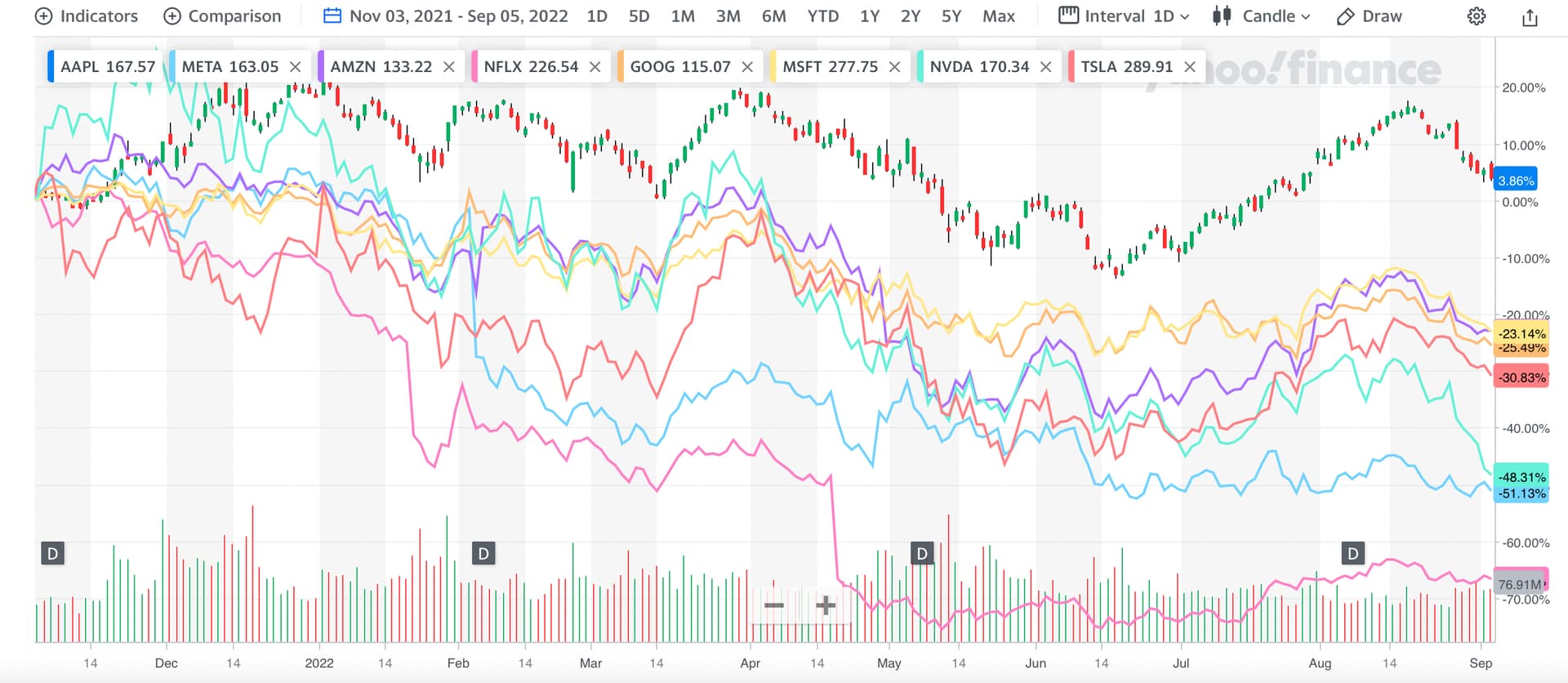

Technically, only AAPL AMZN TSLA NFLX of FANGMANT are above 50-day SMA.

Since @manch misses the boats of AAPL and TSLA, jumping onboard of AMZN seems ok so far

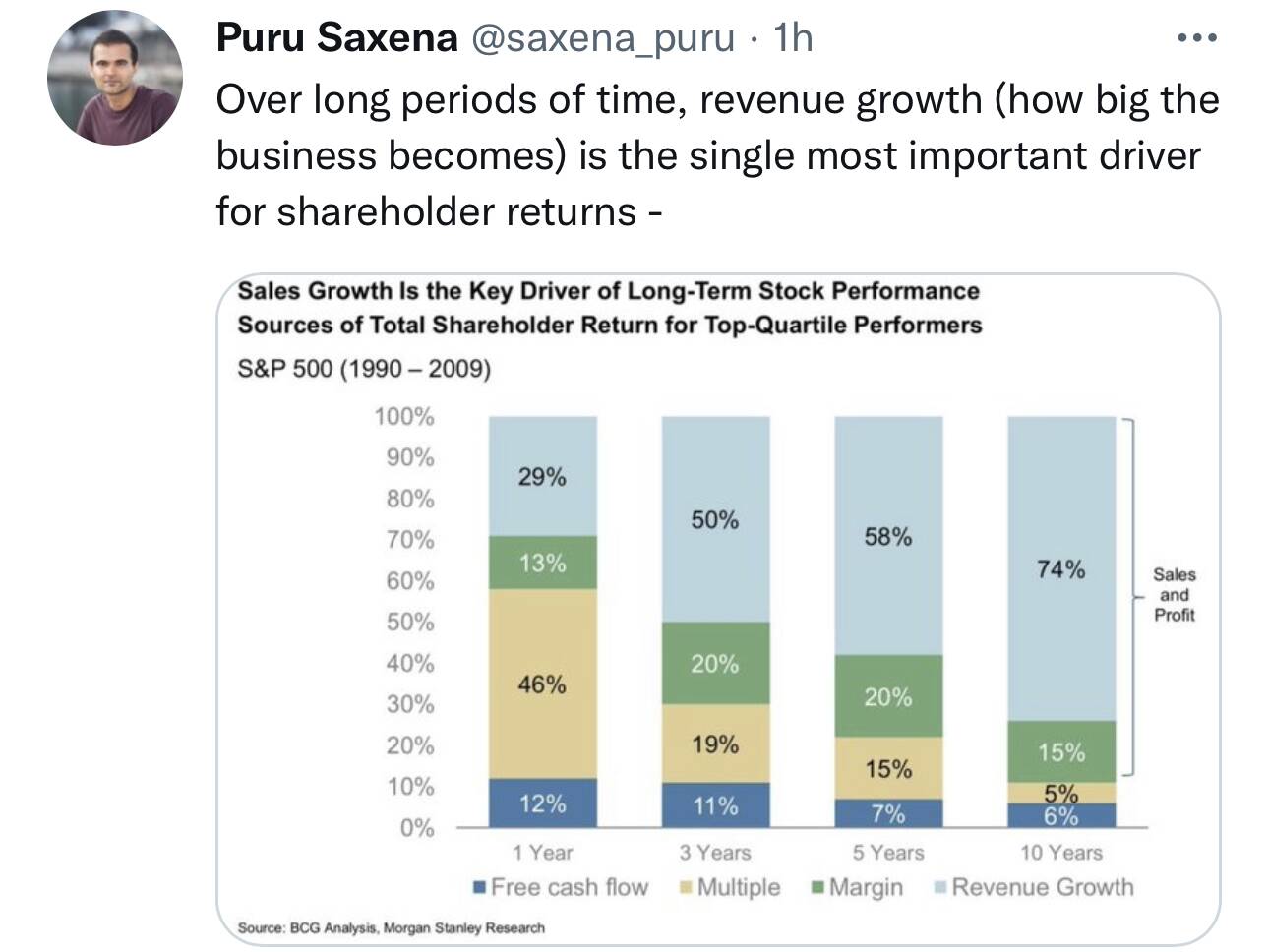

He’s not wrong. Any big 100B company today like Walmart and Costco was once a 100M company. They got to be worth 100B by their consistent revenue growth over decades.

