traction From Partnership Wins, Global Growth

10 ‘Strong Buy’ Tech Stocks to Buy Now

3 Stocks Poised for Huge Growth Over the Next Decade

2 Top Growth Stocks All Set to Step on the Gas

Why You Should Be Buying This Top Cloud Stock

The Best Stocks to Invest in Artificial Intelligence and Augmented Reality

The whole cohort is getting hammered today. It’s a good time to watch for ones to buy. On days like this, I love to sell puts of stocks I want to add.

TWLO went below the 200-day.

![]()

Cloud stocks are hit hardest today.

What are opinions on SQ? Is it reasonably priced now - seems to be about 10x earnings?

I’ve not been a fan of it. The core business isn’t a money maker. They need upsells to actually make money.

1 Like

Owned two in

Cramer’s updated list:

SPLK

AYX

NOW

TWLO

TEAM

HUBS

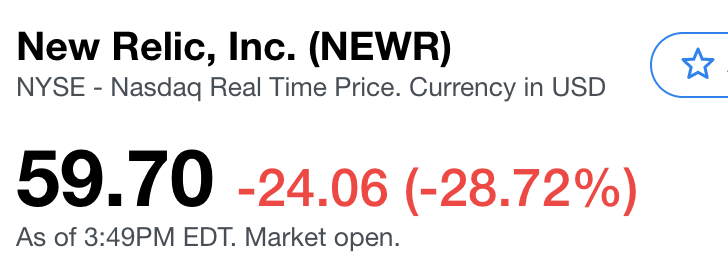

NEWR

FIVN

RNG

ZEN

Owned four of the

Cloud kings

ADBE

CRM

NOW

VMW

SPLK

WDAY

TWLO

Owned none of the

Cloud princes

HUBS

NEWR

OKTA

TEAM

COUP

My mind is filled with full of issues, unable to focus on stocks !

However, my 2 cents.

This is the period all hypes (Momentum Hypes) will fail and only really strong revenue, profit companies stay in market. Stay away from all non-profit making companies.

1 Like

Almost all cloud stocks are loss making ![]() and overvalued. Long term, doesn’t matter right?

and overvalued. Long term, doesn’t matter right?

Matters…If they are loss making now, will they make break even or further loss during downturn or recessionary period?

If they continue to make loss after loss (say UBER, WeWork…) they will eventually bankrupt with unsustainable level.

It is up to the investor to evaluate good companies, even if it is loss, that can sustain long term so that investor can hold long without minding about one or two years dip.

That is where I rely on big players holdings, such as buffet’s TEVA, even though company is making loss, it will recover as buffet would have made sure his billions are not vanished in downturn.

I care 100x more about cash flow break even than profitability of fast growing companies. Companies go bankrupt because of cash flow not profits. Most cloud companies get paid for a full year upfront and have to defer the revenue to recognize it over a year. That makes the cash flow amazing. Especially since the gross margins are sky high.

It’s way better than manufacturing companies with long supply chains. Those companies could have to pay suppliers before they even sell the product to the end customer. The early genius of Amazon was 90 day payment terms with suppliers and crazy fast inventory turns with immediate payment by customers. They were turning inventory faster than anyone which gave them cash flow to invest in growth.

Also, the longer the time between issuing supplier purchase orders and collecting from customers the more risk something could go wrong. A competitor could launch a new product that dramatically cuts sales. A natural disaster would eliminate sales from a region. There’s inherently far more risk, since the supply chain requires making commitments months in advance. Electronics made in China and shipped by ocean to the US have 5 month+ lead times. The assembly line can crank them out in a day but components like displays have very long lead times. Semiconductors do too. If they don’t start making your parts months in advance then you won’t have them. They won’t start without a purchase order, so companies are committed to buying them months in advance.

Why did AMZN go into hardware if their current model is so good?

Short story for those who doesn’t know: Before SJ, Apple nearly go bankrupt because of bad supply chain. During the first few years of SJ/TC era, Apple made less revenue but is profitable instead of loss-making, power of good supply chain.

Something doesn’t add up. Why do many of them go into subscription based? Thot subscription based is more profitable in the long term e.g. ADBE. Short term, those who move into subscription based got hammered e.g. NTNX.

Hardware is a platform for AI and to make ordering easier. All the hardware is sold around breakeven price point. It’s about the data.

Customers want subscription based vs spending huge money on servers and software to run on it. Paying for a year in advance is nothing for customers compared to buying severs to run enterprise software. Plus, the customers don’t need a bunch of IT people to run and maintain data centers. You can deploy SAAS apps in days vs months of you’re buying servers.

1 Like

Awww no love for fellow comrade CEO: