Logic makes sense but its already 4 months since rates passed 4% and 2 months since passed 5%. But the home closing prices are only inching higher. Lets see how true the predictions of crash are going to be. Every 1% rate bump means 10% reduction in prices, so prices should already be down by 20% but so far none. May be as you say it will play out slowly but there are still little to no signs, in fact prices are still rising. If rates go up by another 2%, should we expect another 20% drop in RE prices, meaning 40% total drop. This logic sounds preposterous in the face of still rising prices.

Prediction is the first step of planning. What to do next?

Bay Area

As a buy n hold RE investor, nothing i.e. not selling any rentals or buying any new rentals. My rentals have been cash-out re-fi at below 3% fixed 30 yr loan and sitting on 150%-200% gain. Rents have been lagging for many years, are catching up fast.

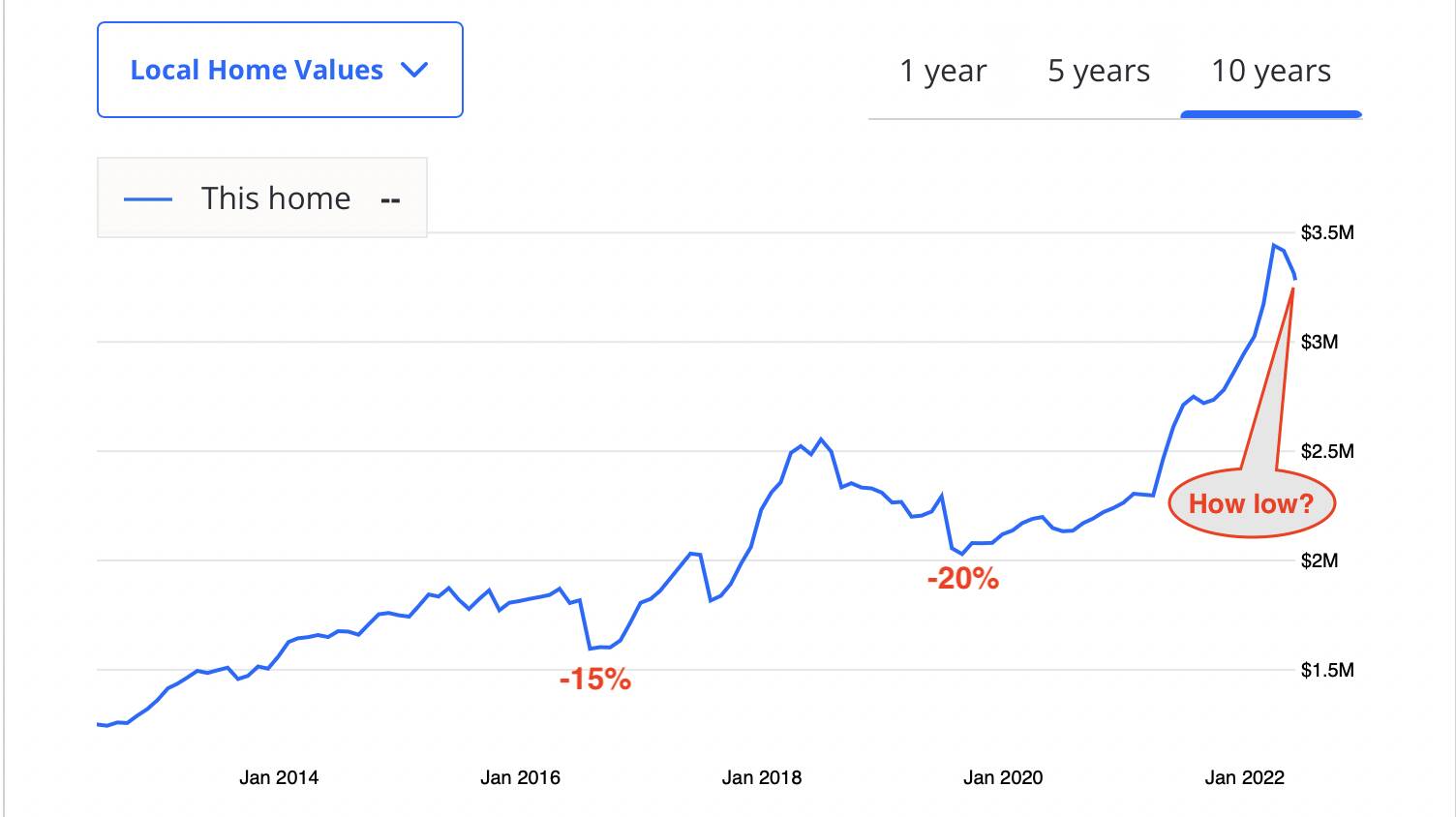

Below is the Zillow’s price chart for one of my rental… clearly price is weakening, how low would it decline by before it rallies again RE is a secular compounder, unless you really need $, selling is not a good idea considering the selling cost is pretty high.