Kevin thinks META has bottomed, bought in. FA indicates price is too low BUT FA metrics are irrelevant if business is in a decline. Many investors don’t want to take risk with metaverse. Are those investors sold out of META? If yes, META has bottomed. https://twitter.com/SPYleaps/status/1585576443425308672/photo/1

When you’re down, people say such things about you.

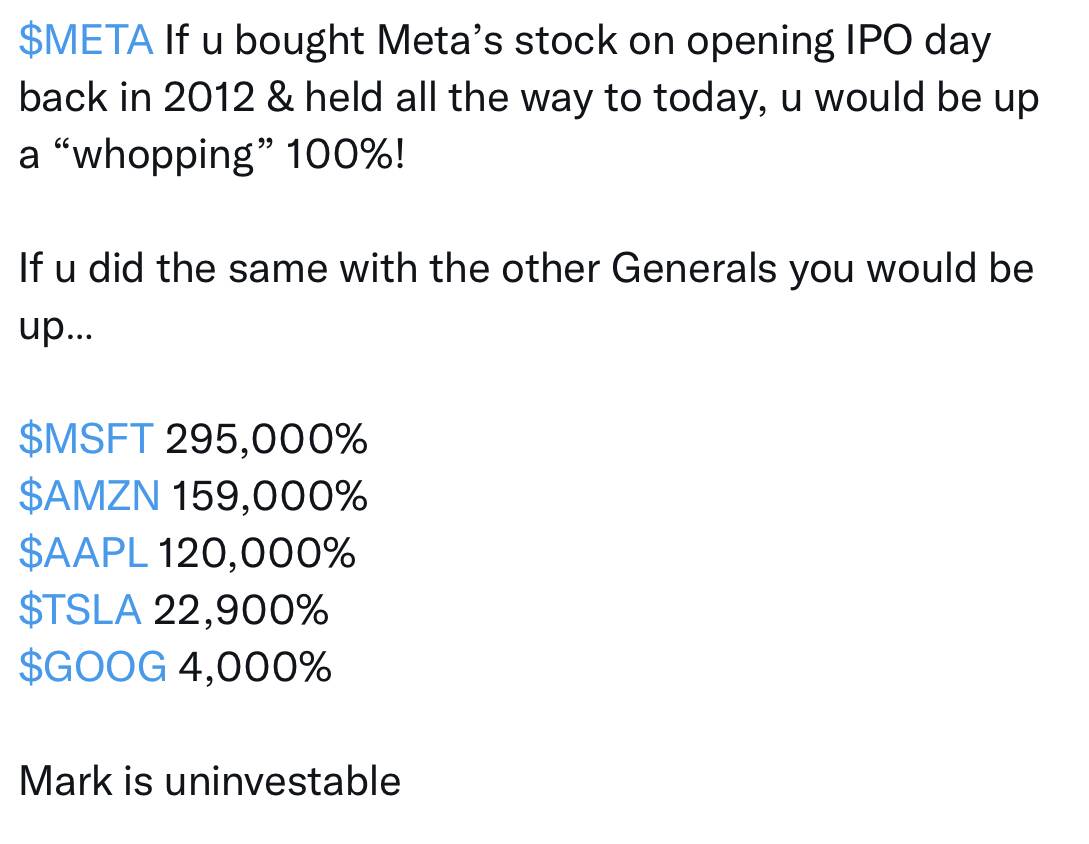

The reason for such a low return is because Mark has intentionally waited for a long time to IPO FB, he didn’t want those “add little value” investment companies (e.g. GS) to make tons of money from the IPO.

The reason for such high return for MSFT is because it is not well known at IPO. It was just a tiny software development company. To spot such company is nearly (nearly because may be some people can) impossible. Whereas FB (now META) and GOOG were well known at IPO.

MSFT ipo-ed in the 70s. Most of those investors are now either dead or too old to enjoy their wealth. META’s IPO investors are still alive and kicking.

I want to be a friend of BG. Even if no CEO job, can leverage on BG’s parent. Networking or guanxi is critical to huge success in corporate or investment.