So amazon is starting to leverage its hardware (Alexa home automation) as entry point to offer services, in the above case financial service. This is similar to Apple leveraging its iPhones to offer Apple Pay and Apple Card.

Square also has its own hardware in the form of terminals and card readers. It’s pretty dominant at least in small to medium businesses.

If you are serious about software, you need to do your own hardware.

Can people ask Alexa how much money they have in a certain bank account? Can people do online banking with Alexa saying something like “pay John $10 for pizza”?

People who install Alexa speakers in their house is not someone who worry about being hacked. Theoretically Alexa is just the computer version of a real life assistant. If you were a big boss like Bill Gates would you do your own online banking? Or would you tell your (human) assistant to take of things for you?

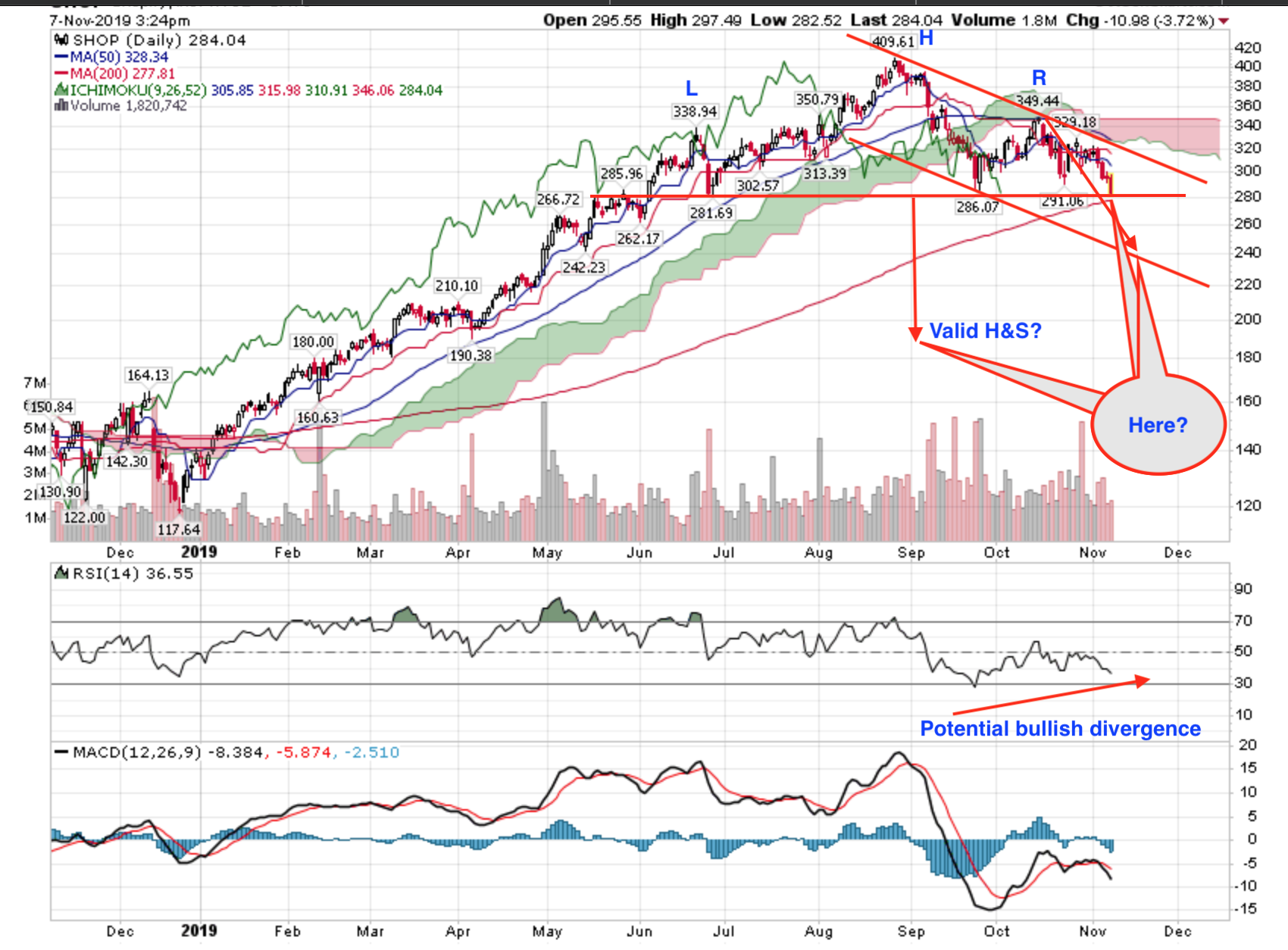

Read the headlines on SHOP earnings and you realize why Wall Street analysts are clowns. They probably did the headlines on purposes to drive the stock down, so their firms can buy. It rebounded after a big swing lower.

Their offerings are so still about multi- and omni channel. The latest is unified commerce. However, I noted that TrueCommerce can be integrated with Shopify to provide that Not sure how good is it. MSFT has an unified commerce product, Dynamics 365.

Shopify’s ecosystem continues to expand with newer features like its payments platform Shopify Pay, a point-of-sale card reader, a wholesale channel for buyers, bulk label printing services, APIs (application programming interfaces) and augmented reality features for mobile apps, and cash advances to merchants via Shopify Capital. It also recently acquired fulfillment automation start-up 6 River Systems to bolster its logistics services.

Shopify’s revenue growth is decelerating, but it’s still remarkable for a 15-year-old company. As for the organization’s bottom line, the growth of its higher-margin services and tighter cost controls should eventually stabilize earnings growth.

However, Shopify’s biggest weakness is still its valuation. It trades at nearly 350 times forward earnings and over 17 times next year’s sales, which suggests that the stock is priced to perfection.

By comparison, Adobe trades at less than 30 times forward earnings and roughly ten times next year’s sales. Analysts expect Adobe’s revenue and earnings to rise 18% and 24%, respectively, next year – which makes it a less volatile play on the cloud-based e-commerce, marketing, and creative software markets.

In short, Shopify’s business is still rock-solid, but its stock looks dangerously speculative. Investors shouldn’t fret too much about its mixed third-quarter numbers, but they should only nibble at the stock at these frothy levels.

Below gave some color on why SHOP building a FBA is the right move.

Tobias the founder wants to arm the rebels, sound like what SJ has said during the early days of Apple. Should have researched more about SHOP during 2017

4 possible bottoms,

200-day SMA i.e. 2mrw re-bound. Bought more, now own 18 just in case the train leaves without me.

$230 i.e. 1:1 zigzag

$200 H&S in log graph

$160 H&S

Not sure how good is it. MSFT has an unified commerce product, Dynamics 365.

Not sure how good is it. MSFT has an unified commerce product, Dynamics 365.