Inventories are not that low in the markets I follow ($2–5M range in mid-peninsula). Maybe the story is different further out where WFH has had more of an impact. Mountain View has the highest inventory I’ve seen since 2010 and 2/3rds of the properties have been listed >14 days. 94010 (Hillsborough/Burlingame) has also seen a significant increase in inventory over the last 1–2 months.

Things have definitely cooled down but we’ll need to wait until fall/winter to see whether the fed manages to pull off a soft landing. Personally I don’t think these higher rates are sustainable. The fed will get cold feet once the true economic impact starts to appear.

Exactly. If one can withstand the mortgage payment for a year or two, should not hesitate to buy the dream home (if found one) at today’s price. Can re-fi at lower rate when the rate is down

What I heard is those WFH areas are softening more because people realize future is hybrid and not 100% WFH.

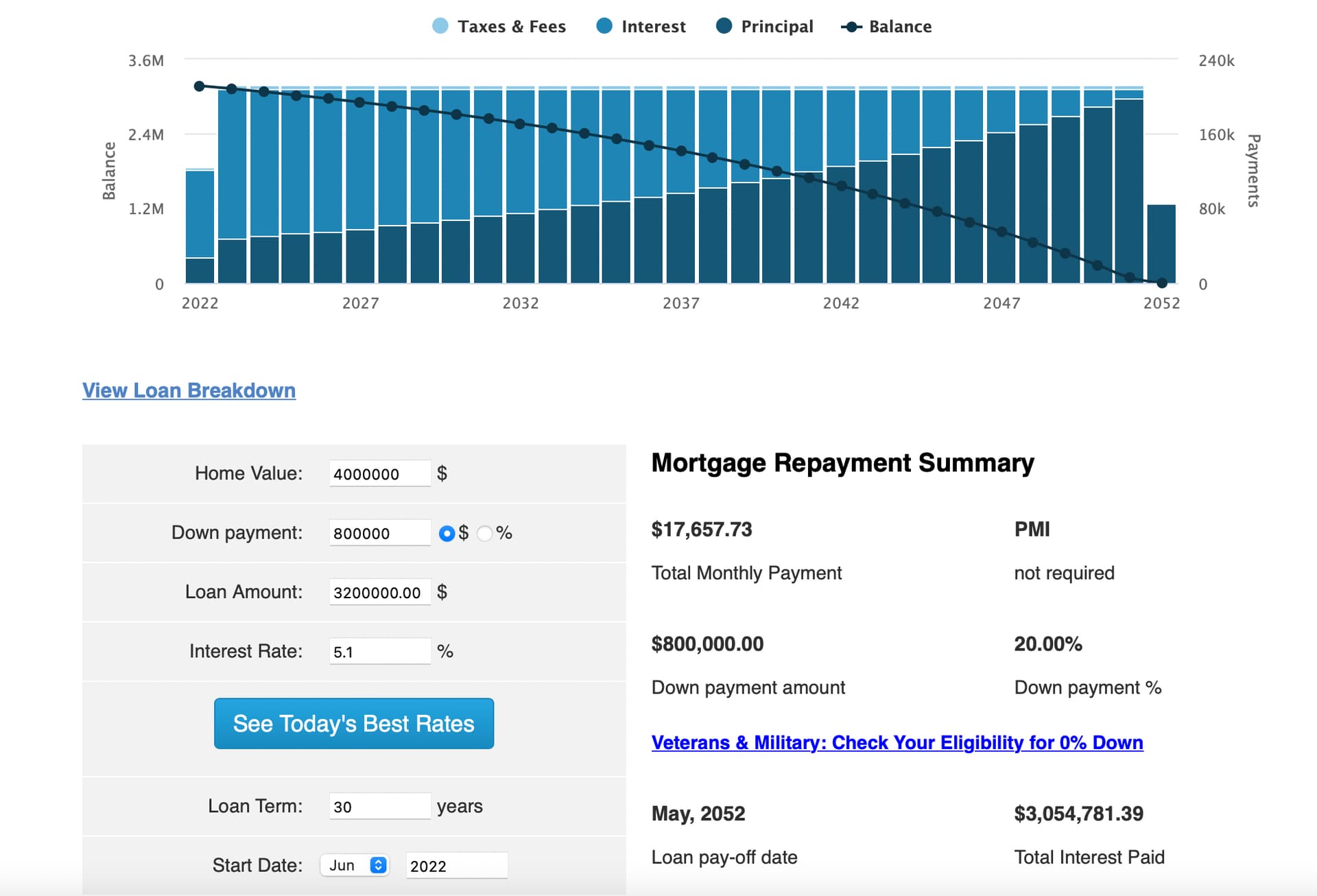

This is not artificial run up, but physically some party paid the price to seller.

In addition, SFBA most of the homes are very old, the house insurance remake value is very low than land value. No loans for land value.

For more clarity, $4M home carries land value 3M (paid cash) while Home value max $1M. The loans on the home value is $800k (mortgage). Such homes, no one will sell the home at loss as they may be cash rich !

A party who buys $4M must have at least 10M Networth and after tax $10000/month income stream (as property tax/month=$4000).

This kind of homes won’t come down as very less sellers will be. Second, most the first homers, with < 3.5% interest locked, got second home.

Mortgages/real estate are like bonds, not like stocks and they are vary hard to reduce the value.

Still I do not say real estate won’t come down in bay area, but the impact will not be great without S&P going down further.

Hard to feel sorry for this woman. So her house only went up 5 times instead of 6. Her big problem is capital gains tax. After the $500k freebie she will be paying 100s of thousands in taxes. Now that’s something to cry about and a major cause of the inventory shortage.

She and her husband should just stay even if the house a bit big for them Now.

SS is not taxed in California. Her property tax is dirt cheap. Assuming she likes her neighborhood, etc, financially she will be more than fine staying.

It won’t help with our housing inventory issue but whatever do what’s best for your own situation.

Gloria Othon is feeling the cooling market first hand. Othon, 61,

It’s 100% due to Fed easy money. When rates rise it should be back in theory at least. Do you also think gas prices food prices lumber prices etc will stay elevated? I think they will come down for sure.

Lumber prices have been tumbling.

Apparel prices have been declining.

China has ended lockdown. Prices of manufactured goods should start to decline.

Gas and food may have to wait a little longer.

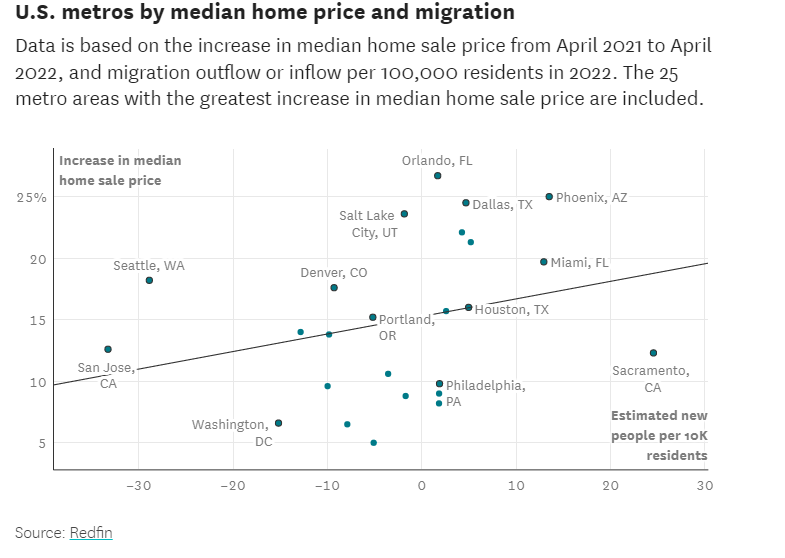

Sacramento had the highest incoming migration rate among the 25 major metros examined by Redfin, at 24.5 new people per 10,000 residents, but a relatively modest home sale price increase of 12.3% year-over-year. The metro area attracted many Bay Area residents earlier in the pandemic, as offices went remote and people sought out more space.

Marr said a “dramatic” 30% rise in home price growth in spring 2021 was followed by a “really big slowdown” more recently. While he said he couldn’t pinpoint the reasons, he suspected that during that period, many Bay Area residents left for a wider range of places out of state, not just Sacramento and the Central Valley.

Greater supply might also be keeping Sacramento’s home-price growth lower, he added. According to the April 2022 report from the Sacramento Association of Realtors, inventory increased 33% from April of last year, with 1,342 active listings as of April 2022.